Accumulated Depreciation Definition & Formula

Accumulated depreciation is the running total of depreciation charged against an asset since purchase. Learn how it reduces book value on the balance sheet.

Overview

Accumulated depreciation is the running total of depreciation charged against an asset since purchase. Learn how it reduces book value on the balance sheet.

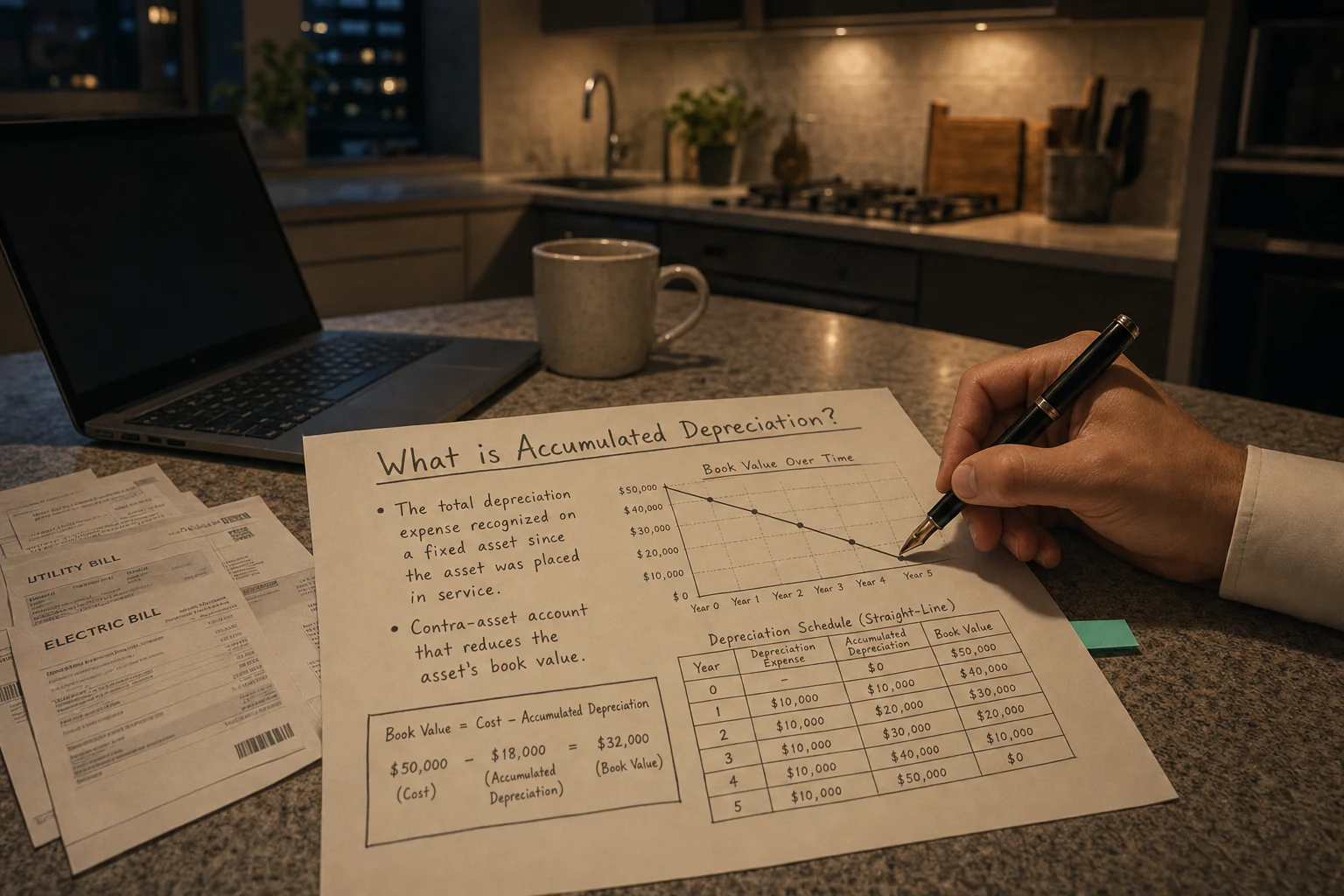

Accumulated depreciation is the total amount of depreciation that has been recorded on an asset since it was acquired and put into use. In other words, it represents how much of the asset’s cost has been used up or allocated as expense over time. Each time a business records depreciation expense for an asset, that amount adds to the accumulated depreciation balance.

In accounting, accumulated depreciation is classified as a contra-asset account, meaning it carries a negative balance that offsets the corresponding asset’s value. It is listed under the asset section of the balance sheet (usually as a credit or negative figure) to reduce the gross value of the asset. This allows the financial statements to reflect the asset’s net book value – essentially the asset’s original cost minus all depreciation taken to date.

