A guide to understanding the book value of a company's tangible fixed assets and what it reveals about their age, condition, and operational capacity.

Survival comes first, truth, understanding, and science later.

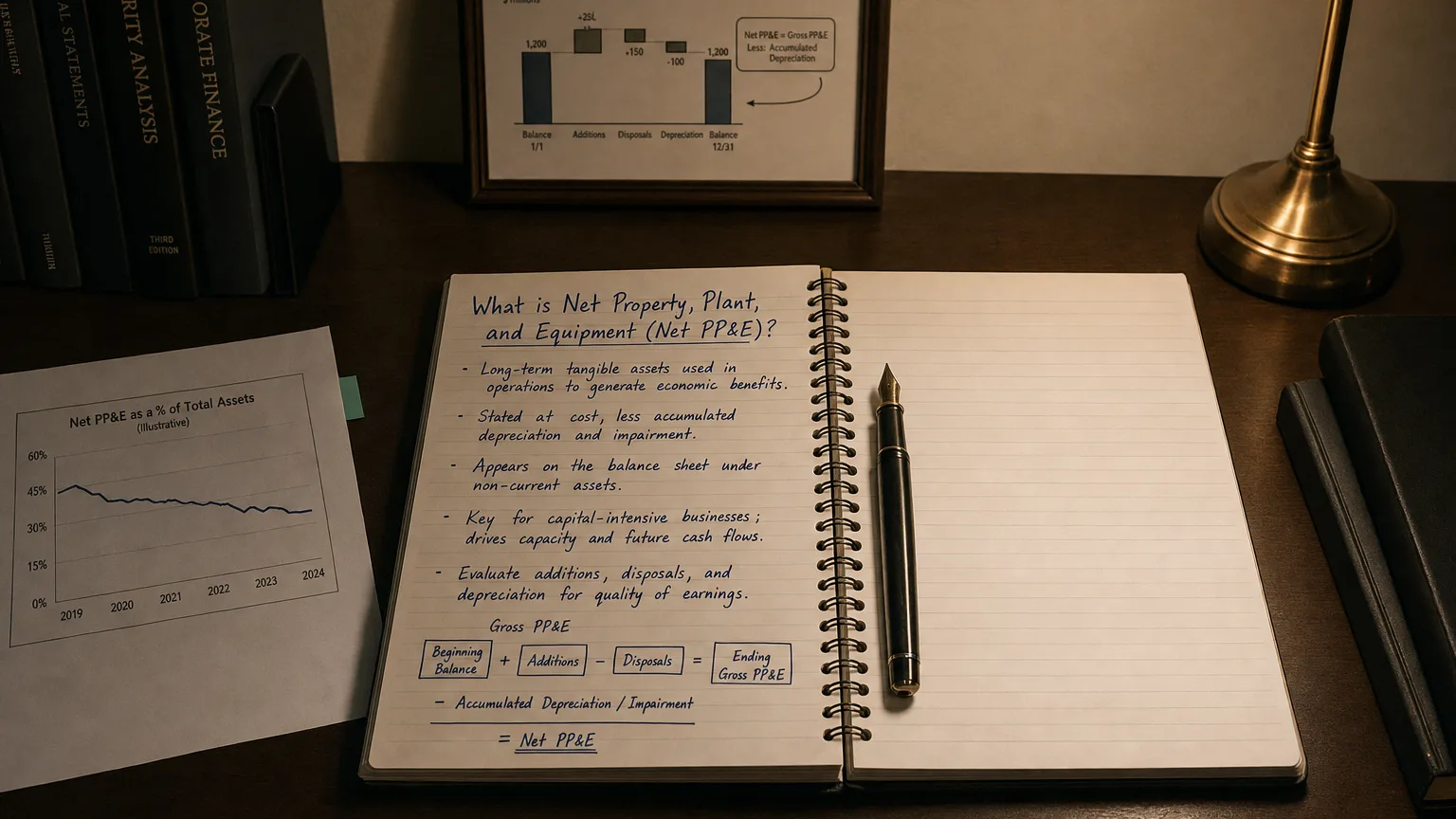

Net Property, Plant, and Equipment (Net PP&E) refers to the value of a company’s fixed tangible assets (such as land, buildings, machinery, and equipment) after accounting for depreciation. In other words, it represents the book value of those long-term assets as reported on the balance sheet. Net PP&E is typically listed under non-current assets on the balance sheet, often labeled as “Property, Plant, and Equipment, net (of depreciation).” This figure gives a snapshot of how much of the company’s investment in physical assets remains un-depreciated, reflecting their remaining useful value to the business.

Components of Net PP&E

Net PP&E is composed of two main components: Gross PP&E and Accumulated Depreciation. Understanding these components is key to understanding what Net PP&E represents:

-

Gross PP&E (Total Cost of Assets): This is the total historical cost of all the property, plant, and equipment a company has acquired. It includes the purchase price of assets and any costs necessary to get them ready for use (such as delivery and installation fees). Gross PP&E reflects the original investment in long-term assets before any depreciation. (For example, if a company bought machinery for $5 million and a building for $10 million, the gross PP&E would initially be $15 million.)

