is a financial concept covered in this article. Long-Term Portion of Expenses Incurred But Not Yet Paid

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

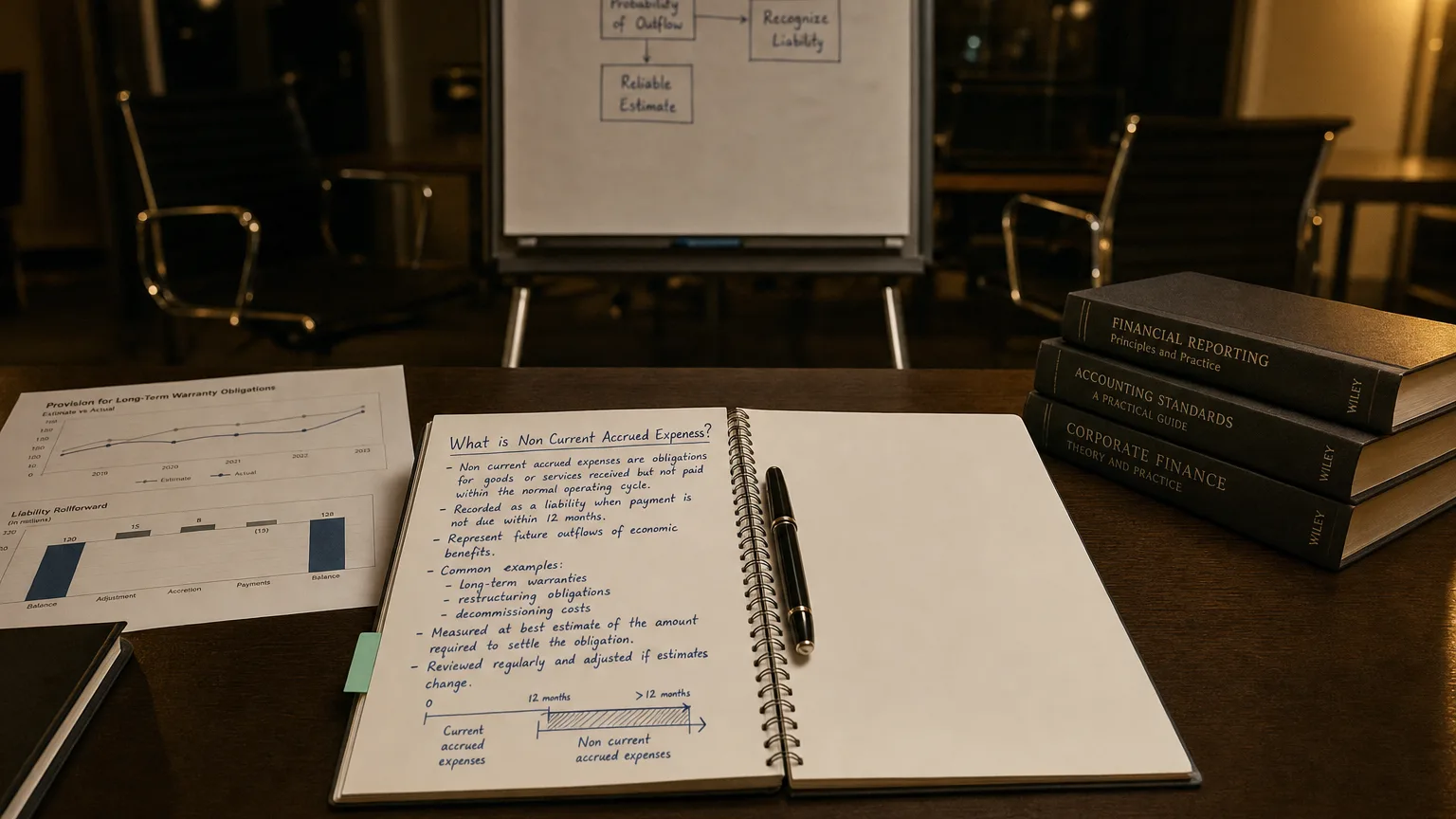

Non Current Accrued Expenses represent obligations for goods or services that have been received or consumed by the company, where the expense has been recognized in the income statement, but payment is not due within the next 12 months. These are the long-term portion of accrued liabilities, reflecting timing differences between expense recognition and cash settlement.

Definition and Purpose

Non Current Accrued Expenses arise under accrual accounting when an expense is recognized in the period it is incurred, regardless of when cash payment occurs.

The non-current portion covers obligations expected to be settled after more than one year or one operating cycle.

Distinguishes from accounts payable (invoice received) — accruals often lack formal invoices and involve estimation.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

Common Examples

- Long-term incentive compensation or bonuses payable over multiple years

- Accrued restructuring costs with extended payment terms

- Long-term warranty obligations beyond one year

- Accrued legal settlements or litigation expected to settle far in future

- Environmental cleanup costs with long timelines

- Accrued interest on long-term debt (if payable periodically)

- Deferred compensation plans

Overlaps with provisions when uncertainty exists (e.g., warranties, litigation).

Accounting Treatment

Recognition:

- Expense debited when incurred (matching principle)

- Credit to accrued liability

- Reclassify to current as due within 12 months

- Estimate if amount uncertain (best estimate required)

Discounting may apply if time value material and settlement significantly delayed.

Subject to periodic reassessment — changes adjust expense.

Balance Sheet Presentation

Appears under non-current liabilities as:

- ‘Non Current Accrued Expenses’

- ‘Long-Term Accrued Liabilities’

- ‘Other Non Current Accrued Expenses’

- Often aggregated with detailed breakdown in notes

Footnotes describe nature, expected timing, and major components.

Distinction from Provisions

While overlapping:

- Accrued expenses: More certain timing/amount (e.g., known bonus formula)

- Provisions: Higher uncertainty (e.g., estimated warranty claims)

- Many companies use interchangeably for long-term accruals

Analytical Considerations

These liabilities indicate:

- Long-term commitments beyond normal operating cycle

- Potential cash outflow timing (liquidity planning)

- Earnings quality (subjective estimates possible)

- Operational risks (e.g., high litigation accruals)

- Comparison to current accruals for working capital trends

Growth may signal increasing long-term obligations; reversals can inflate future earnings.