Accumulated Depreciation vs. Depreciation Expense

It’s important to distinguish accumulated depreciation from depreciation expense, as they relate to each other but are not the same:

Depreciation Expense: This is the portion of an asset’s cost allocated as an expense for a single accounting period (for example, one year or one month). It represents how much of the asset’s value was “used up” during that period. Depreciation expense appears on the income statement as a non-cash expense, reducing the company’s net income for the period.

Accumulated Depreciation: This is the cumulative total of all depreciation expense recorded on an asset since the asset was placed in service. It is the sum of each year’s (or period’s) depreciation expenses for the asset up to the current date. Accumulated depreciation appears on the balance sheet as a contra-asset account that reduces the asset’s carrying value. It does not appear on the income statement; only the current period’s depreciation expense does.

In summary, depreciation expense measures the asset’s value decline for a specific period, whereas accumulated depreciation measures the total decline in value to date for the asset. Each period’s depreciation expense gets added to the accumulated depreciation account over the life of the asset.

How Depreciation is Calculated and Accumulated Over Time

Depreciation is calculated using an appropriate method to systematically spread an asset’s cost over its useful life. The simplest and most common method is straight-line depreciation, where the expense is the same each period. The straight-line formula is:

Annual Depreciation Expense = (Cost of Asset – Salvage Value) / Useful Life

Cost of Asset is the original purchase price.

Salvage Value (or residual value) is the estimated value of the asset at the end of its useful life (what you expect to sell or scrap it for at the end).

Useful Life is how long the asset is expected to be used in the business (e.g. 5 years, 10 years, etc.).

For example, if a machine costs $25,000 and is expected to be used for 5 years with a $2,000 salvage value, the annual depreciation expense using straight-line would be:

$25,000−$2,0005 years=$4,600 per year\frac{\25,000 - \2,000}{5 \text{ years}} = \4,600 \text{ per year}5 years$25,000−$2,000=$4,600 per year

Each period (year) that depreciation expense is recorded, the same amount is added to the accumulated depreciation. In the example above, after the first year, accumulated depreciation on the machine would be $4,600. After the second year, it would increase to $9,200, and after four years it would total $18,400. This accumulation continues until the asset’s total depreciation equals its depreciable cost. Once the asset is fully depreciated (i.e. the accumulated depreciation equals the asset’s original cost minus any salvage value), no further depreciation expense is recorded. Accumulated depreciation will never exceed the asset’s cost – depreciation stops when the asset’s book value reaches the salvage value or zero.

If the asset is disposed of or sold, the accumulated depreciation associated with that asset is removed from the books. The asset’s cost and its accumulated depreciation are taken off the balance sheet, and any difference between the asset’s book value (cost minus accumulated depreciation) and the sale price is recognized as a gain or loss.

Balance Sheet Presentation and Net Book Value

On the balance sheet, accumulated depreciation is shown alongside the related asset, but as a negative value (since it’s a contra-asset). Typically, the asset’s original cost is listed, and then a line for “Less: Accumulated Depreciation” is subtracted to arrive at the asset’s net book value (also called carrying value). For instance, a balance sheet might display:

Equipment – at cost: $239,000

Less: Accumulated Depreciation: $(100,000)$

Equipment, net (book value): $139,000

In this example, the equipment’s net book value is $139,000, which equals its $239,000 cost minus $100,000 accumulated depreciation. The net book value is the amount at which the asset is carried on the balance sheet, and it reflects the un-depreciated portion of the asset’s cost. (Note that the net book value is an accounting value and is not necessarily the asset’s market value; it simply follows the cost allocation over time.)

Because accumulated depreciation is a contra-asset, it may be presented in parentheses or with a minus sign. Some balance sheets list each fixed asset “net of accumulated depreciation,” while others show the cost and accumulated depreciation separately as illustrated above. Either way, the presence of accumulated depreciation ensures that the asset’s book value is reduced over time to reflect depreciation.

It’s important to understand that accumulated depreciation is neither a liability nor a “fund” of cash; it’s purely an accounting figure. It doesn’t represent money set aside, but rather it’s an offset to the asset’s cost. By tracking accumulated depreciation, companies can show the original cost of assets and how much of that cost has been allocated to expense, giving clarity on the asset’s remaining value on the books.

Why Accumulated Depreciation is Important

Accumulated depreciation plays a vital role in accounting and financial reporting for several reasons:

Proper Expense Matching: It implements the matching principle in accounting, which means the cost of a long-term asset is spread out and matched to the periods that benefit from its use. This prevents a large expense all at once when the asset is purchased, leading to more consistent and fair reporting of profits over time. By depreciating an asset over its life, companies avoid distorting any single year’s profit with the entire cost of the asset.

