A guide to how land and the enhancements made to it are treated as separate assets with very different accounting rules, especially regarding depreciation.

Pennies don't fall from heaven, they have to be earned here on earth.

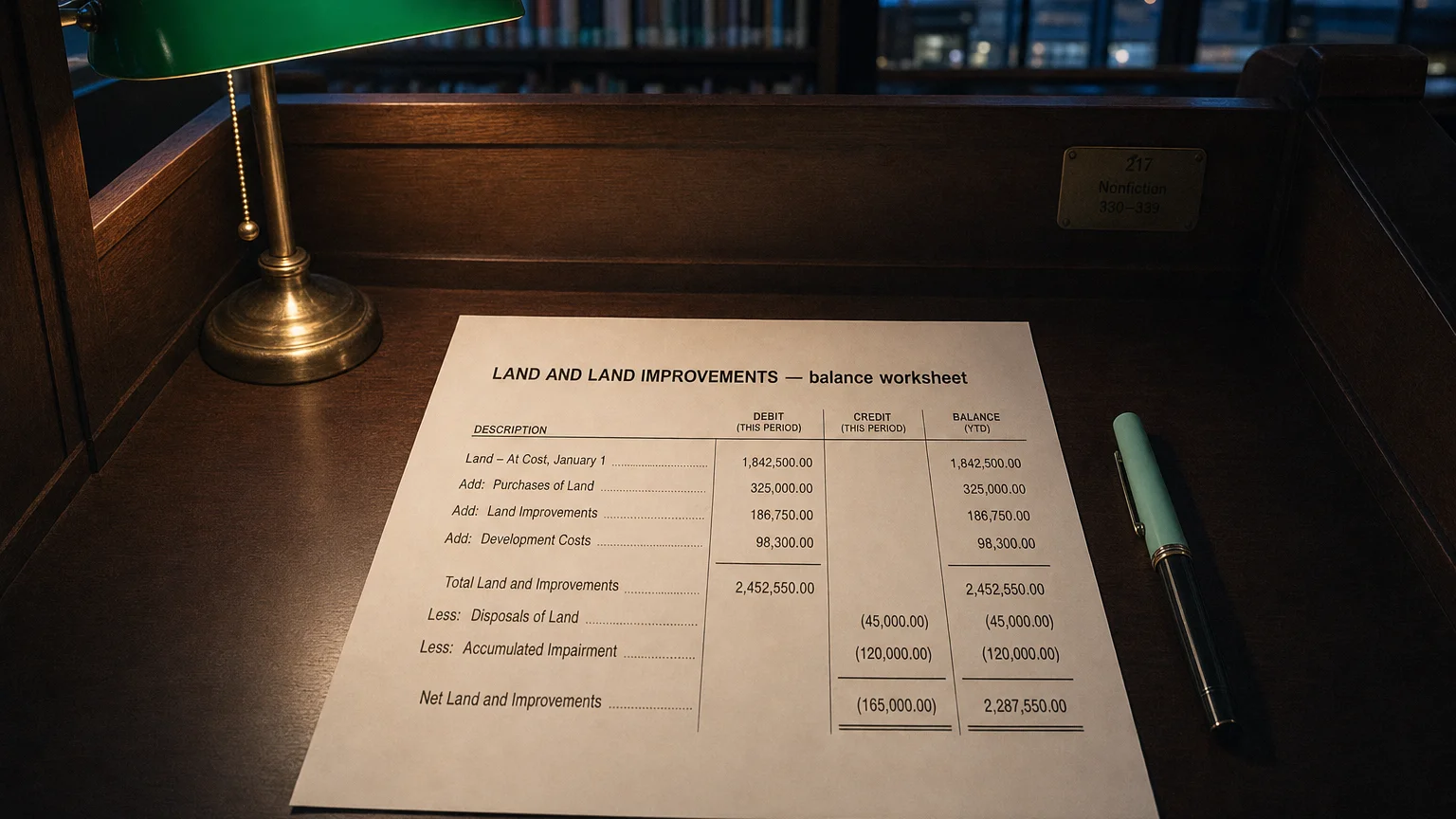

In accounting, Land is recorded as a long-term asset (part of Property, Plant, and Equipment) at its historical cost. Crucially, because land has an indefinite useful life, it is not depreciated. In contrast, Land Improvements are enhancements or additions to land that do have limited useful lives, such as fences, paved areas, and lighting. Because they wear out, land improvements are capitalized in a separate account from land and are depreciated over their estimated useful life.

Defining Land vs. Land Improvements

The key to this topic is understanding that although they are physically connected, land and its improvements are treated as two distinct assets for accounting purposes.

- Land: This account includes the purchase price of the land itself, plus any costs required to get it ready for its intended use, such as legal fees, title insurance, and costs for grading or clearing old buildings.

- Land Improvements: This is a separate asset account for additions to the land that will deteriorate over time. Common examples include fences, gates, paving for parking lots and sidewalks, landscaping, irrigation systems, and outdoor lighting.

“Pennies don’t fall from heaven, they have to be earned here on earth.”

