Accounts Payable What It Is and Why It Matters

Accounts payable (AP) are short-term supplier debts recorded as current liabilities. Learn how AP affects cash flow, working capital, and financial analysis.

Overview

Accounts payable (AP) are short-term supplier debts recorded as current liabilities. Learn how AP affects cash flow, working capital, and financial analysis.

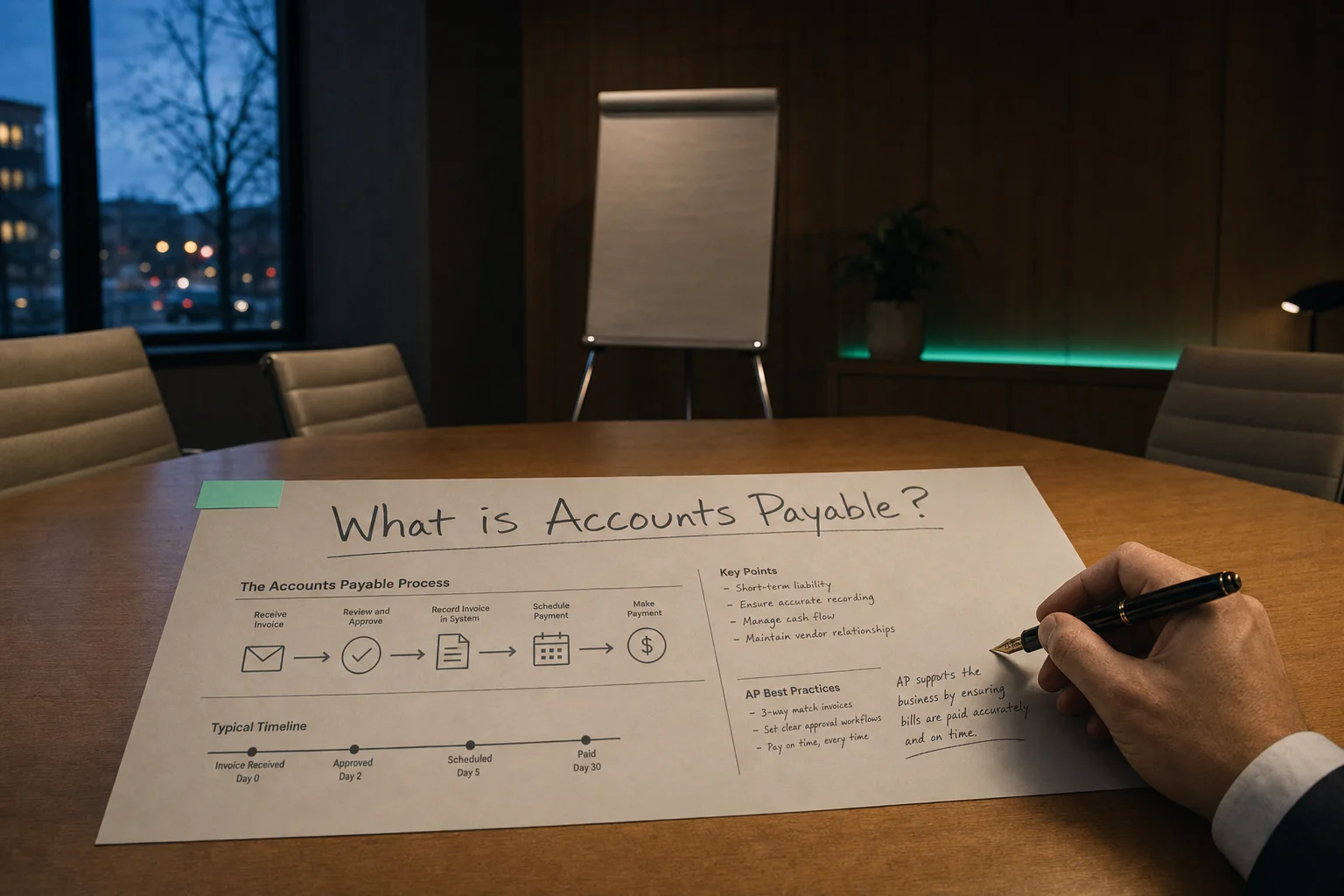

Accounts Payable (AP) represents the amounts a company owes to suppliers or creditors for goods and services purchased on credit. In simple terms, it is a short-term obligation to pay off these debts, usually within a few weeks or months (often 30 to 90 days). This item is commonly referred to as trade payables or simply "payables," indicating the outstanding bills the company needs to settle in the near term.

Understanding and Classifying Accounts Payable

On the balance sheet, accounts payable is listed under the current liabilities section. Current liabilities are debts or obligations due within one year (or one operating cycle), and AP typically falls well within this timeframe. It’s important to note that accounts payable is not an expense account on the income statement; instead, it’s a liability on the balance sheet that reflects amounts owed. This classification matters because AP directly affects measures of short-term financial health, like working capital and liquidity ratios.

What's Included in Accounts Payable?

