An essential guide to understanding unearned revenue as a short-term liability and how it impacts financial statements.

It is all about redundancy. Nature likes to overinsure itself.

Current deferred revenue (also known as unearned revenue) refers to money that a company has received in advance for goods or services that it has not yet delivered, and which it expects to deliver within the next 12 months. In other words, it’s payment collected upfront from customers for work the company still owes. Until the company fulfills its obligation to the customer, this advance payment is not recorded as actual revenue. Instead, it appears on the balance sheet as a liability (a debt the company owes in the form of goods or services). This entry ensures the company’s financial statements remain accurate and in line with standard accounting principles.

Why Deferred Revenue is a Liability (Significance in Accounting)

Even though it contains the word “revenue,” deferred revenue isn’t real earned revenue yet – it represents an obligation. According to accrual accounting and the revenue recognition principle, revenue should be recognized only when it is earned (i.e. when goods or services are delivered), not when cash is received. This is why deferred revenue is initially recorded as a liability. The company has an obligation to deliver the product or service in the future, or else return the payment. If the company fails to deliver what was promised, it would have to refund the customer’s money – reinforcing why the upfront payment is considered a liability until the obligation is met. Recording deferred revenue properly prevents a company from overstating its income by prematurely counting unearned money as revenue. It ensures the financial statements reflect the company’s true earned revenue and remaining obligations at any given time.

In practical terms, deferred revenue helps align revenue with the period it is earned, following the matching and revenue recognition principles. This practice provides transparency and accuracy in financial reporting. For managers and analysts, deferred revenue is significant because it indicates future revenue the company can expect and the workload or services it still must deliver. A large deferred revenue balance can signal strong sales and cash inflows, but it also means the company has a lot of future work or deliveries owed to customers.

Current vs. Non-Current Deferred Revenue

Deferred revenue on the balance sheet is often split into current and non-current portions, depending on when the company expects to fulfill the obligation and earn the revenue.

