Estimated Non-Current Liabilities for Probable Future Obligations with Uncertain Timing or Amount

Survival comes first, truth, understanding, and science later.

Long Term Provisions are balance sheet liabilities representing the company’s best estimate of future economic outflows for obligations that are probable, arise from past events, and are expected to settle beyond 12 months. These provisions reflect prudent recognition of long-term risks and commitments where timing or exact amount is uncertain, in line with standards like IAS 37 (IFRS) and ASC 450 (US GAAP).

Definition and Core Characteristics

Long Term Provisions are recognized when a company has a present obligation (legal or constructive) as a result of a past event, it is probable that an outflow of resources will be required to settle it, and a reliable estimate can be made of the amount.

The ‘long-term’ classification applies when settlement is expected after more than one year or one operating cycle. These differ from definite liabilities (e.g., loans) due to inherent uncertainty in timing or amount.

Provisions embody the prudence concept—recognizing expected losses early while gains only when realized.

Common Types of Long Term Provisions

“Survival comes first, truth, understanding, and science later.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Skin in the Game: Hidden Asymmetries in Daily Life (2018)

Typical long-term provisions include:

- Decommissioning, restoration, and environmental rehabilitation costs (e.g., oil rig dismantling, mine closure)

- Extended product warranties or guarantees beyond one year

- Restructuring costs (e.g., long-term severance or site closure obligations)

- Asset retirement obligations (AROs)

- Provisions for onerous contracts (unavoidable costs exceeding benefits)

- Long-term litigation or legal claims expected to settle far in the future

- Certain employee benefit obligations not classified as pensions

Industry examples: Mining companies provision for site restoration; manufacturers for multi-year warranties; energy firms for nuclear decommissioning.

Recognition Criteria

A provision is recognized only if all three conditions are met:

- Present obligation (legal: from contract/law; constructive: from established practice creating valid expectation)

- Probable outflow (>50% likelihood under IFRS; >likely than not under US GAAP)

- Reliable estimate of the amount

If any criterion is missing, the item is a contingent liability (disclosed in notes, not recognized).

Constructive obligations often arise from company policy or public statements creating stakeholder expectations.

Measurement and Subsequent Treatment

Provisions are measured at the best estimate of expenditure required to settle the obligation:

- Expected value method (weighted average) for large populations

- Most likely amount for single obligations

- Discounted to present value using pre-tax rate reflecting time value and risks (unwinding increases finance costs over time)

- Reassessed at each reporting date—changes recognized in profit or loss

Utilization reduces the provision; unused amounts reversed to income.

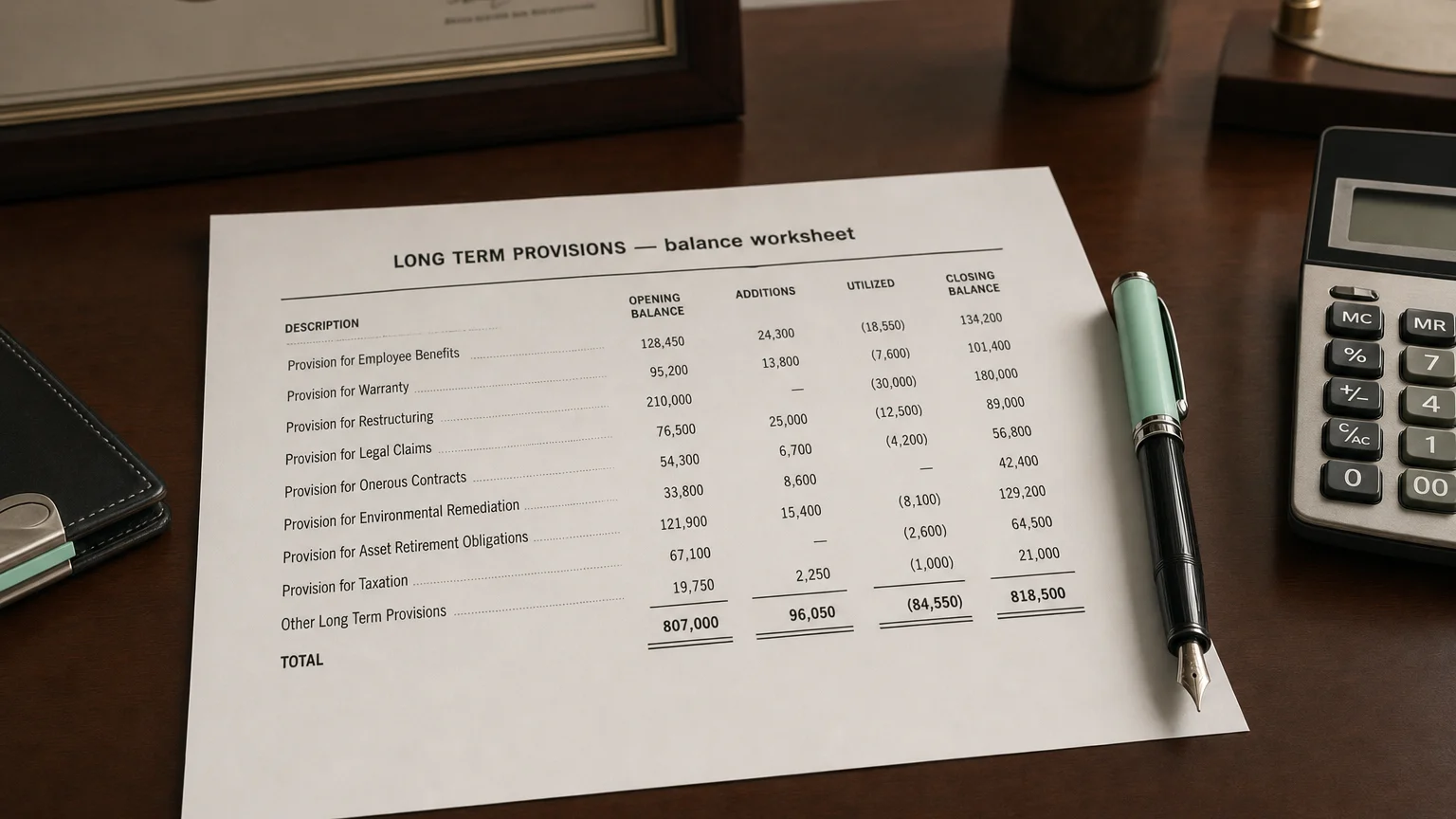

Balance Sheet and Disclosure

Presented as a separate line under non-current liabilities (or aggregated with disclosure in notes).

Extensive note disclosures required: nature, expected timing, uncertainties, reimbursement expectations, movements during the period.

Movements table typically shows opening balance, additions, utilizations, reversals, unwinding, and closing balance.

Analytical Considerations

Long term provisions affect analysis in several ways:

- Increase reported liabilities and reduce net assets/equity

- Non-cash expense at creation impacts profitability

- Subjective estimates can be used for earnings management (big bath provisions or releases)

- Discount unwinding creates ongoing finance costs

- Signal underlying operational risks or legacy issues

Sharp increases may indicate emerging risks; frequent reversals warrant scrutiny for quality of earnings.

Q · 01What is Long Term Provisions?+