A comprehensive guide to the catch-all category for a company's miscellaneous short-term obligations on the balance sheet.

Know what you own, and know why you own it.

A company’s balance sheet often includes a line item called Other Current Liabilities. This section explains what that term means, what kinds of items it covers, why companies use this grouping, how it differs from other liabilities, and why it matters in financial analysis. We’ll also look at an example of how “Other Current Liabilities” appears on a balance sheet for clarity.

Definition of Other Current Liabilities

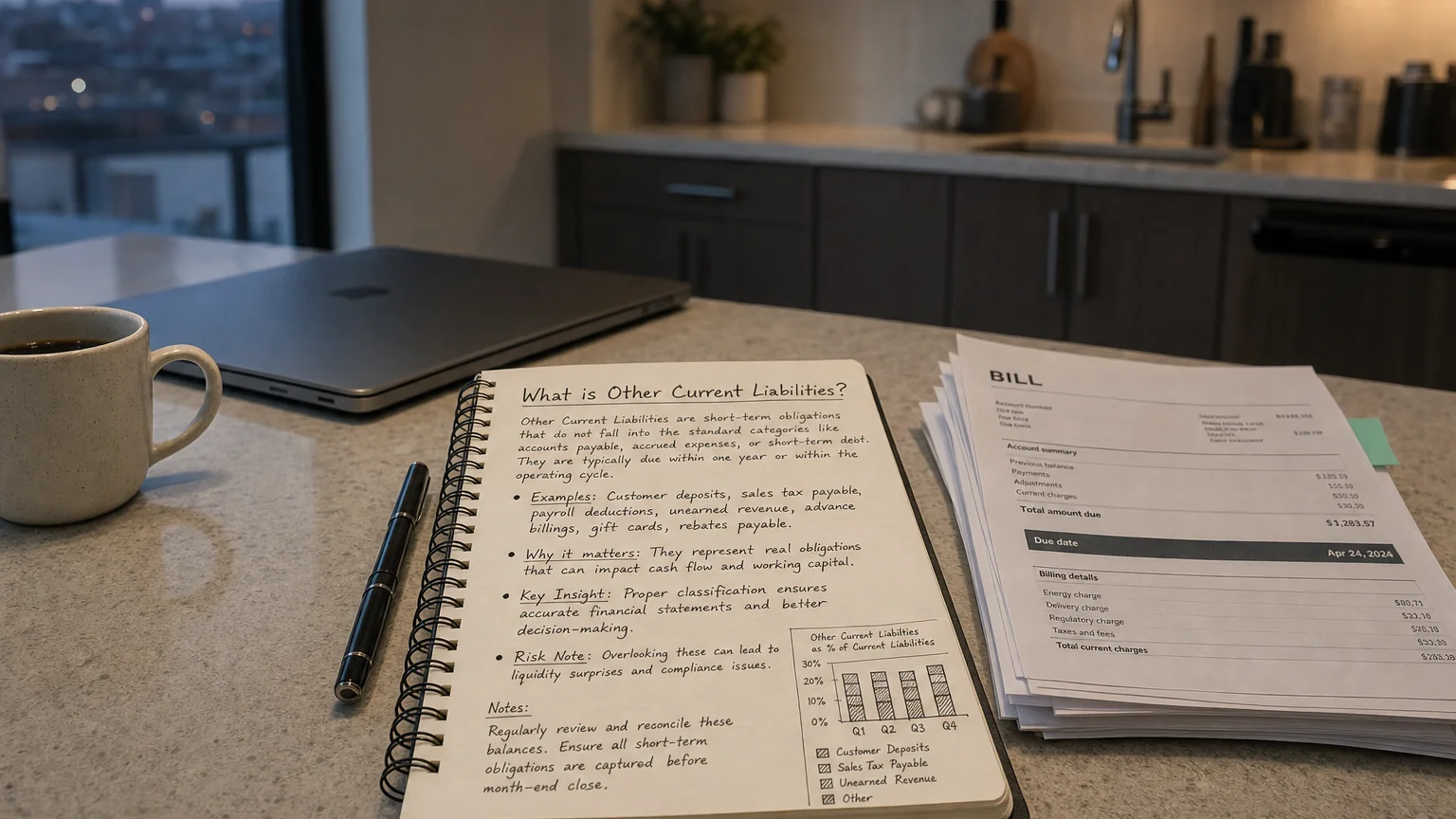

Other Current Liabilities represent short-term obligations (debts or payable amounts due within the next 12 months) that are grouped together rather than listed individually. In essence, these are current liabilities that are not significant enough to merit their own separate line on the balance sheet. Instead of cluttering the balance sheet with many small or infrequent items, a company will lump them into an “other” category. In other words, it’s a catch-all grouping for various smaller current obligations that don’t fit neatly into the major current liability categories like accounts payable, short-term debt, or accrued expenses.

