is a financial concept covered in this article. Long-Term Liabilities Tied to Assets or Businesses Classified as Held for Sale

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

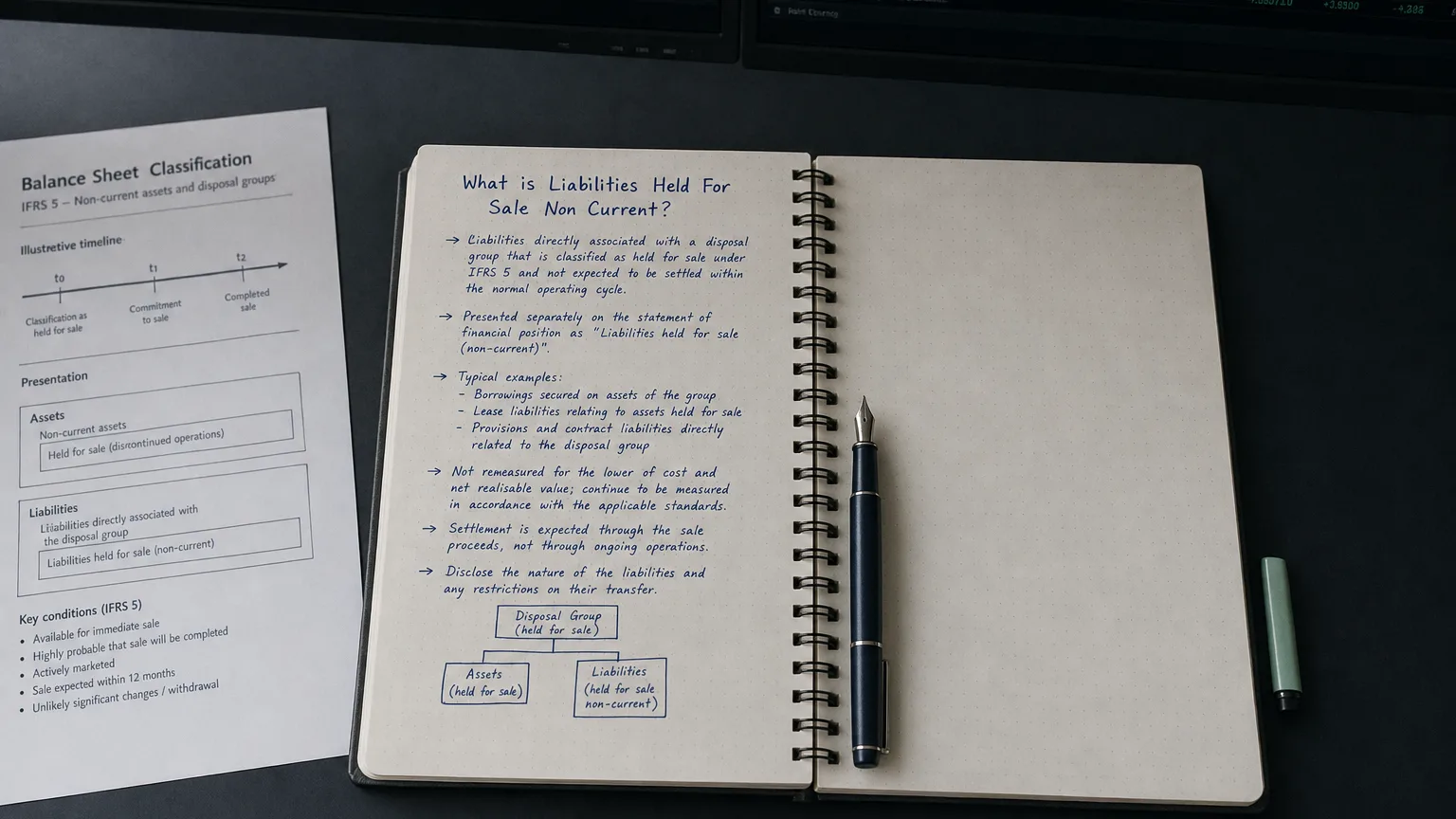

Liabilities Held for Sale Non Current represent obligations that were originally classified as non-current (due beyond 12 months) but are now part of a disposal group or directly associated with non-current assets held for sale. When a company commits to selling a business unit, division, or major asset, these liabilities are reclassified and presented separately on the balance sheet under accounting rules (IFRS 5 and US GAAP).

Definition and Purpose

This item includes non-current liabilities that will transfer with a disposal group or asset the company plans to sell. The ‘non-current’ tag reflects their original maturity, even though the pending sale makes the group current in substance.

Common examples: long-term borrowings secured by the asset, deferred liabilities, provisions, or pension obligations related to the business being divested.

Reclassification signals strategic restructuring—separates exiting obligations from continuing operations.

Classification Criteria

“No asset is so good that it can’t become a bad investment if bought at too high a price, and there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Founder & Co-Chairman, Oaktree Capital Management The Most Important Thing (2011)

Held-for-sale status requires:

- Asset/disposal group available for immediate sale.

- Sale highly probable within one year.

- Active marketing at reasonable price.

- Management committed to plan.

Once met, the entire disposal group’s assets and liabilities are reclassified separately—no offsetting allowed.

Balance Sheet Presentation

Under IFRS 5 and US GAAP:

- Presented as separate sections: ‘Assets held for sale’ and ‘Liabilities held for sale’.

- Many reports use ‘Non Current’ suffix to preserve original maturity distinction.

- IFRS: Typically current in presentation; no restatement of comparatives.

- US GAAP: May re-present prior periods for discontinued operations.

Major classes disclosed on face or in footnotes.

Measurement Rules

Key differences from assets:

- Liabilities: Remain at carrying amount—no fair value less costs to sell.

- Assets: Measured at lower of carrying amount and fair value less costs to sell.

- Impairment tested for disposal group as a whole.

- Continue recognizing interest/expenses on these liabilities.

No depreciation/amortization on related held-for-sale assets while classified.

Analytical Importance

This line item provides insight into:

- Upcoming divestitures or portfolio streamlining.

- Impact on future leverage (liabilities removed post-sale).

- Cleaner view of core ongoing operations.

- Potential gains/losses on disposal.

Adjust ratios (debt-to-equity, net debt) by excluding these items for continuing business analysis.

Q · 01What is Liabilities Held For Sale Non Current?+