-

Accumulated Depreciation: This is the total amount of depreciation expense that has been recorded against those assets over time. Depreciation is the accounting process of allocating the cost of an asset over its useful life to reflect wear and tear or obsolescence. Accumulated depreciation grows each accounting period as depreciation expense is recognized, and it reduces the book value of the assets on the balance sheet. (Using the previous example, if over several years $4 million of depreciation has been recorded on the machinery and building, the accumulated depreciation would be $4 million.)

-

Net PP&E (Net Book Value): This is the difference between Gross PP&E and Accumulated Depreciation at any given time. It represents the remaining book value of the assets. Using the numbers above, Net PP&E = $15 million gross cost – $4 million accumulated depreciation = $11 million. This net amount is what appears on the balance sheet as the value of the company’s fixed assets after depreciation. Essentially, Net PP&E answers the question: “What is the current accounted value of our PP&E after accounting for all the depreciation to date?”

How Net PP&E is Calculated

In formula form, Net PP&E = Gross PP&E – Accumulated Depreciation. Many financial references express this relationship including the effects of new asset purchases (capital expenditures) in the calculation. For example, Investopedia defines PP&E as being calculated by taking the gross value of fixed assets, adding any capital expenditures, and then subtracting accumulated depreciation. In simple terms, at any point in time you arrive at Net PP&E by subtracting the total depreciation from the total asset cost.

Over an accounting period, the Net PP&E balance changes based on certain transactions. To see how Net PP&E is determined from one period to the next, consider the following steps:

-

Start with the beginning Net PP&E: Begin with the net PP&E value from the end of the previous period (this was the last reported balance on the prior balance sheet).

-

Add Capital Expenditures (CapEx): Capital expenditures are funds the company spends to buy new fixed assets or improve existing ones. These purchases increase the Gross PP&E. When a company invests in new equipment or facilities, that cost is added to PP&E on the balance sheet. (For example, if $2 million is spent on new machinery this period, that $2M increases Gross PP&E, and thus will increase Net PP&E before depreciation.)

-

Subtract Depreciation Expense: During the period, the company records depreciation expense to reflect the wear-and-tear or usage of its assets. Depreciation accumulates as a contra-asset (Accumulated Depreciation) and reduces the net book value of PP&E. Thus, you subtract the period’s depreciation from Net PP&E. If no new assets are purchased, Net PP&E will decrease each year by the amount of depreciation expense, since the assets are being used up.

-

Subtract Asset Disposals (if any): If the company disposes of any PPE assets during the period (by selling them or retiring them), those assets are removed from the books. This means removing the asset’s original cost from Gross PP&E and its accumulated depreciation from the Accumulated Depreciation account. The net effect is a reduction in Net PP&E equal to the asset’s net book value (cost minus depreciation) at the time of disposal. For example, if a vehicle that originally cost $100,000 (now with $90,000 in accumulated depreciation) is sold off, Gross PP&E drops by $100K and Accumulated Depreciation drops by $90K. Net PP&E decreases by the $10K net book value of the vehicle.

-

Arrive at the ending Net PP&E: After accounting for additions and subtractions in the steps above, the result is the ending Net PP&E balance. This ending balance is what is reported on the current period’s balance sheet as “Property, Plant, and Equipment (net).”

In equation form, a roll-forward of Net PP&E from beginning to end of period can be summarized as:

Ending Net PP&E = Beginning Net PP&E + CapEx – Depreciation – Net Book Value of Disposals.

This aligns with the idea that new investments increase the asset base, while depreciation and asset removals decrease it. As an illustration, Corporate Finance Institute provides an example: a company starts with $5,000,000 of gross PP&E and $2,100,000 in accumulated depreciation; it buys $1,000,000 of new equipment and records $150,000 of depreciation for the period. The ending Net PP&E is calculated as $5,000,000 + $1,000,000 – $2,100,000 – $150,000 = $3,750,000.

Example of PP&E on a balance sheet (excerpt). The balance sheet shows “Property & Equipment” net of depreciation. In this illustrative example, the company’s net PP&E was $25,482 at year-end 2013, and it declined in subsequent years as depreciation outpaced new additions.

Capital Expenditures and Asset Disposals: Effects on PP&E

Two key types of transactions directly affect the PP&E balance over time: capital expenditures and asset disposals:

-

Capital Expenditures (CapEx): These are investments in new fixed assets or improvements to existing ones. CapEx increases the Gross PP&E value. On the balance sheet, capital expenditures are added to PP&E (increasing the asset base) whenever the company purchases new equipment, builds a facility, or makes significant upgrades that extend an asset’s life. In the context of Net PP&E, capital expenditures will increase the net balance (assuming the new assets haven’t yet been depreciated or are only lightly depreciated). For example, if a company builds a new factory or buys a fleet of vehicles, its PP&E (gross and net) will rise by the cost of those investments.