Typical Components Included in Other Current Liabilities

Many types of obligations can fall under Other Current Liabilities, depending on the company and industry. Common components include:

-

Accrued Expenses (Accrued Liabilities): Expenses that have been incurred but not yet paid. This can include accrued wages or salaries owed to employees, interest payable on loans, utilities or rent that have built up, etc. Companies often group such accrued expenses (salaries, interest, utilities, etc.) into other current liabilities if they are not shown as separate line items. Essentially, these are short-term payables that the company owes due to past services or costs, even though the cash hasn’t been paid out yet.

-

Unearned or Deferred Revenue (Customer Prepayments): Money received in advance of providing goods or services. For example, customer deposits or advance payments, and outstanding gift card balances are unearned revenue. The company owes the customer the product/service or a refund, so until it’s delivered, this is a liability. Such deferred revenue or customer deposits are often listed under other current liabilities. (This is common in industries like subscriptions, gift cards, or project deposits.)

-

Dividends Payable: If the company’s board has declared dividends to shareholders that have not yet been paid, that declared amount is a current liability. When the amount is not large enough to warrant its own line, it can be included in other current liabilities. These dividends are generally due within a short period (often within a quarter), making them current obligations.

-

Short-Term Loans or Notes Payable (if not separately listed): Any small short-term borrowings that the company must repay within the year can fall here. For instance, a company that seldom uses short-term bank loans might not list a “short-term debt” line separately; instead, a minor loan or line-of-credit balance could be grouped into other current liabilities. (If short-term debt is substantial or regularly used, it would typically be shown as its own line item rather than in “other”.)

-

Current Portion of Long-Term Obligations: The portions of long-term liabilities that are due within the next year can be included. This might encompass the current portion of deferred tax liabilities, the current portion of long-term debt or lease obligations, or any upcoming payments on long-term loans, bonds, or mortgages due within 12 months. Often, large current portions (like the current portion of long-term debt) are shown separately, but smaller or less usual items might be tucked into other current liabilities.

-

Provisions for Warranties or Legal/Contingent Liabilities: These are short-term estimated obligations. For example, a company may have an accrued liability for product warranty claims expected to be settled within a year, or it might have a pending lawsuit or legal settlement that will require payment in the near term. Such contingent liabilities or warranty provisions due within a year can be part of other current liabilities. They require some estimation and are recorded because they represent probable short-term sacrifices of economic benefits (e.g. paying customers’ warranty claims or legal damages).

-

Taxes Payable (if not listed separately): Any current tax obligations, such as income taxes due, sales taxes collected to be remitted, or property taxes owed, could be included in this category if the company doesn’t list a separate “Taxes Payable” line. For instance, income taxes that have accrued but are not yet paid at the balance sheet date are current liabilities; companies sometimes group such tax payables under other current liabilities when they are not material enough to be isolated on the face of the balance sheet.

(Note: The specific items included in “Other Current Liabilities” will vary by company. Many firms disclose the composition of this line in the footnotes to the financial statements if it’s significant, so that analysts can see the major components.)

Why Group Items Under “Other Current Liabilities”?

Materiality and Clarity: Companies group certain items under Other Current Liabilities to keep the balance sheet concise and focused on the most important figures. If every small liability had its own line, financial statements would become unwieldy and harder to read. By aggregating minor or less common liabilities into one line, the balance sheet remains streamlined. In general, any item that is large or significant enough (or of particular interest to stakeholders) will get its own line, whereas miscellaneous small obligations get lumped into “other.” This practice follows the accounting concept of materiality – only significant information merits separate presentation.

Simplicity: For example, suppose a company has a variety of tiny obligations – a small payroll payable here, a minor interest payable there, a few customer deposits – none of which individually amount to much. Listing each one separately isn’t useful to the reader. Instead, they aggregate these into Other Current Liabilities as a single total. This catch-all category captures liabilities due within the year that do not fit neatly into another specific line item on the balance sheet.

Frequency/Importance: Often, items that are not part of the company’s core operations or not incurred regularly are grouped as “other.” Accounts that require greater transparency or are frequent (like Accounts Payable) are shown individually, whereas accounts that are ancillary or infrequent may be combined into “other current liabilities”. For instance, if a company hardly ever has short-term bank loans, it might not dedicate a line to short-term debt; any occasional small loan would just appear in the other current liabilities category.

