is a financial concept covered in this article. Short-Term Expenses Incurred But Not Yet Paid or Invoiced

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

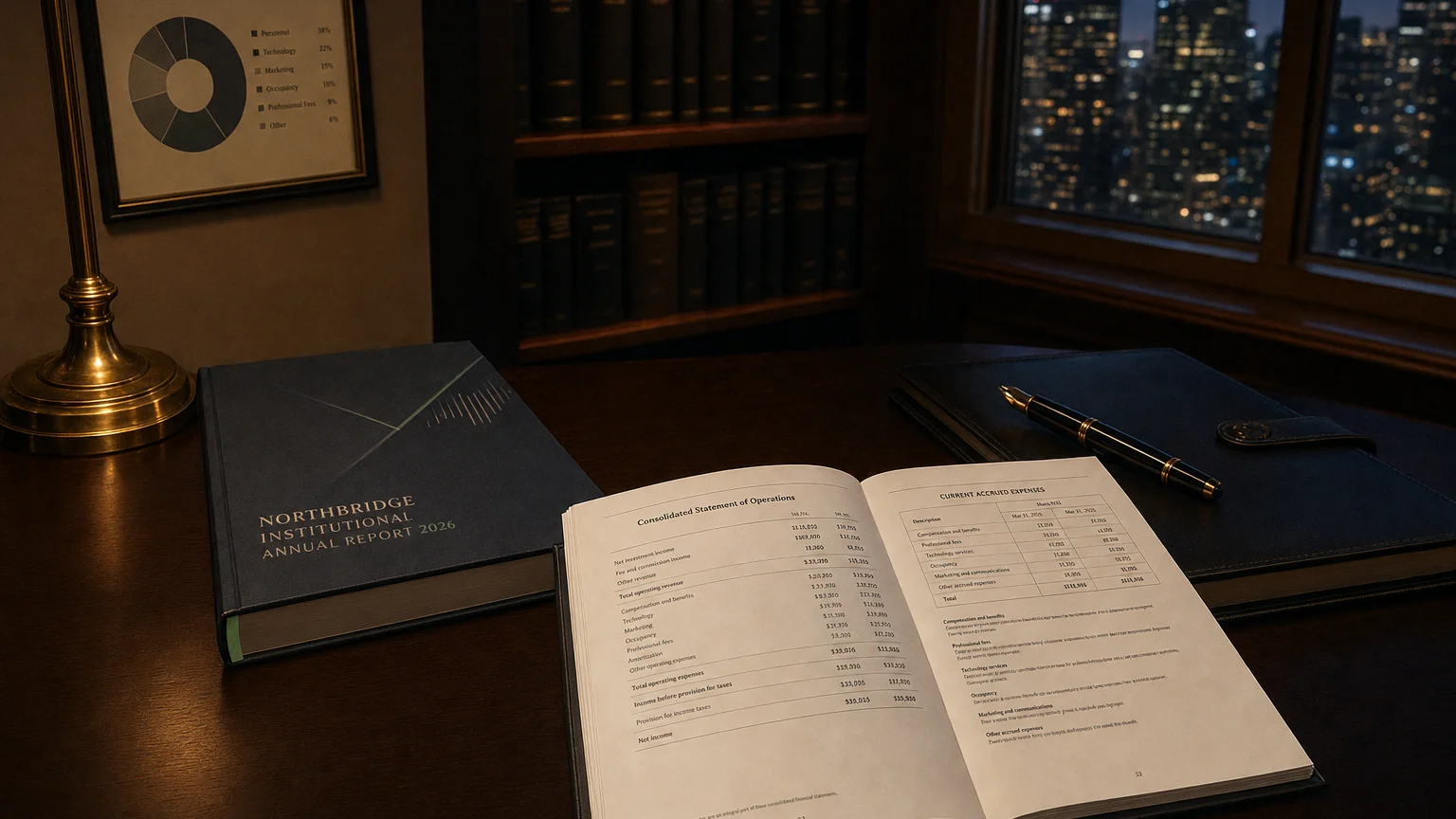

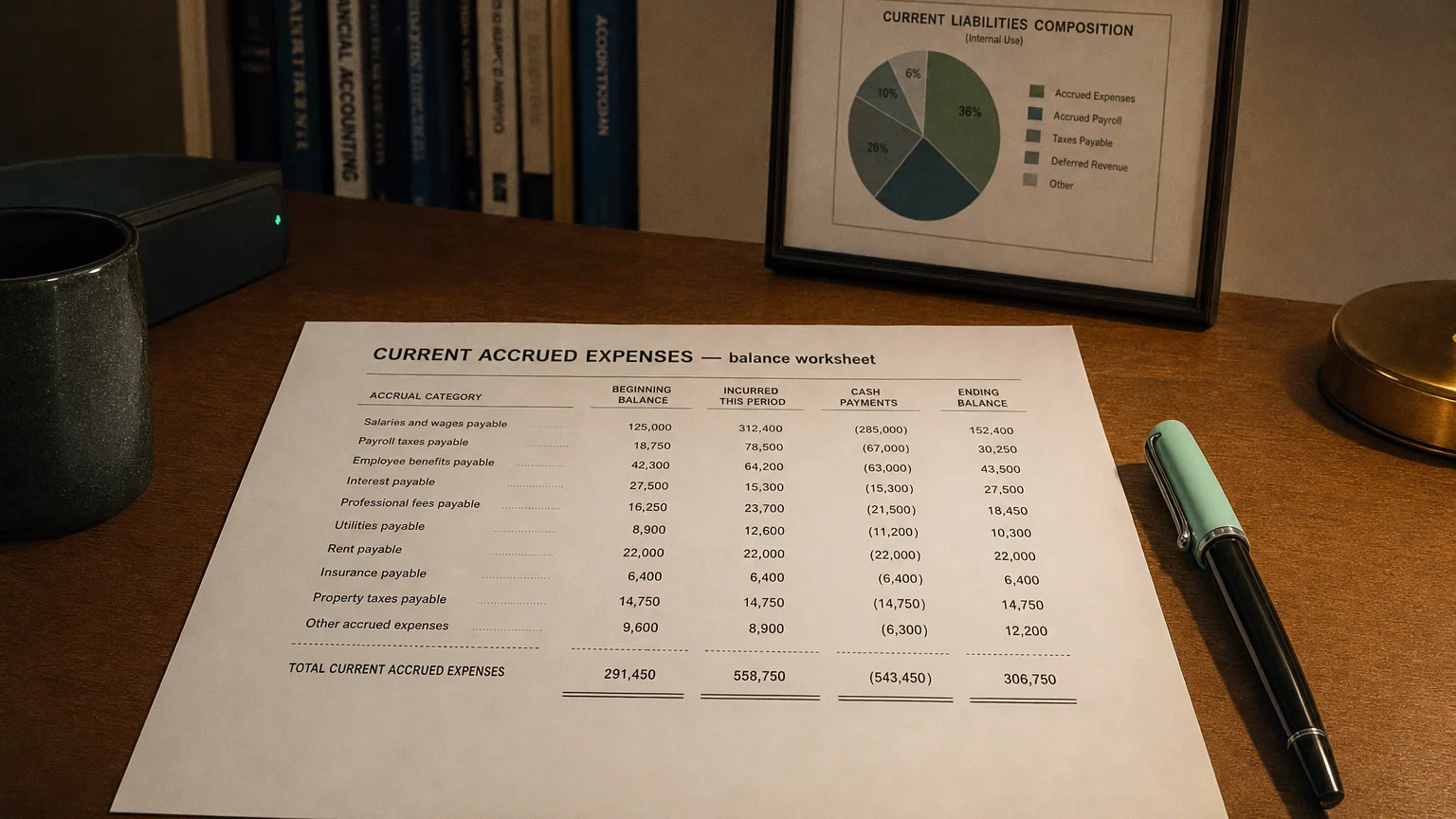

Current Accrued Expenses (or Accrued Liabilities - Current) represent expenses that a company has incurred during the reporting period but has not yet paid or received an invoice for, with payment expected within 12 months or the operating cycle. These are recognized under accrual accounting to match expenses with the period in which they are incurred, regardless of cash payment timing.

Definition and Purpose

Current Accrued Expenses ensure expenses are recorded in the period they help generate revenue, even if cash payment occurs later.

They differ from accounts payable (invoice received) by often lacking formal invoices and requiring estimation or time-based allocation.

The ‘current’ portion covers obligations due within one year.

Common Examples

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

- Accrued salaries and wages (earned but unpaid at period-end)

- Accrued employee bonuses and commissions

- Accrued utilities (electricity, water used but unbilled)

- Accrued interest on borrowings

- Accrued professional fees (legal, audit)

- Accrued advertising or marketing expenses

