A detailed guide to short-term obligations on the balance sheet where a company has received a benefit but must provide a good, service, or payment within the n

You can't take the same actions as everyone else and expect to outperform.

Current deferred liabilities are short-term obligations that a company has incurred but not yet fulfilled or paid, where the settlement is deferred to a future date (within the next 12 months). In accrual accounting, these liabilities arise when a company receives a benefit (like cash) but the corresponding performance will occur later. Because these obligations are due within one year, they are classified as current liabilities on the balance sheet. A primary example is deferred revenue, where a company owes goods or services to customers who have paid in advance.

Common Examples of Current Deferred Liabilities

Current deferred liabilities can take several forms, with the most common being:

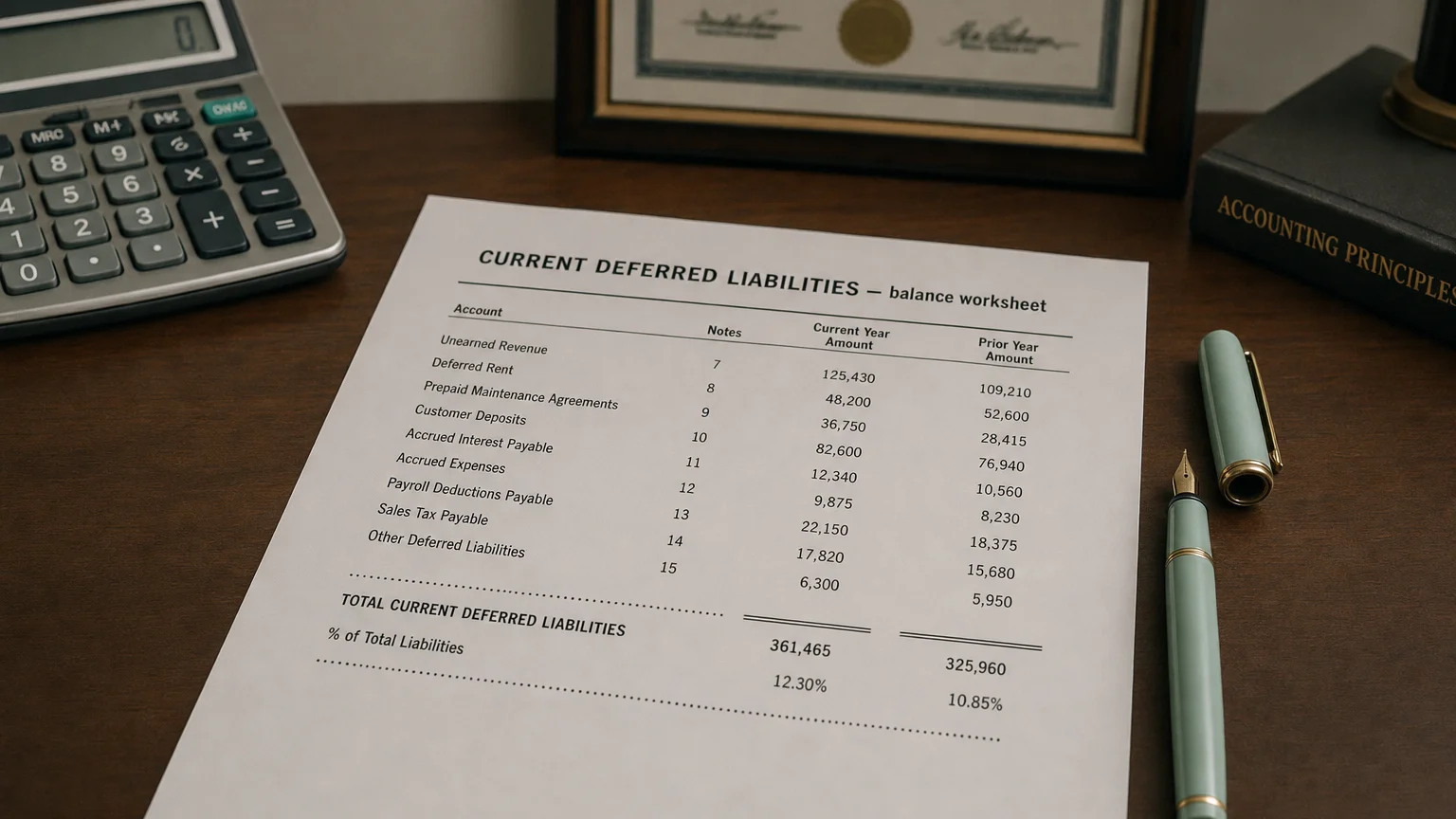

- Deferred Revenue (Unearned Revenue): This is the classic example. It arises when a company receives payment in advance of delivering goods or services. Examples include prepaid annual software subscriptions, gift card balances, and tickets sold for an upcoming event.

- Short-Term Deferred Tax Liabilities: These arise from temporary timing differences between financial and tax accounting that are expected to reverse within the next year, resulting in a higher tax payment in the near future.

- Customer Advances and Deposits: Similar to deferred revenue, this is cash received from customers for orders or projects to be completed in the near term. The company owes either the product, the service, or a refund.

Current vs. Non-Current Deferred Liabilities

“You can’t take the same actions as everyone else and expect to outperform.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘Dare to Be Great’ (2006)

The key difference is the timing of when the obligation will be settled. Current deferred liabilities are due within one year, whereas non-current deferred liabilities are not expected to be settled for more than a year. Companies often split deferred liabilities into current and non-current portions on the balance sheet.

Subscription Example

If a customer pays upfront for a 5-year software license, only the portion of the service to be delivered in the first year is recorded as a current deferred revenue liability. The remaining balance for years 2-5 is classified as a non-current deferred revenue liability.

Impact on Financial Analysis and Key Metrics

Current deferred liabilities can significantly affect a company’s liquidity metrics and working capital analysis:

- Working Capital: Because they are a current liability, they reduce working capital (). A large deferred revenue balance can even result in negative working capital on paper.

- Liquidity Ratios: An increase in current deferred liabilities raises total current liabilities, which lowers the Current Ratio. This can make a company appear less liquid, even if it has a strong cash position from the customer prepayments.

- Revenue Visibility: On the positive side, a growing deferred revenue balance often indicates strong future revenue, as it represents sales that have been booked but not yet recognized.

Analytical Consideration

Analysts must interpret liquidity ratios in context. A software company with a low Current Ratio due to high deferred revenue is not necessarily in distress, as the liability will be settled by providing a service, not paying cash. The upfront cash collection is a sign of a healthy business model.

Real-World Examples

Current deferred liabilities are common across many industries:

- Tech & Software (SaaS): Companies like Salesforce report substantial current deferred revenue from prepaid annual subscriptions, giving investors insight into the future revenue pipeline.

- Retail & Gift Cards: Retailers like Starbucks record the value of unredeemed gift cards as a current deferred liability (often called ‘stored value card liability’).

- Franchises: Companies like Papa John’s report current deferred revenue from upfront franchisee fees for services that will be provided within the upcoming year.

- Manufacturing: Factories often take customer deposits for custom orders, recording them as a current deferred liability until the product is delivered.

Q · 01What is Current Deferred Liabilities?+