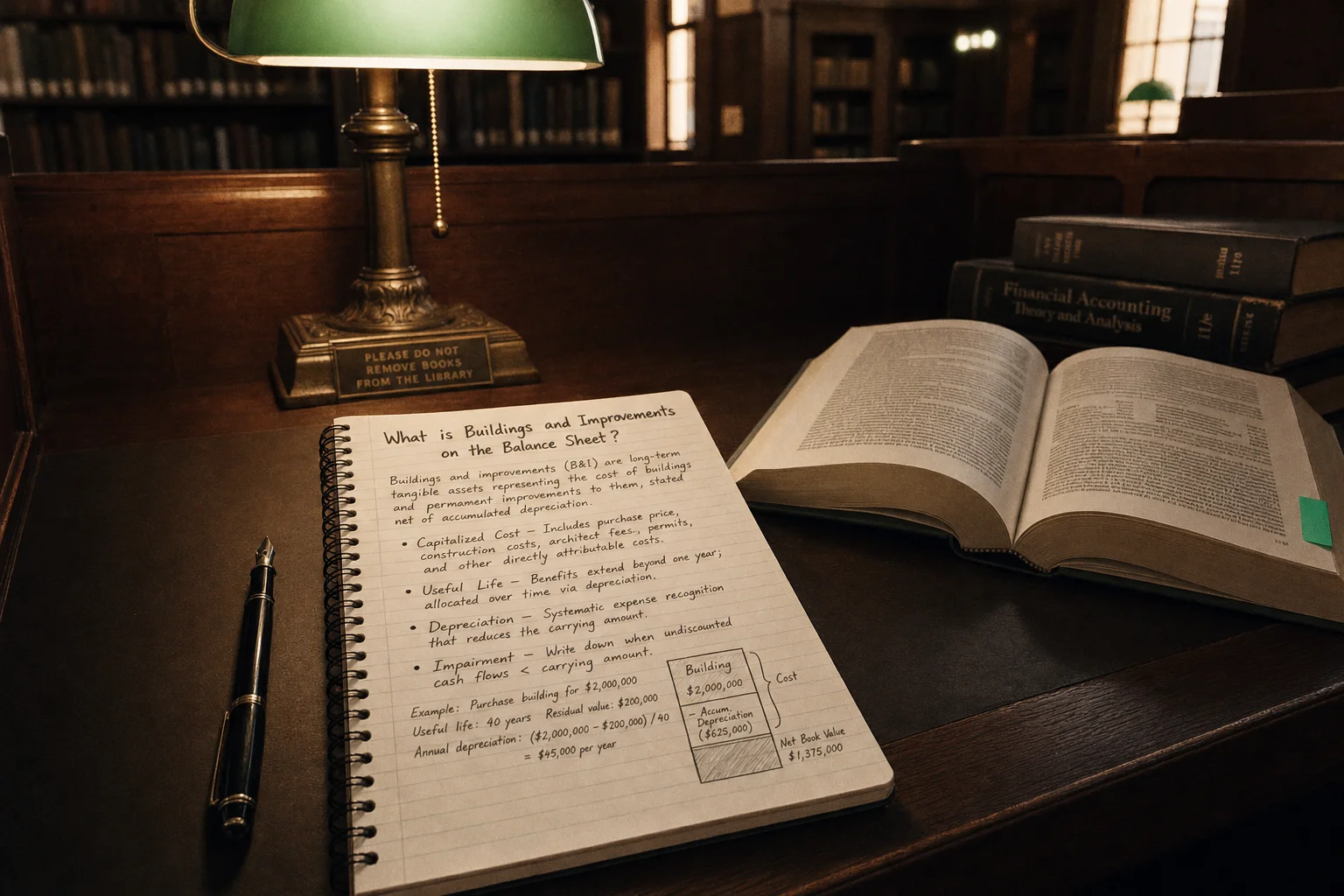

Buildings and improvements records the historical cost of owned structures, additions, and permanent renovations within PP&E. These assets are capitalized and depreciated straight-line over 20–50 years, separate from non-depreciable land.

Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.

Buildings and Improvements is a sub-account within Property, Plant, and Equipment (PP&E) that records the historical cost of owned buildings, structures, and permanent improvements made to them (e.g., additions, renovations, or leasehold improvements with long useful lives). These assets are capitalized and depreciated over their estimated useful lives, reflecting their contribution to long-term operations.

What It Includes

Buildings and Improvements captures the capitalized cost of:

- Office buildings, factories, warehouses, retail stores

- Structural additions or expansions

- Major renovations (roof replacement, HVAC upgrades)

- Leasehold improvements on leased buildings (if long-term)

- Site improvements directly tied to building use (e.g., parking lots, fencing)

Land is recorded separately because it is not depreciated.

Costs include purchase price, construction, professional fees, and qualifying interest during construction.

“Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

Accounting Treatment

Capitalization and depreciation:

- Record at historical cost (purchase + directly attributable costs)

- Transfer from Construction In Progress upon completion

- Depreciate systematically over useful life (commonly straight-line)

- Residual value considered (often low for buildings)

- Impairment tested if indicators present

Leasehold improvements depreciated over shorter of lease term or useful life.