-

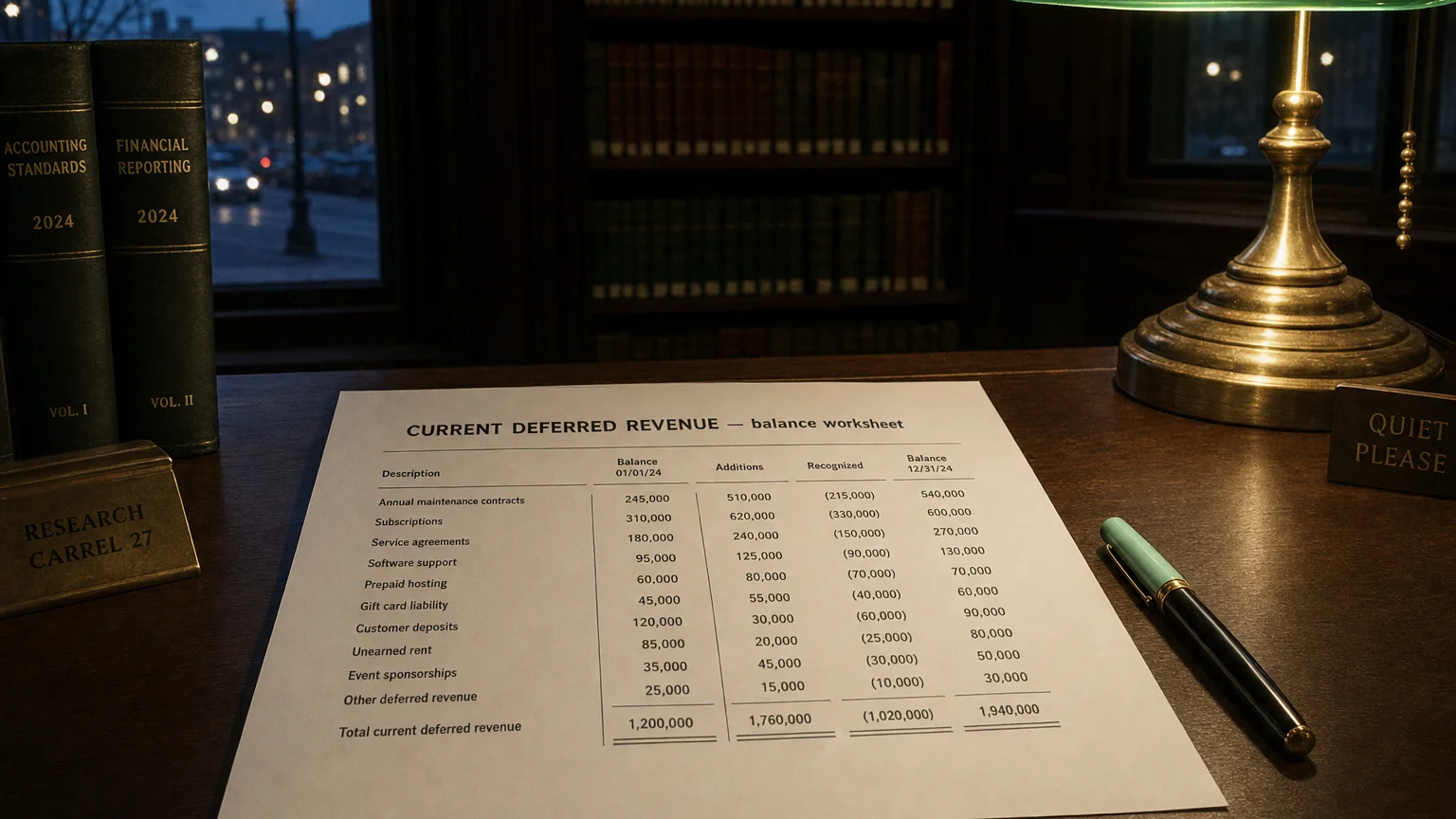

Current Deferred Revenue: This is the portion of deferred revenue that will be earned within the next 12 months. It is listed under current liabilities on the balance sheet. In financial reports, it might be labeled as “Deferred Revenue (Current)” or “Unearned Revenue – Short Term.” For example, if a customer pays upfront for a service that will be delivered over the next six months, that payment is recorded entirely as current deferred revenue since the earning of that revenue will occur within the year.

-

Non-Current Deferred Revenue: This represents deferred revenue for goods/services that will be delivered beyond 12 months in the future. It appears under long-term liabilities. For instance, if a company sells a two-year service contract and is paid in advance, the portion of the service to be provided in the second year is classified as non-current deferred revenue (since that part will not be earned until more than a year out).

By separating current vs. non-current deferred revenue, financial statements give a clearer picture of when the company’s obligations will be satisfied. Current deferred revenue indicates income that will be recognized in the short term (within one operating cycle), while non-current deferred revenue shows obligations stretching into later periods. Together, they total the company’s overall deferred (unearned) revenue. This distinction is important for analyzing a company’s short-term liquidity and long-term obligations.

How Deferred Revenue is Recorded and Recognized

When a company receives an advance payment from a customer, it must follow specific steps to record this deferred revenue and later recognize it as actual revenue. Below is the typical process:

-

Receive Advance Payment and Record a Liability: When the cash comes in for an undelivered product or service, the company increases Cash (asset) and simultaneously increases Deferred Revenue (liability) on the balance sheet. The deferred revenue is classified into current or long-term based on when the service/product will be delivered. If the obligation will be delivered within 12 months, record it as a current deferred revenue liability; if delivery extends beyond 12 months, record it as a long-term (non-current) deferred revenue liability. For example, if a customer pays $600 for a two-year subscription (covering two years at $300 each), the company would debit Cash $600, credit $300 to Current Deferred Revenue, and credit $300 to Deferred Revenue (Non-Current) to split the liability into short-term and long-term portions.

-

Maintain Deferred Revenue on the Balance Sheet: After the initial recording, the deferred revenue remains on the balance sheet as a liability until the company starts delivering the product or service. During this period, no revenue is shown on the income statement for this advance payment because it has not been earned yet. The full amount is essentially “on hold” in the deferred revenue account, reflecting the company’s obligation to the customer.

-

Recognize Revenue Over Time as Earned: As the company delivers the product or performs the service, it earns a portion of the revenue. At each delivery milestone or over each accounting period, the company reduces (debits) the Deferred Revenue liability and recognizes (credits) Revenue on the income statement for the amount earned in that period. This transfer moves the money from the liability side of the balance sheet into actual earned income. The recognition can be done all at once (for example, after a single deliverable) or gradually over time (for example, monthly for a subscription service), depending on how the goods/services are provided. Each recognition entry decreases the deferred revenue balance and increases reported revenue. This process continues until the company has delivered all promised goods/services and the entire deferred amount has been recognized as revenue.

Throughout this process, no new cash is coming in during the revenue recognition stage – the cash was received upfront. What changes is the allocation of that upfront payment from a liability to earned revenue as time passes or as obligations are met. This ensures that the company’s income statement only reflects revenue actually earned in the period, while the balance sheet shows the remaining liability for what’s still owed to customers.

Example: Deferred Revenue in Action (Subscription Service)

To illustrate, let’s consider a simple example of how current deferred revenue works in practice:

-

Initial Payment (Day 1): Suppose a magazine publisher sells a 12-month subscription to a customer for $120 upfront (covering one year of magazines). The customer pays the full $120 in advance. At the time of this payment, the company will record an increase in Cash by $120 and simultaneously record $120 in Deferred Revenue (since the magazines for the year are not delivered yet). The $120 is categorized as current deferred revenue because all magazines will be delivered within the next 12 months. On the balance sheet, $120 is added to current liabilities under deferred revenue, reflecting the publisher’s obligation to deliver magazines in the future.

