Investment Properties is a financial concept covered in this article. Real Estate Held for Rental Income or Capital Appreciation

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

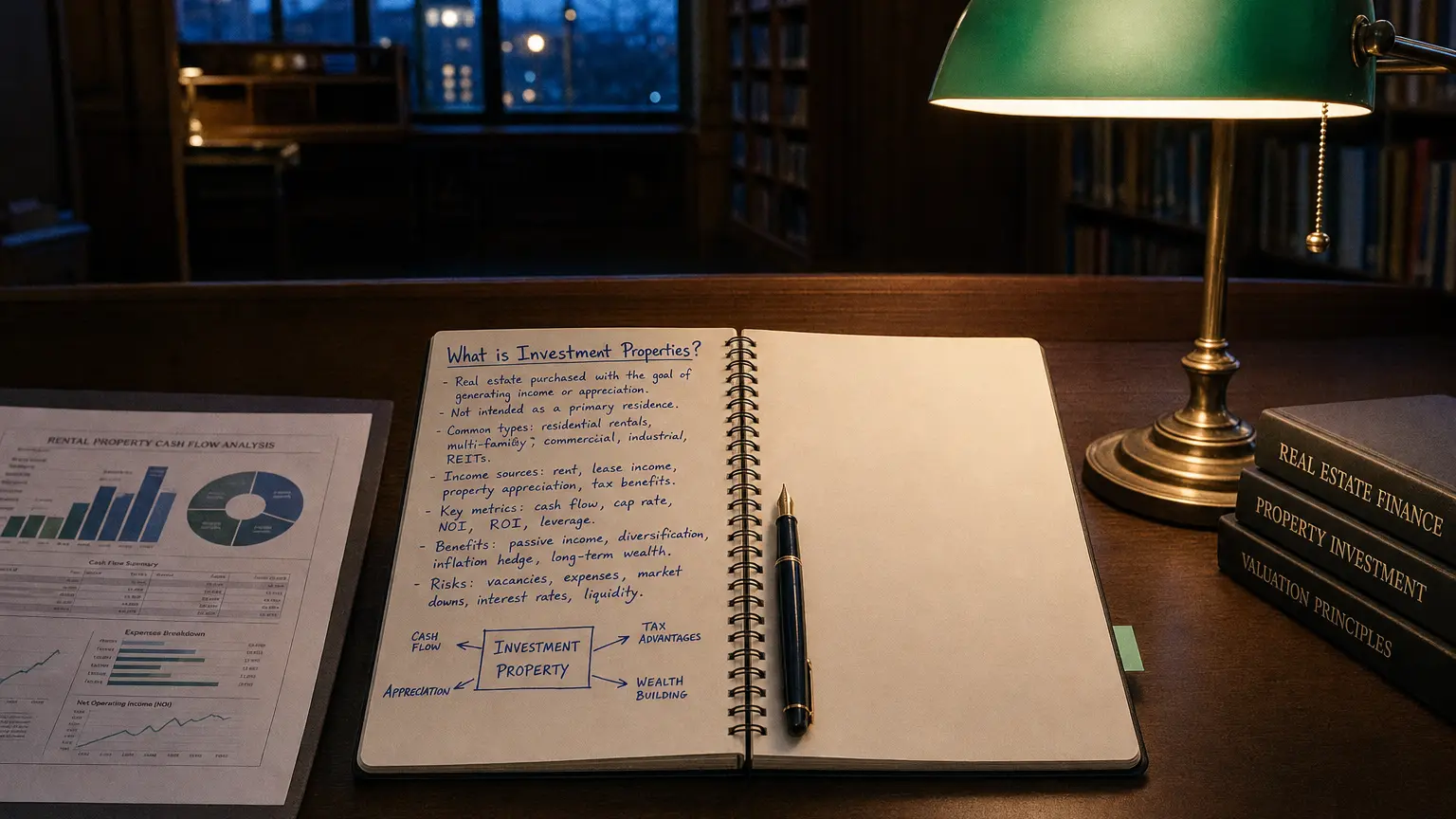

Investment Properties are real estate assets (land or buildings) held by a company to earn rentals, for capital appreciation, or both, rather than for use in production, supply of goods/services, or administrative purposes. Under IFRS (IAS 40), these properties are accounted for separately from owner-occupied property (PP&E), with unique measurement and recognition options.

Definition and Scope

Investment Properties under IAS 40 include:

- Land held for long-term capital appreciation

- Land held for undetermined future use

- Buildings leased out under operating leases

- Buildings vacant but held for future leasing

- Properties under development for future investment use

Excluded: Owner-occupied (PP&E), property for sale in ordinary course (inventory), or under construction for third parties.

US GAAP has no equivalent category—all treated as PP&E under ASC 360.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Accounting Models

IAS 40 offers two models (policy choice, applied consistently):

Fair Value Model (Preferred by many)

- Measured at fair value each period

- Gains/losses recognized in profit or loss

- No depreciation

- Fair value reflects market conditions and highest/best use

Cost Model

- Carried at cost less accumulated depreciation/impairment

- Same as PP&E

- Fair value disclosed in notes

Transfers between categories trigger remeasurement.

