Long-Term Obligations Arising from Timing Differences in Revenue or Gain Recognition

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

Non Current Deferred Liabilities represent amounts received or accrued by a company that will be recognized as revenue, income, or gains in future periods beyond the next 12 months. These are non-current portions of deferred (unearned) revenue or similar items where the company has an obligation to deliver goods/services or where accounting rules defer recognition over an extended period.

Definition and Nature

Non Current Deferred Liabilities arise when a company receives cash or consideration upfront but accounting standards require recognition of the associated revenue or gain over a longer period (beyond one year).

They represent future performance obligations or timing differences, distinguishing them from immediate liabilities or accrued expenses.

The non-current portion is separated from current to match the expected timing of revenue recognition.

Common Examples

- Long-term deferred/unearned revenue (multi-year subscriptions, licenses, maintenance contracts)

- Advance payments for goods/services delivered over several years

- Deferred gains on sale-leaseback transactions (recognized over lease term)

- Government grants or incentives deferred over asset life or performance period

- Customer loyalty programs with long redemption horizons

- Upfront fees in long-term contracts (e.g., insurance premiums, telecom)

Example: Software company receives 3-year subscription payment upfront → portion beyond 12 months classified as non-current deferred liability.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

Accounting Treatment

Under ASC 606 / IFRS 15 (revenue from contracts):

- Recognize liability when cash received before satisfying performance obligation

- Allocate transaction price to obligations

- Classify as current/non-current based on expected recognition timing

- Recognize revenue as control transfers (over time or point in time)

Other deferrals follow specific guidance (e.g., leases, grants).

No interest imputation unless significant financing component.

Balance Sheet Presentation

Shown under non-current liabilities as:

- ‘Non Current Deferred Liabilities’

- ‘Long-Term Deferred Revenue’

- ‘Other Non Current Deferred Liabilities’

- Often aggregated with separate disclosure in notes

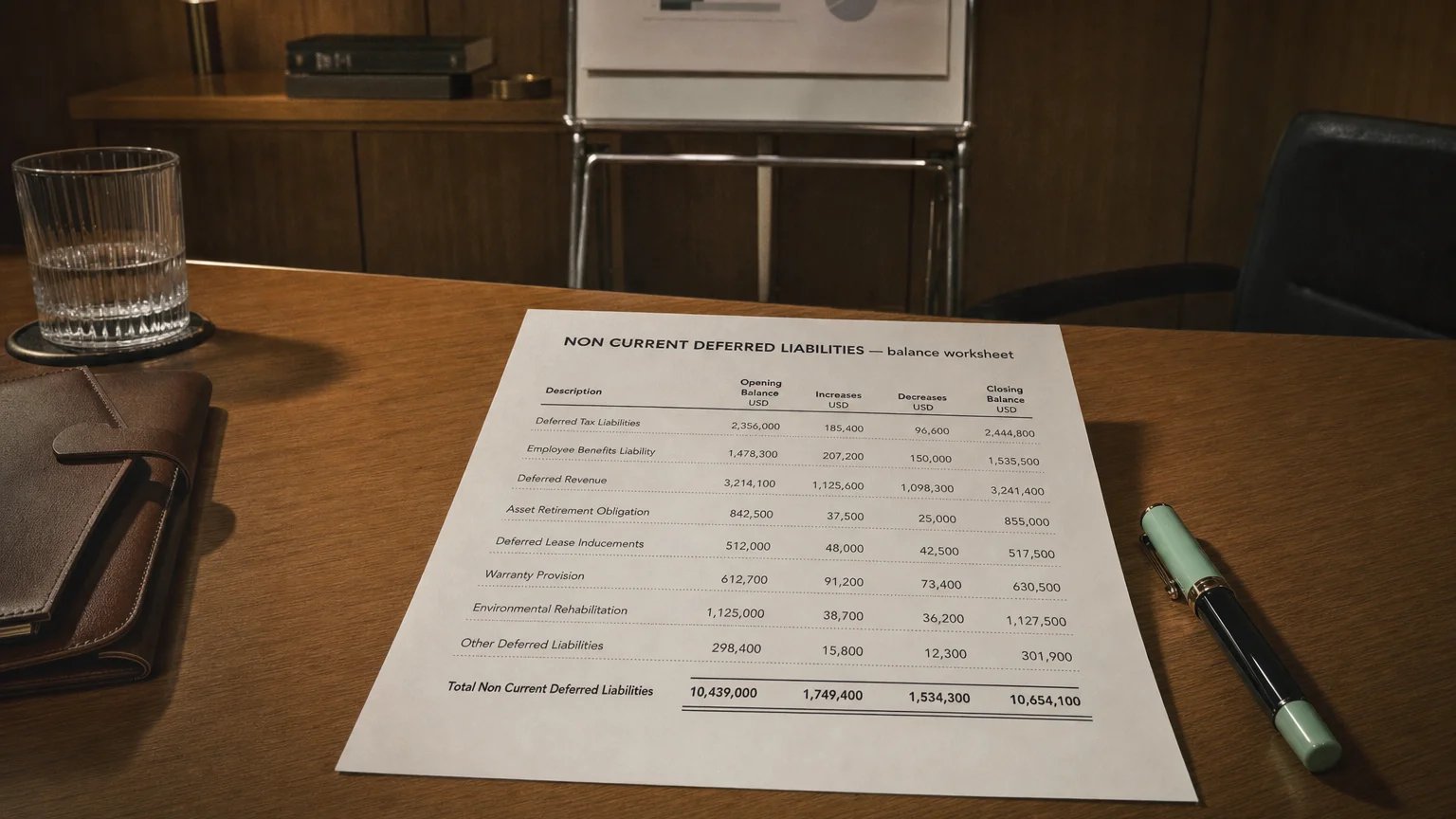

Movements detailed in footnotes (opening, additions, revenue recognized, adjustments).

Analytical Implications

These liabilities provide insight into:

- Future revenue visibility (high-quality recurring revenue)

- Business model (subscription vs. transactional)

- Cash flow ahead of earnings (positive working capital)

- Contract backlog and customer commitment

- Potential earnings volatility as deferred amounts recognize

Large growth in deferred liabilities signals strong sales; sharp declines may indicate slowing bookings.

Q · 01What is Non Current Deferred Liabilities?+