-

During the Year (Earning the Revenue): Now, each month when the publisher delivers one issue of the magazine, it has fulfilled 1/12 of the annual service. At the end of each month, the company will recognize $10 of actual revenue (the portion earned for delivering that month’s magazine) and reduce the deferred revenue liability by $10. In terms of a journal entry, the company debits Deferred Revenue $10 and credits Revenue $10 for each issue delivered. This reflects that $10 of the previously unearned amount is now earned in that month.

-

End of the Year: After 12 months (and 12 issues delivered), the company has delivered all magazines for the year. At this point, the entire $120 initially received has been recognized as revenue (earned) over the year, in $10 increments each month. The deferred revenue account has been brought down to $0 because there is no remaining undelivered service. The liability is fully satisfied. The income statement over the year would have incrementally reported those revenues, and the balance sheet at year-end no longer carries that $120 obligation. This pattern ensured the company’s income each month matched the service provided in that month, adhering to proper revenue recognition.

In summary, the above example shows how an upfront payment is deferred and then recognized gradually. The key takeaway is that until the company delivers on what the customer paid for, the money stays as a liability (deferred revenue). Only once the product/service is delivered does it officially become earned income.

Common Real-World Examples of Deferred Revenue

Many everyday business transactions result in deferred revenue. Here are a few common examples:

-

Subscription Services: Companies like streaming services or software providers often collect subscription fees upfront for a period of access (monthly, annual, etc.). For instance, a cloud software company might sell an annual license or SaaS subscription and receive payment in advance. That payment is recorded as deferred revenue and then recognized as income month-by-month as the service is provided.

-

Memberships and Season Passes: Gyms or clubs may sell annual memberships. The cash from a one-year gym membership paid in advance is deferred revenue, recognized gradually each month as the membership period passes. Similarly, theme parks selling season passes would treat the upfront fee as deferred revenue and recognize it over the season.

-

Airline Tickets and Event Tickets: When an airline sells a ticket or a concert promoter sells concert tickets in advance, the payment is unearned revenue until the flight takes place or the concert is held. The airline or event organizer carries the ticket sales as deferred revenue, then recognizes the revenue on the date of the flight or event when the service is delivered.

-

Insurance Premiums: Insurance companies often require prepayment for coverage (e.g. paying your car insurance premium for the next 6 months upfront). The insurer records the premium as deferred revenue and then earns the revenue each month as insurance coverage is provided. If the coverage is annual, the portion beyond 12 months would be long-term deferred revenue.

-

Gift Cards and Deposits: When a retailer sells a gift card, it receives cash now, but owes the customer merchandise (or a service) later when the card is redeemed. Until the customer uses the gift card, the amount is deferred revenue on the retailer’s books. Similarly, any deposit a company takes (for a future service or as a down payment) is usually treated as deferred revenue until the product or service is delivered or the deposit is applied.

In each of these cases, the idea is the same – money now, work later. The company cannot count the money as revenue immediately; it must first fulfill the obligation. Only then does deferred revenue turn into real revenue on the income statement.

Key Takeaways

-

Definition: Deferred revenue (or unearned revenue) is cash received before a company has provided the goods or services. It is recorded on the balance sheet as a liability because the company still owes the customer that product/service.

-

“Current” Deferred Revenue: This term refers to the portion of deferred revenue that will be earned within the next 12 months, listed under current liabilities. Deferred revenue expected to be earned beyond one year is classified as a long-term liability.

-

Why It Matters: Listing deferred revenue as a liability ensures that a company follows accrual accounting principles, only recognizing revenue when it is actually earned (when the product/service is delivered). This prevents premature revenue recognition and keeps financial reports accurate and compliant with accounting standards.

-

Recording Deferred Revenue: When cash is received upfront, the entry is typically Debit Cash, Credit Deferred Revenue – increasing assets and increasing liabilities. No revenue is recorded at this point because nothing has been earned yet.

-

Revenue Recognition: As the company delivers the goods or performs the service over time, it recognizes revenue in that period and reduces the deferred revenue accordingly (Debit Deferred Revenue, Credit Revenue). Gradually, the liability is drawn down to zero as all obligations are fulfilled, and the cash collected earlier becomes earned income.

-

Real-World Insight: Deferred revenue is common in many industries (subscriptions, tickets, insurance, etc.) and is a sign of future revenue. A growing balance of deferred revenue can indicate strong sales of prepaid products or services, but it also represents a commitment to deliver on those sales in the future. Financial analysts watch deferred revenue because it affects a company’s liquidity and indicates how much revenue is “in the pipeline” to be recognized.

By understanding current deferred revenue, business students and junior analysts can better interpret balance sheets and appreciate how companies account for advance payments. It highlights the important principle that cash received is not always immediately revenue – only when the company has earned it by delivering value does it count as revenue. This ensures clarity and honesty in financial reporting, matching revenues with the periods in which they are actually earned and the corresponding efforts or deliveries are made.

Sources: Relevant information adapted from accounting educational resources and examples, ensuring the explanation aligns with general accounting principles and standards for revenue recognition.

Q · 01What is Current Deferred Revenue?+