Long-Term Portion of Unearned Revenue Expected to Be Recognized Beyond 12 Months

The stock market is filled with individuals who know the price of everything but the value of nothing.

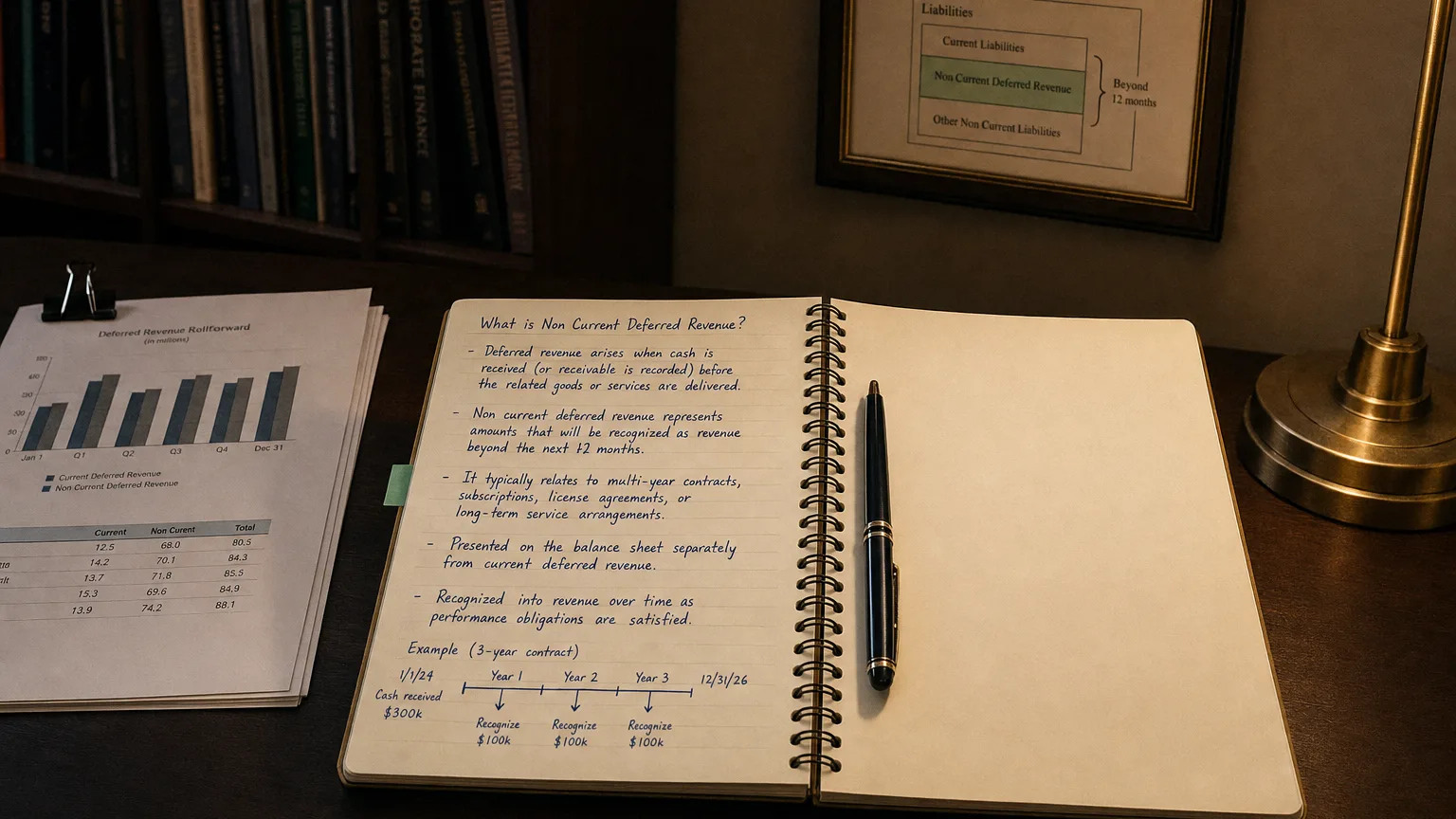

Non Current Deferred Revenue (also called Long-Term Unearned Revenue or Long-Term Deferred Income) is the portion of advance payments received from customers that a company expects to recognize as revenue more than 12 months after the balance sheet date. It represents contractual obligations to deliver goods or services in the future, classified as non-current to match the timing of performance.

Definition and Core Concept

Non Current Deferred Revenue arises when a company receives payment upfront for goods or services to be provided over an extended period. Under revenue recognition standards, revenue is earned only when performance obligations are satisfied.

The total deferred revenue is split into current (expected to be recognized within 12 months) and non-current portions based on the expected timing of delivery.

It is a liability because the company owes future performance—if not delivered, cash may need to be refunded.

Common Sources

- Multi-year software licenses and SaaS subscriptions

- Extended maintenance/support contracts

- Long-term service agreements (e.g., telecom, warranty extensions)

- Prepaid insurance premiums covering future periods

- Upfront fees for long-term memberships or loyalty programs

- Advance billings on long-term projects (construction, consulting)

High-growth SaaS and subscription companies often show significant non-current deferred revenue, signaling strong future revenue visibility.

“The stock market is filled with individuals who know the price of everything but the value of nothing.”

— Philip Fisher, Author, Common Stocks and Uncommon Profits Common Stocks and Uncommon Profits (1958)

Accounting Treatment

Under ASC 606 / IFRS 15:

- Record contract liability when cash received before transferring control

- Allocate transaction price to distinct performance obligations

- Classify based on expected satisfaction timing

- Recognize revenue as obligations are met (over time or point in time)

- Reassess classification each period

No accretion unless significant financing component exists.

Balance Sheet Presentation

Appears under non-current liabilities as:

- ‘Non Current Deferred Revenue’

- ‘Long-Term Deferred Revenue’

- ‘Long-Term Unearned Revenue’

- Sometimes aggregated in ‘Other Non Current Liabilities’ with note disclosure

Footnotes provide rollout schedule (amounts expected to be recognized in future years).

Analytical Importance

This item is valuable for:

- Assessing revenue visibility and backlog quality

- Evaluating business model sustainability (recurring vs. one-time)

- Forecasting future revenue growth

- Comparing cash collections vs. recognized revenue

- Identifying potential earnings pressure if new bookings slow

Declining non-current deferred revenue may signal weakening future demand or shorter contract durations.