In summary, grouping under Other Current Liabilities helps avoid overloading the balance sheet with detail, focusing attention on key obligations while still reporting all debts due within a year (with details available in notes if needed). Companies and regulators do monitor this grouping – if any one component of “other” is big enough (relative to total current liabilities), it typically must be disclosed separately (either on the balance sheet or in a note), so nothing truly important is hidden.

Other Current Liabilities vs. Long-Term Liabilities

The distinction between current and long-term liabilities is primarily the time horizon for payment. Other Current Liabilities consist of obligations due within the next 12 months (or operating cycle). In contrast, long-term liabilities are debts or obligations that are due in more than one year. So, an “Other Long-Term Liabilities” category might exist separately for miscellaneous liabilities that will be paid over a longer period (such as long-term asset retirement obligations, deferred tax liabilities due in future years, etc.).

Key differences include:

-

Timing: Items classified under other current liabilities must be settled in the short term (next year), whereas long-term liabilities (including any “other long-term liabilities”) are not due for settlement soon. This means other current liabilities have a more immediate impact on the company’s cash flow in the near term, while long-term liabilities represent future obligations.

-

Balance Sheet Presentation: Current liabilities (including other current liabs) are listed in a separate section from long-term liabilities. Other current liabilities contribute to total current liabilities, which is used to assess short-term liquidity. Long-term liabilities are listed below current liabilities and contribute to the total liabilities and long-term solvency considerations.

-

Analytical Impact: Because other current liabilities must be paid within a year, they factor into liquidity metrics (like the current ratio, discussed below). Long-term liabilities, on the other hand, are examined in context of solvency and leverage (for example, debt-to-equity ratios) since they affect the company’s long-term financial stability. A $10 million obligation due next month is a much more urgent strain on liquidity than a $10 million bond due in five years – thus, the former would be in current liabilities (affecting short-term liquidity analysis) while the latter is a long-term liability (affecting long-term debt analysis).

In summary, Other Current Liabilities differ from long-term liabilities simply by when the company owes the money: if it’s within the coming year, it’s current; if it’s farther out, it’s long-term. The “other” designation in both cases just means the items are miscellaneous or minor ones aggregated for convenience.

Other Current Liabilities vs. Specific Current Liabilities (Accounts Payable, etc.)

It’s also useful to distinguish Other Current Liabilities from the well-known specific current liabilities like Accounts Payable or Short-Term Debt. Accounts payable (money owed to suppliers on credit) and short-term debt (like bank loans due within a year) are typically separate line items on the balance sheet because they are common and often significant in amount. They each have a clear definition and importance: e.g., accounts payable is usually one of the largest current liabilities for many firms and is closely watched as part of working capital.

By contrast, “Other Current Liabilities” is a general category. It covers all the remaining short-term obligations that don’t have their own titled line. If an obligation is large or important enough (say a big bank loan, or a sizable accrued expense), it will be listed on its own. But if a liability doesn’t fit into the standard categories or is relatively small, it gets grouped into other current liabilities. In other words, other current liabilities exist to capture “everything else” short-term that isn’t accounts payable, isn’t a major short-term loan, isn’t taxes payable, etc.

For example, imagine a company only occasionally has a small note payable. If the amount is minor, instead of showing a separate “Notes Payable” line, the company might include that amount under other current liabilities. As one source notes: if a company rarely uses short-term loans, it may group those loans into an “other” category rather than listing them separately. The same goes for other sporadic or minor items like a one-time payable or a small outstanding expense – they simply get absorbed into the Other Current Liabilities line.

Accounts Payable vs. Other Current Liabilities: Accounts payable (A/P) specifically refers to trade payables – amounts owed to suppliers for goods and services received. A/P is generally listed separately because it’s a major, recurring liability for most businesses. Other current liabilities would not include normal accounts payable. However, other current liabilities might include other payables that aren’t trade-related. For instance, if a company has a payable to a non-trade creditor or an unusual short-term obligation, those could fall in “other.”

Short-Term Debt vs. Other Current Liabilities: If a company has a formal short-term debt (like a bank loan due in 6 months or a revolving credit facility usage), that is often listed as Short-Term Borrowings or Short-Term Debt. But if the company has no significant borrowings, or perhaps only a small note, it might not break it out. In such cases, that small debt could hide within other current liabilities. Essentially, other current liabilities excludes the major defined categories (A/P, short-term debt, current portion of long-term debt, accrued payroll, etc.) unless those categories are themselves absent or immaterial.