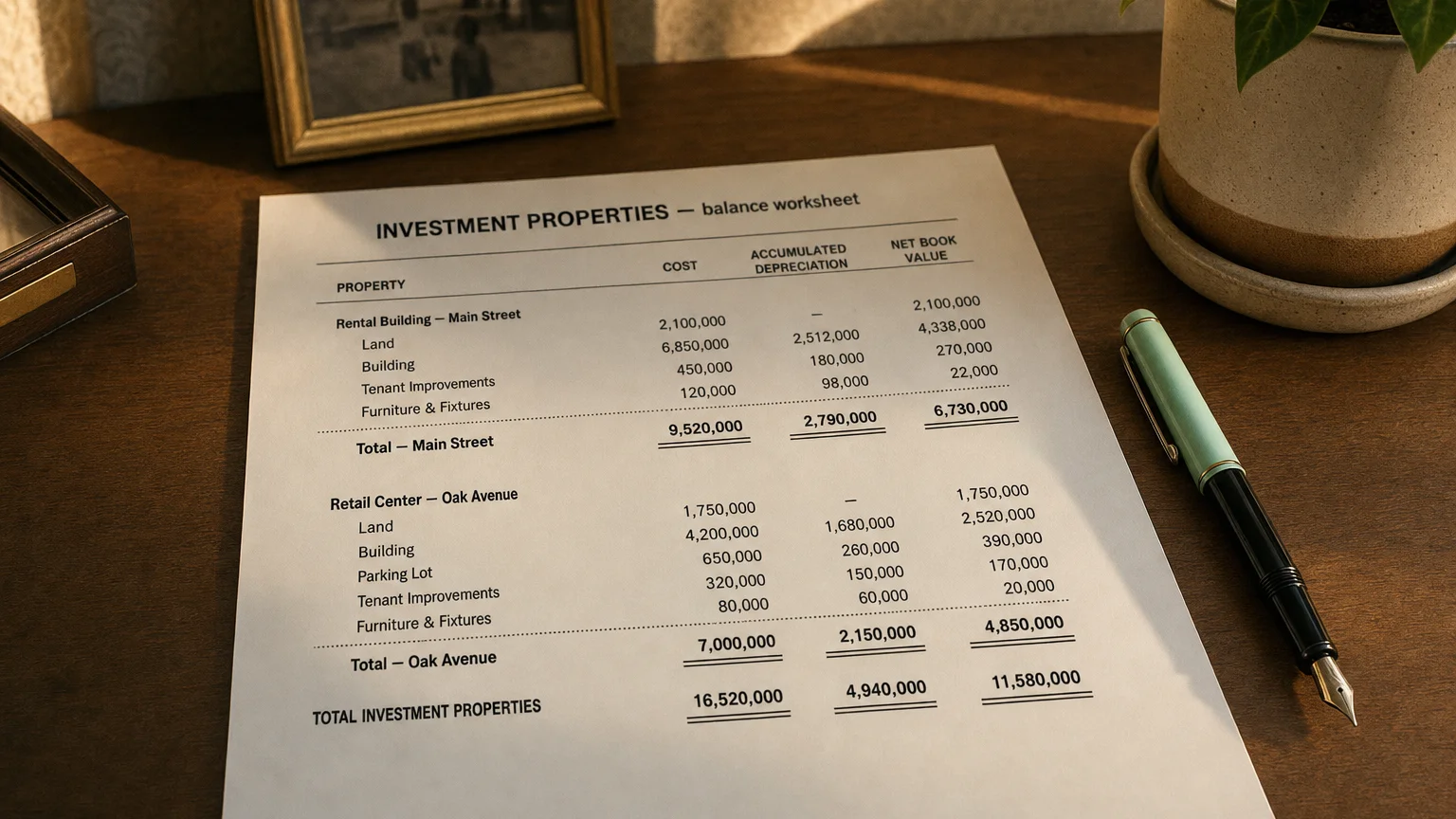

Balance Sheet Presentation

Under non-current assets as:

- ‘Investment Properties’

- ‘Investment Property’

- Fair value model: Single line at fair value

- Cost model: Gross cost less depreciation/impairment

- Separate from owner-occupied PP&E

Footnotes detail model used, valuation method, and rollforward.

Valuation and Changes

- Fair value typically by independent appraisers

- Based on market evidence, discounted cash flows, or capitalized income

- Changes in fair value directly impact profit or loss (fair value model)

- Rental income recognized separately in P&L

Common Industries

- Real estate investment companies (REITs)

- Property developers holding completed assets

- Retail/hospitality groups with leased properties

- Insurance and pension funds

- Companies with surplus real estate

Analytical Implications

Investment properties affect analysis by:

- Introducing earnings volatility (fair value changes)

- Reflecting real estate market exposure

- No depreciation charge (fair value model boosts reported profits)

- Higher asset values vs. cost model peers

- NAV (net asset value) relevance for property companies

Fair value gains can mask underlying operational performance.

Q · 01What is Investment Properties?+