A guide to the tangible, long-lived assets essential for a company's operations, and how they are accounted for on the balance sheet.

Pennies don't fall from heaven, they have to be earned here on earth.

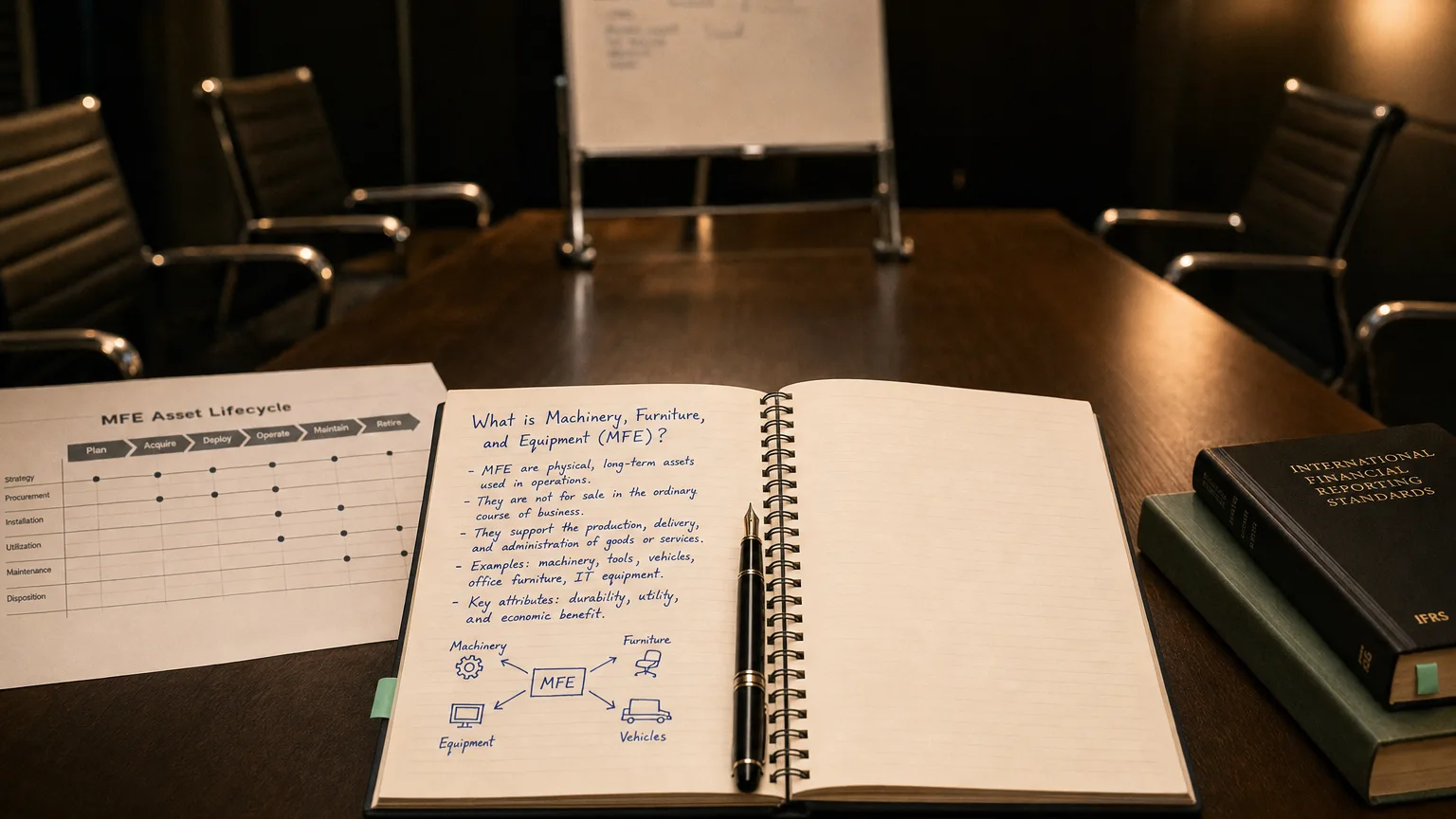

In accounting, machinery, furniture, and equipment (MFE) are tangible, long-lived assets used in a company’s operations. They fall under the broader category of Property, Plant, and Equipment (PPE)—assets held for use in producing goods or services over more than one accounting period. In other words, MFE are fixed assets that are not intended for resale and are expected to provide economic benefits to the business for multiple years.

What are Machinery, Furniture, and Equipment?

This category covers the physical tools a business uses to operate. It is typically broken down into three main types:

“Pennies don’t fall from heaven, they have to be earned here on earth.”

— Margaret Thatcher, Prime Minister of the United Kingdom Speech to the Conservative Party Conference (1979)

- Machinery: Includes heavy-duty production machines, industrial tools, and factory equipment. For example, an assembly line robot in a car factory or a large printing press for a newspaper.

- Furniture: Long-term office and workspace furnishings. This includes items like desks, chairs, filing cabinets, conference tables, and retail display fixtures.

- Equipment: A broad category for general operational devices and vehicles. Common examples are computers, servers, printers, hand tools, forklifts, and company delivery vans.

Accounting Treatment of MFE

The accounting for these assets follows a specific life cycle on the company’s books, from purchase to disposal.