Realistic Asset Values: It provides a more realistic view of asset values on the balance sheet. Accumulated depreciation reduces the recorded value of assets to reflect wear and tear or usage. The resulting net book value (cost minus accumulated depreciation) is an estimate of the asset’s current worth on the books. This helps investors and management see how much of an asset’s useful life has been used up and how much remains, rather than seeing the asset at full historical cost indefinitely.

Insight for Management and Investors: The amount of accumulated depreciation can indicate the age and stage of an asset. A high accumulated depreciation relative to an asset’s cost suggests the asset is older or nearing the end of its useful life, which can signal the need for replacement or maintenance. Tracking this helps in business planning – for example, planning for capital expenditures to replace fully-depreciated assets. It also gives lenders and investors insight into how “used up” the company’s fixed assets are, which can factor into decisions about credit or investment.

Impact on Income and Taxes: Depreciation expense (which accumulates in the accumulated depreciation account) is a non-cash expense that reduces taxable income. This provides tax benefits by spreading deductions over several years. Although accumulated depreciation itself isn’t on the income statement, it represents the total of those deductions taken over time. In tax and accounting, the accumulated depreciation is used to determine an asset’s adjusted basis (book value), which is important for calculating any gain or loss when the asset is sold and for ensuring compliance with tax rules that require systematic depreciation rather than immediate expensing.

Accuracy of Financial Reporting: By reporting accumulated depreciation, financial statements adhere to generally accepted accounting principles and present a more accurate financial position. It ensures that the balance sheet reflects the consumption of assets, and the income statement reflects the appropriate expenses for each period. This improves the quality of financial reporting and helps stakeholders make better decisions based on the company’s true financial condition.

Example: How Accumulated Depreciation Works

Let’s illustrate accumulated depreciation with a simple example. Suppose a company buys a piece of equipment for $10,000, expecting it to last 5 years with no salvage value (for simplicity). The company uses straight-line depreciation. This means it will depreciate the equipment evenly over 5 years – in this case, $2,000 per year ($10,000 ÷ 5). Below is how the depreciation expense and accumulated depreciation would progress year by year:

At Purchase: Equipment is recorded at its full cost of $10,000. Accumulated depreciation is $0 (asset is brand new). The equipment’s book value on the balance sheet is $10,000 (cost $10,000 minus $0 depreciation).

End of Year 1: The company records $2,000 of depreciation expense for the first year. Accumulated depreciation now becomes $2,000 (total to-date). The equipment’s net book value is $10,000 – $2,000 = $8,000.

End of Year 2: Another $2,000 depreciation expense is recorded. Accumulated depreciation increases to $4,000 (the sum of year 1 and year 2 depreciation). Book value is now $10,000 – $4,000 = $6,000.

End of Year 3: Record another $2,000 depreciation. Accumulated depreciation is $6,000. Book value is $10,000 – $6,000 = $4,000.

End of Year 4: Record $2,000 depreciation. Accumulated depreciation grows to $8,000. Book value is $10,000 – $8,000 = $2,000.

End of Year 5: Record the final $2,000 of depreciation. Accumulated depreciation is now $10,000, which equals the asset’s full cost. The equipment’s book value is $10,000 – $10,000 = $0. The asset is fully depreciated (no remaining book value). At this point, no more depreciation expense will be recorded on this asset.

Figure: Example of an asset being depreciated over 5 years. The accumulated depreciation grows each year (by the annual depreciation expense), and the net book value of the asset declines accordingly to zero by the end of year 5.

In this example, each year’s depreciation expense adds to the accumulated depreciation balance, gradually reducing the asset’s book value. After 5 years, the accumulated depreciation of $10,000 fully offsets the asset’s $10,000 cost, leaving a book value of $0. If the equipment had a salvage value (say the company expected to sell it for scrap at $500), the depreciation would stop once the book value reaches $500 instead of zero.

The concept is the same for any depreciable asset: Accumulated depreciation keeps a running total of all depreciation taken over the asset’s life, and the net book value (cost minus accumulated depreciation) tells you what value is left to be expensed in future periods. This ensures that the balance sheet and income statement are aligned in reflecting the asset’s usage and the expense of that usage over time, rather than all at once.

Summary: Accumulated depreciation is a key accounting concept that helps present a realistic value of assets on the balance sheet and properly match expenses with revenues on the income statement. It differs from periodic depreciation expense, but is built up from those expenses. By understanding accumulated depreciation, one can better interpret a company’s financial statements – seeing how much of the assets’ costs have been recognized so far and how much remains to be depreciated in future periods. This contributes to more accurate financial reporting and informed decision-making for the business and its stakeholders.