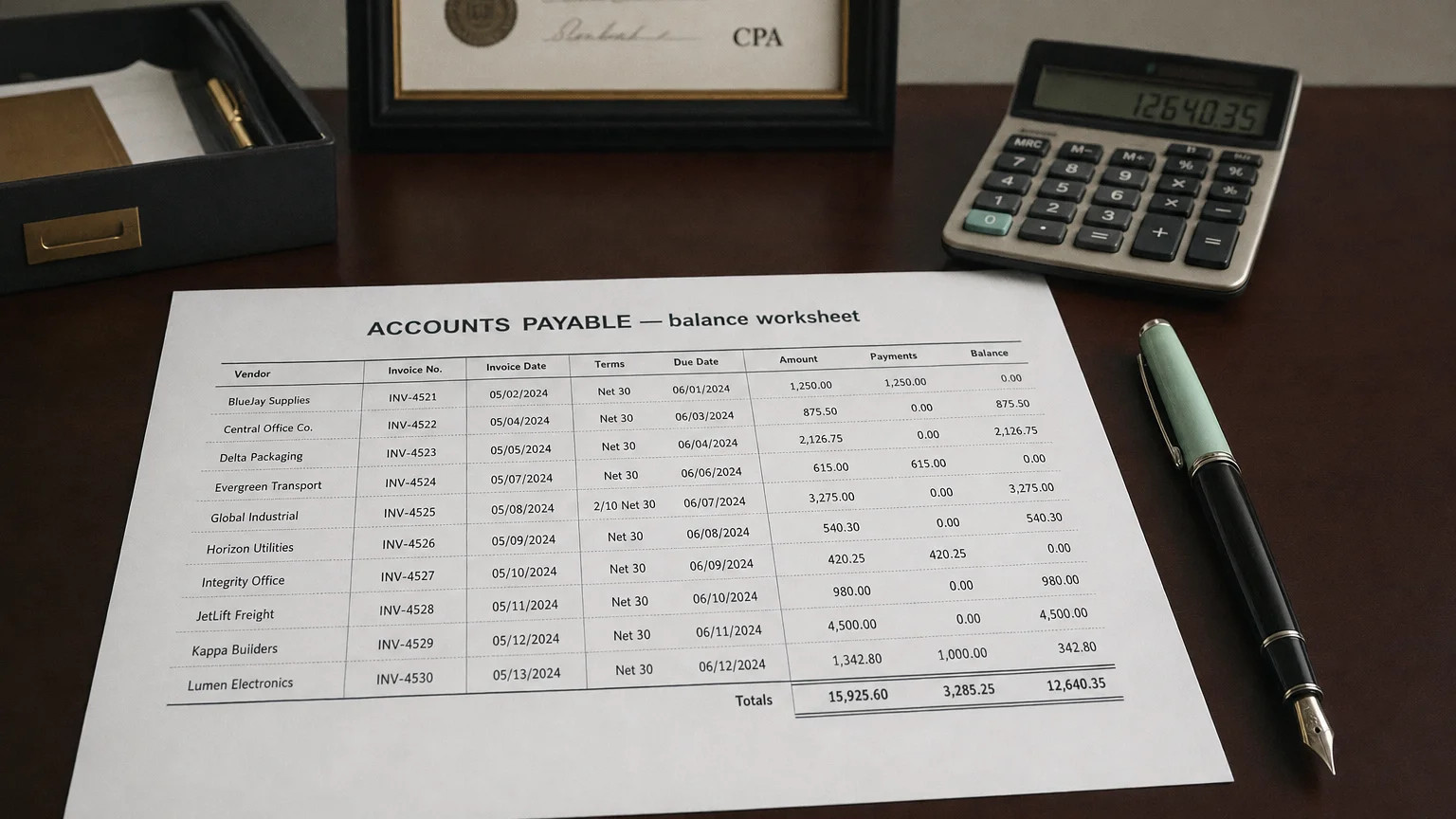

AP includes a variety of unpaid bills and invoices from normal business operations. Examples include supplier invoices for inventory, bills from service providers (like IT support or cleaning services), utility bills, and invoices for professional fees (legal or accounting).

Importance of Accounts Payable in Financial Analysis

"Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks."

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman's Letter 1985 (1985)

Accounts payable is more than just a list of bills; it plays a key role in analyzing a company's financial health and operations:

- Liquidity and Working Capital: As a major current liability, AP directly impacts the current ratio and working capital. Analysts examine AP levels to gauge if a firm can cover its short-term obligations with its current assets.

- Cash Flow Management: The timing of payments to suppliers affects cash flow. Delaying payments (increasing AP) can temporarily boost cash on hand and operating cash flow. However, a consistently rising AP balance might also signal that a company is experiencing financial stress.

- Vendor Relationships: Paying accounts payable on time is essential for maintaining good relationships with suppliers. Effective AP management can lead to favorable credit terms, such as longer payment periods or early payment discounts.

- Indicator of Financial Health: Trends in accounts payable are closely watched. Analysts calculate metrics like Days Payable Outstanding (DPO) to assess how quickly a firm pays its suppliers, which provides insight into its operational efficiency and liquidity.

Accounts Payable vs. Accrued Expenses

Both accounts payable and accrued expenses are current liabilities representing money a company owes, but they differ in timing and how they are recognized.

The Key Difference: The Invoice

Accounts Payable is recorded only when an invoice or bill is received from a supplier. The amount is definite and documented. In contrast, Accrued Expenses are recorded for costs that have been incurred but not yet billed. These are often estimates made at the end of an accounting period (e.g., wages earned by employees but not yet paid). The accrual is later adjusted when an actual bill arrives.

In summary, accounts payable are formal, invoice-backed obligations with exact amounts, whereas accrued expenses are informal, estimated liabilities for expenses incurred without a bill at the reporting date. Understanding this distinction is important for accurate financial reporting.