— Margaret Thatcher, Prime Minister of the United Kingdom (1979-1990) Speech at Lord Mayor’s Banquet, London (1979)

The Critical Accounting Difference: To Depreciate or Not?

The reason for separating land and land improvements is their different treatment regarding depreciation, which is driven by their useful lives.

The Fundamental Rule

- Land is Non-Depreciable: Land is considered to have an unlimited useful life. It does not wear out or become obsolete. Therefore, accounting standards explicitly prohibit its depreciation. It remains on the balance sheet at its original historical cost.

- Land Improvements Are Depreciable: Enhancements like parking lots and fences do wear out over time. They have a finite useful life, so their cost must be allocated as an expense over the periods they provide a benefit. This is done through periodic depreciation.

This separation ensures that the financial statements accurately reflect the consumption of assets, in line with the matching principle.

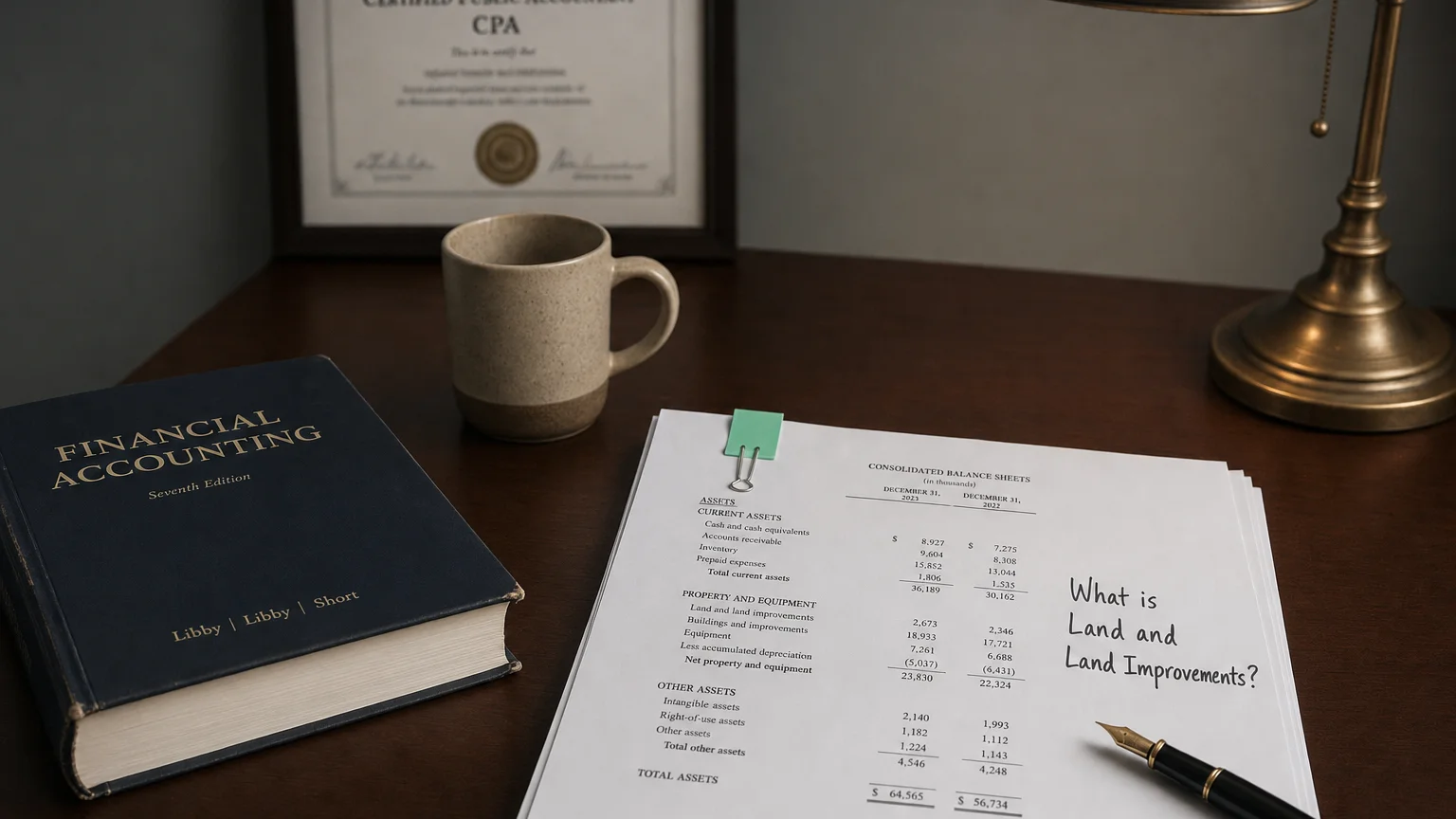

Balance Sheet Presentation

On a company’s balance sheet, you will see the different treatments reflected in how these assets are presented, typically within the Property, Plant, and Equipment (PPE) section.

Balance Sheet Excerpt

A company might show the following under its non-current assets:

Property, Plant, and Equipment:

- Land: $500,000

- Land Improvements: $100,000

- Less: Accumulated Depreciation - Land Improvements: ($40,000)

In this case, the net book value of the land improvements is 500,000.

Q · 01What is Land And Improvements?+