Think of Other Current Liabilities as the “miscellaneous” drawer of current debts: necessary to capture everything current that isn’t explicitly labeled elsewhere. It ensures the balance sheet’s current liabilities section is complete without itemizing every trivial payable.

Impact on Liquidity and Solvency Analysis

Even though “Other Current Liabilities” might appear as a single line, it plays an important role in financial analysis, especially regarding liquidity (short-term financial health) and to some extent solvency (long-term sustainability):

-

Liquidity Analysis: Other current liabilities are part of a company’s total current liabilities, so they directly factor into key liquidity ratios. For instance, the current ratio (current assets divided by current liabilities) and quick ratio consider all current liabilities – including those grouped under “other”. If other current liabilities suddenly increase (without a corresponding rise in current assets or cash), these liquidity ratios will worsen, signaling potential short-term financial strain. Analysts pay attention to changes in other current liabilities for this reason. A significant jump in this line item might indicate that the company has incurred new short-term obligations that could pressure cash flow – for example, accruing a large expense or a short-term portion of a legal settlement. On the flip side, a decrease in other current liabilities can improve liquidity ratios (assuming assets remain constant), indicating the company has paid off or reduced some obligations. In summary, a higher level of current liabilities (including “other”) means the company needs more liquid assets to comfortably meet those upcoming payments, so liquidity is tighter.

-

Solvency and Financial Flexibility: Solvency typically concerns long-term obligations, but a high level of other current liabilities can also raise flags about a company’s overall financial health. If a company has many short-term obligations piled into “other current liabilities,” it may suggest the company faces several imminent demands on its cash. Creditors and investors will consider this when assessing the company’s solvency and working capital management. For example, if other current liabilities comprise unusual items like a sizable payable due to a legal judgment or a large amount of deferred revenue that will require future service delivery, analysts might consider whether the company has the resources to handle these near-term obligations without jeopardizing longer-term stability. Moreover, other current liabilities can affect working capital (current assets minus current liabilities) – a key indicator of short-term financial flexibility. A company with current liabilities (including other) far exceeding its current assets could be at risk of liquidity crunch and, if not managed, potentially insolvency. Thus, while solvency ratios (like debt-to-equity) focus more on long-term debt, the composition and size of current liabilities are also pertinent to understanding if a company can remain solvent through the coming year.

-

Hidden Obligations & Footnote Analysis: Another analytical consideration is that important obligations might be “hidden” in the other current liabilities line until you dig into the details. Seasoned analysts will often review the footnotes to see the breakdown of other current liabilities. This can reveal things like a large accrued expense or a short-term provision that the company must address. For instance, if a company has a significant accrual for litigation or a major deferred revenue obligation to fulfill, those details would be in the notes. Recognizing these components is crucial for fully evaluating liquidity. In short, other current liabilities should not be ignored just because it’s a single line – one must ask “What’s in there?” to properly gauge short-term financial obligations.

Example: Appearance of Other Current Liabilities on a Balance Sheet

To illustrate, consider a simplified partial balance sheet for a hypothetical company RetailCorp Inc. (figures in millions of dollars):

| Current Liabilities | Amount |

|---|---|

| Accounts Payable | $45.0 |

| Short-Term Debt | $25.0 |

| Accrued Expenses | $18.0 |

| Other Current Liabilities | $12.0 |

| Total Current Liabilities | $100.0 |

In this example, RetailCorp has aggregated $12.0 million of various smaller liabilities under Other Current Liabilities, out of $100.0 million total current liabilities. This “other” category sits below the more specifically identified items (accounts payable, short-term debt, accrued expenses) and contributes to the total current liabilities.