- Accrued rent or property taxes

High-service or labor-intensive businesses typically show larger balances.

Accounting Treatment

Recognition process:

- Estimate or calculate expense incurred

- Debit Expense (income statement)

- Credit Accrued Expenses (balance sheet)

- Reverse/pay when invoice received or cash paid

Reversals prevent double-counting when actual invoice/payment occurs.

Balance Sheet Presentation

Appears under current liabilities as:

- ‘Current Accrued Expenses’

- ‘Accrued Liabilities’

- ‘Accrued Expenses and Other Liabilities’

- Often grouped in ‘Payables and Accrued Expenses’

Major components disclosed in footnotes.

Distinction from Similar Items

Current Accrued Expenses

- Incurred but unbilled/unpaid

- Estimation common

Accounts Payable

- Invoice received

- Trade/supplier specific

Provisions

- Higher uncertainty (e.g., warranties, litigation)

Analytical Implications

These balances indicate:

- Operational activity level (higher expenses = higher accruals)

- Working capital needs (near-term cash outflows)

- Earnings quality (estimation judgments)

- Seasonality (e.g., bonus accruals at year-end)

- Comparison to cash payments in cash flow statement

Rapid growth may signal increasing operational scale or delayed payments.

Q · 01What is Current Accrued Expenses?+