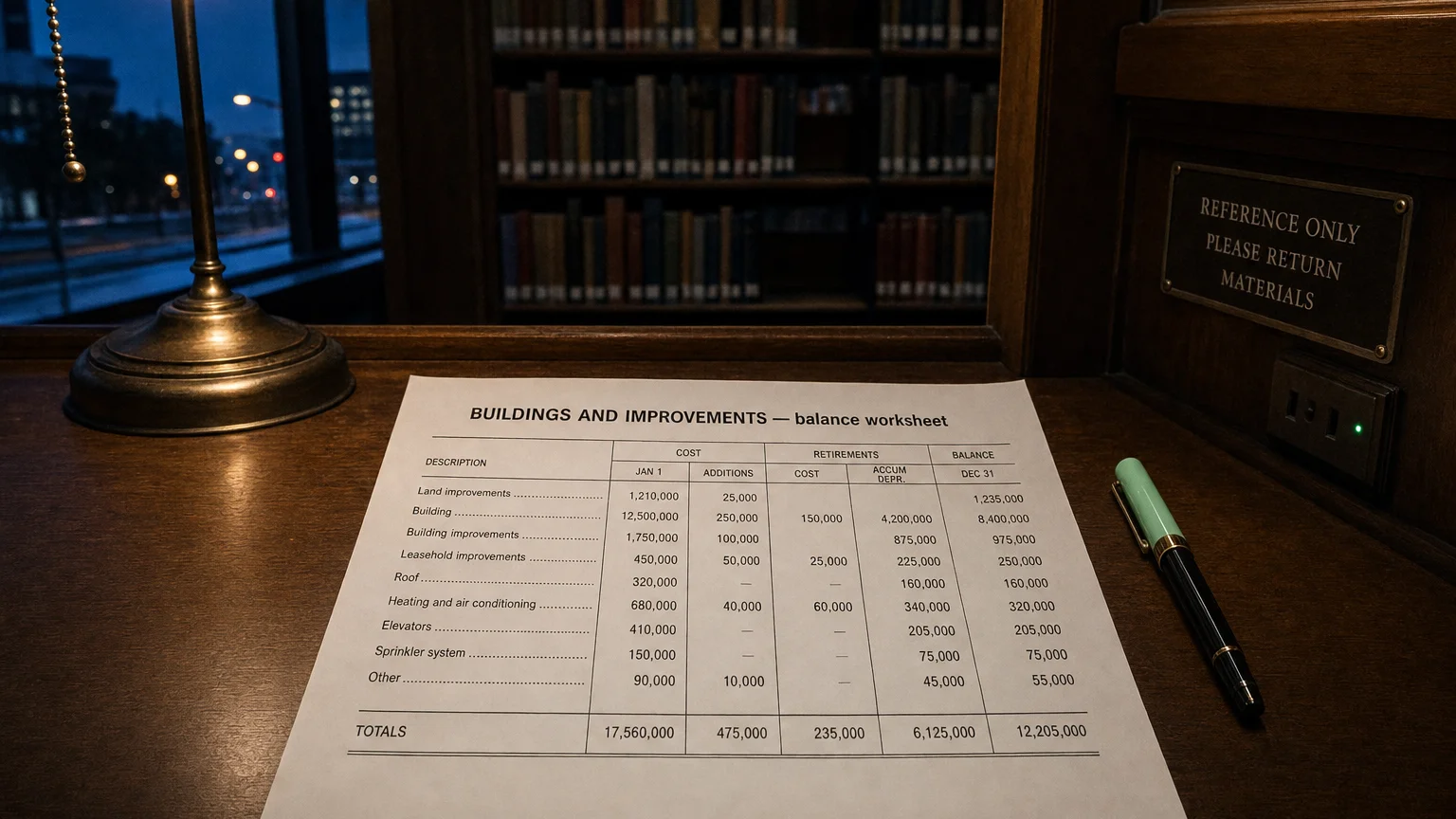

Balance Sheet Presentation

Within Property, Plant and Equipment section:

- ‘Buildings and Improvements’ at gross cost

- Less accumulated depreciation → net book value

- Often largest component of PP&E for many companies

- Disclosed separately from Land, Machinery, etc.

Footnotes detail useful lives, depreciation method, and major additions.

Distinction from Other PP&E

Buildings and Improvements

- Long-lived structures and permanent enhancements

- 20-50 year typical life

Land

- Non-depreciable

Machinery & Equipment

- Shorter lives (5-15 years)

Construction In Progress

- Incomplete buildings (not yet depreciated)

Why It Matters

- Major component of asset base and collateral value

- Significant depreciation expense impacts earnings

- Reflects historical capital investment in facilities

- Age and condition affect maintenance capex needs

- Revaluation possible under IFRS (not US GAAP)

Analytical Implications

This account provides insight into:

- Operational footprint (owned vs. leased facilities)

- Capital intensity of business

- Future depreciation burden

- Asset age (gross book vs. accumulated depreciation)

- Investment in capacity expansion

High gross value with low net (heavy depreciation) may indicate aging infrastructure needing replacement.

Q · 01What is included in buildings and improvements?+

Q · 02How is buildings and improvements depreciated?+

Q · 03Why does buildings and improvements matter to investors?+