The Three Key Stages of MFE Accounting

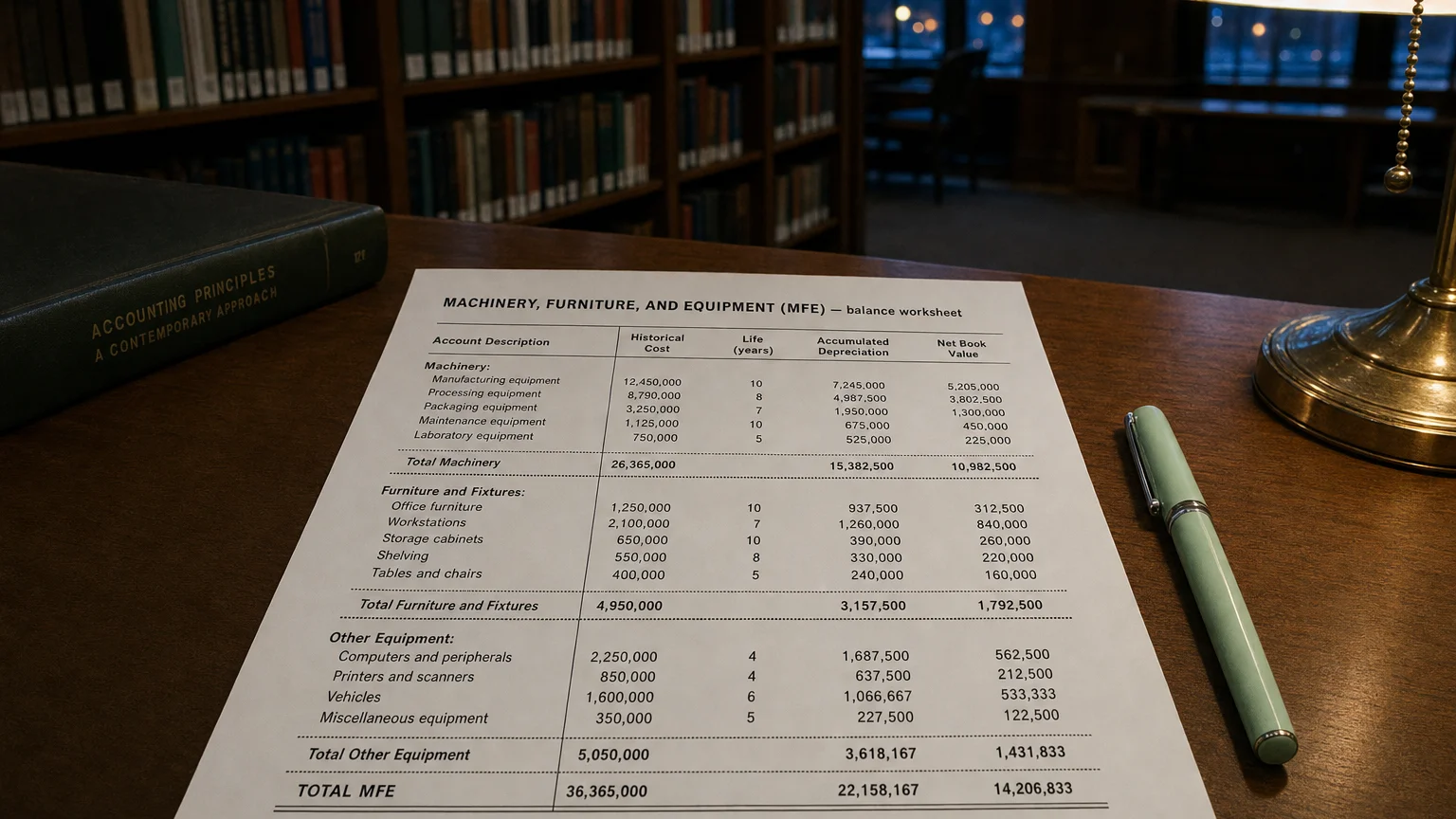

- 1. Capitalization: When MFE is purchased, its cost (including purchase price, shipping, and installation) is capitalized, meaning it is recorded as a non-current asset on the balance sheet rather than being expensed immediately. Companies often set a capitalization threshold, expensing smaller purchases.

- 2. Depreciation: Because these assets are used over multiple years, their cost is systematically allocated as an expense over their useful life. This non-cash charge, known as depreciation expense, is recorded on the income statement each period, and it reduces the asset’s value on the balance sheet.

- 3. Impairment: If an event occurs that suggests an asset’s value has permanently dropped (e.g., it becomes obsolete or is damaged), the company must test for impairment. If the asset’s book value is not recoverable, an impairment loss is recognized, writing down the asset’s value.

Importance in Operations and Financial Analysis

MFE are critical to both a company’s ability to function and how it is perceived by financial analysts.

Operational and Financial Role

Operational Backbone: MFE are the essential tools that enable a company to produce goods, deliver services, and run its administrative functions. Without them, most businesses could not operate.

Financing and Collateral: These fixed assets represent a significant investment and contribute to a company’s net worth. They can also be used as collateral to secure loans, improving a company’s access to financing.

Analysts track a company’s investment in MFE to gauge its efficiency. A key metric is the fixed asset turnover ratio (Net Sales ÷ Average Net PP&E). This ratio measures how effectively a company is using its fixed assets to generate revenue. A high ratio suggests efficient use of machinery and equipment, while a low ratio may indicate under-utilization or inefficiency.

Q · 01What is Machinery Furniture Equipment?+