-

Asset Disposals: When a company sells or retires an asset, it removes that asset’s value from the books. This involves taking out the asset’s cost from Gross PP&E and also removing the related accumulated depreciation. The result is a decrease in Net PP&E equal to the asset’s remaining book value at disposal. If an asset is fully depreciated (accumulated depreciation equals the asset’s cost), removing it will have little to no impact on Net PP&E (net book value is zero in that case). However, if an asset still had an undepreciated portion, disposing of it will reduce Net PP&E. (For instance, selling a machine with $20,000 net book value will cut Net PP&E by $20,000.) Companies may dispose of assets that are old, no longer needed, or replaced by newer assets; this keeps the PP&E account up-to-date with only active, usable assets.

It’s worth noting that land is a special case in PP&E: land is not depreciated. Therefore, land remains on the balance sheet at its original cost (and is part of Gross and Net PP&E without depreciation applied). Other assets like buildings, machinery, and equipment depreciate over time, so their net values decline as accumulated depreciation grows.

Why Net PP&E Is Important in Financial Analysis

Net PP&E is more than just an accounting number – it provides valuable insights into a company’s operations and financial health. Here are a few reasons why Net PP&E is important:

-

Indicator of Long-Term Investment: Net PP&E reflects the scale of a company’s investment in long-term tangible assets that are critical for operations. A high Net PP&E means the company has substantial infrastructure and equipment supporting its business. This is common in capital-intensive industries (manufacturing, utilities, transportation, etc.), where large PP&E balances are needed to generate revenue. For example, an oil company or automobile manufacturer will show a much larger net PP&E than a software or consulting firm. Analysts consider Net PP&E to understand how much the company has tied up in its physical operations and whether that aligns with its industry norms and strategy.

-

Asset Age and Condition (Quality of Assets): Comparing Gross PP&E to Net PP&E can hint at the age and condition of assets. If Net PP&E is significantly lower than Gross PP&E, it means a large portion of the assets’ cost has been depreciated – the assets might be older or heavily used. Conversely, a Net PP&E close to the gross value suggests newer assets (little depreciation so far). This is useful in assessing if the company may need to replace or upgrade assets soon. A steadily declining Net PP&E (without new CapEx) signals that assets are aging and being used up, which could necessitate future capital expenditures to maintain operations.

-

Impact on Capacity and Growth: Net PP&E plays a key role in a company’s capacity to produce goods or services. Increasing Net PP&E over time often indicates the company is expanding or investing in growth (buying new facilities, equipment, etc.), which could lead to higher future revenue. On the other hand, stagnant or decreasing Net PP&E might suggest the company is not reinvesting enough, potentially limiting future growth or signaling efficiency improvements (if production is maintained with fewer assets). In financial planning and analysis, PP&E trends are closely watched to ensure the company’s capital spending (CapEx) supports its strategic plans for growth.

-

Financial Health and Efficiency: Net PP&E is a key component in assessing financial health and operational efficiency. Investors and analysts often look at how effectively a company uses its fixed assets to generate sales. One common metric is fixed asset turnover (Revenue divided by Net PP&E) – a higher turnover means the company generates more revenue per dollar of PP&E, indicating efficient use of assets. A company with a very large PP&E but low output might have its capital tied up in under-utilized assets, which is a red flag for efficiency. Thus, Net PP&E helps evaluate whether the asset base is productive.

-

Investor and Lender Insight: Investors care about Net PP&E because it can signal whether a company is keeping its asset base modern and adequate for its needs. Outdated or poorly maintained equipment can hurt a company’s productivity and profitability. For instance, if a factory is using old machines that slow down production, the company’s profits may suffer – a situation evident if Net PP&E is low due to assets being fully depreciated and not replaced. Savvy investors study PP&E and CapEx trends to determine if the company’s assets are up-to-date, efficient, and capable of supporting future profits. Lenders also look at PP&E since these assets can serve as collateral for loans, and a solid asset base can improve a company’s borrowing capacity (though this strays into credit analysis, it underscores PP&E’s significance).

In summary, Net PP&E is an important figure on the balance sheet that represents the ongoing value of a company’s fixed assets after depreciation. It is calculated as Gross PP&E minus Accumulated Depreciation, with adjustments for new capital expenditures and asset disposals over time. This number is vital for financial analysis because it reveals how much of the company’s capital is invested in supporting its operations, how old or new its asset base is, and whether the company is maintaining and expanding the infrastructure needed for future success. By monitoring Net PP&E and its components, a finance team can better understand the company’s long-term asset management strategy and make more informed decisions regarding capital budgeting, asset replacement, and evaluating the company’s operational efficiency.