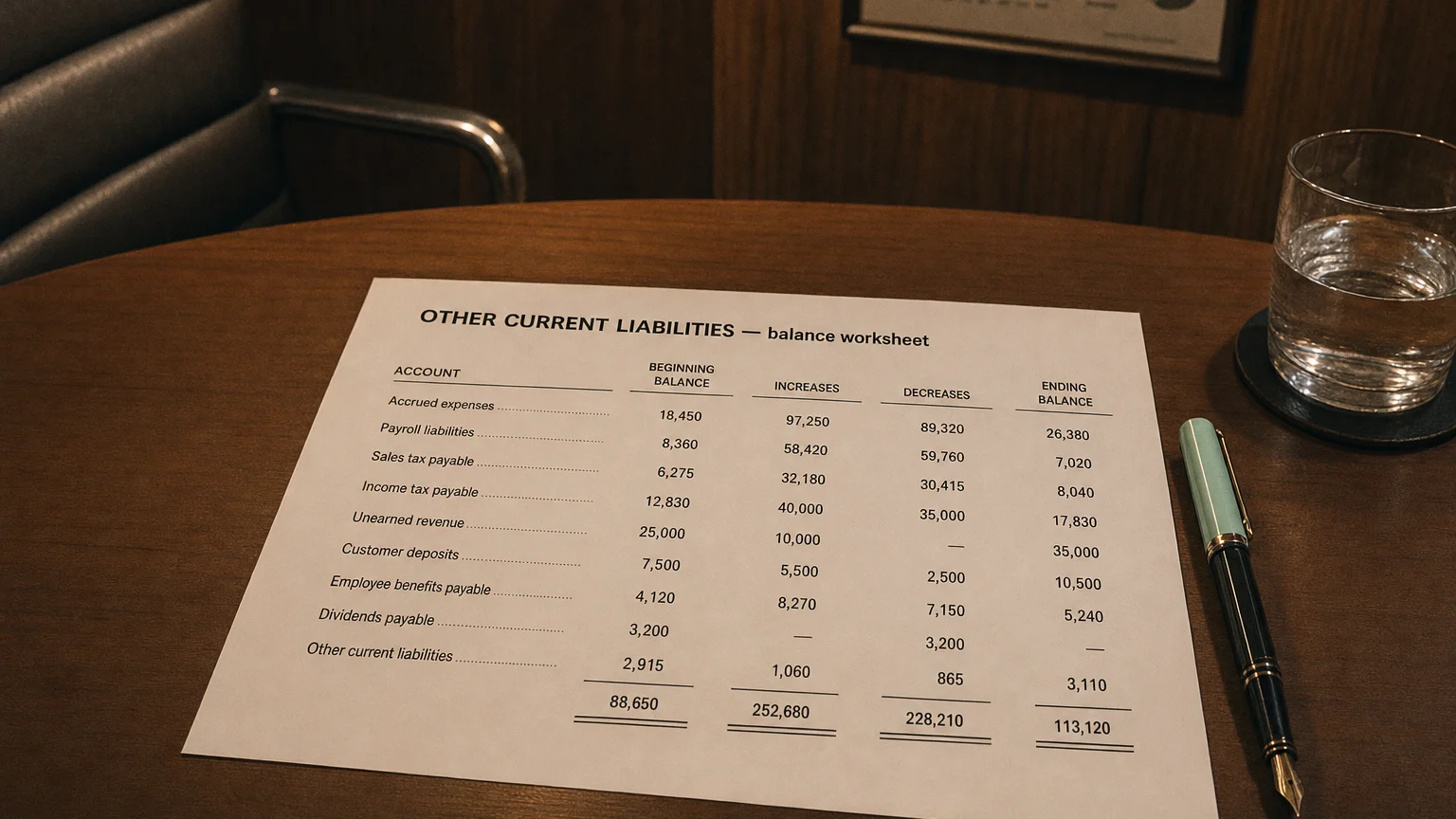

Importantly, the company’s financial statement footnotes would typically explain what makes up that $12.0 million. Suppose the footnote reveals that the Other Current Liabilities consist of: $4.5 million in outstanding gift card balances (unearned revenue), $3.2 million in customer loyalty program points that will be redeemed (another form of deferred revenue or obligation to customers), $2.8 million of accrued warranty liabilities for products, and $1.5 million of customer deposit liabilities. Listing each of those on the balance sheet would be cumbersome, so instead they are summed up as “Other Current Liabilities.” An analyst now knows that a good chunk of those liabilities are obligations to customers (gift cards, loyalty points, deposits) and an accrual for warranties – all of which will likely result in either cash outflow or service delivery in the coming year.

Interpretation: Seeing “Other Current Liabilities” on a balance sheet, you should recognize it as a mixture of various smaller short-term obligations. The example above shows how it might appear and be broken down. When analyzing a real company, one would check the notes to determine if any large or unusual items are included in that category. If, say, the other current liabilities number is growing rapidly over time, it warrants investigation – it could signal things like rising accrued expenses or new types of obligations (perhaps an increase in deferred revenue as the company sells more gift cards or subscriptions, or an accrued legal expense, etc.).

In conclusion, Other Current Liabilities is an important line that ensures all short-term liabilities are accounted for, even if they don’t each get named on the balance sheet. It provides completeness to the current liabilities section and is a useful category for grouping miscellaneous items. Understanding this category helps in painting a full picture of a company’s short-term financial obligations and is essential for thorough financial statement analysis.

Q · 01What is Other Current Liabilities?+