Additional Liability Recognized for Underfunded Defined Benefit Pension Plans (Historical US GAAP Concept)

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

Minimum Pension Liabilities refers to an additional balance sheet liability that companies with defined benefit pension plans were required to recognize under older US GAAP rules (pre-2006) when the plan was significantly underfunded. It represented the excess of the accumulated benefit obligation (ABO) over the fair value of plan assets, adjusted for any existing accrued/prepaid pension cost. This item is largely historical today, replaced by more comprehensive net pension liability recognition.

Historical Context and Definition

Under original SFAS 87 (Employers’ Accounting for Pensions), companies recognized periodic pension expense but did not fully reflect the funded status on the balance sheet. Instead, only a portion was recorded as accrued/prepaid pension cost.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (1934)

To address off-balance-sheet underfunding, an additional minimum liability was required if the plan’s Accumulated Benefit Obligation (ABO) exceeded the fair value of plan assets.

ABO is the present value of benefits earned to date, assuming no future salary increases (more conservative than PBO).

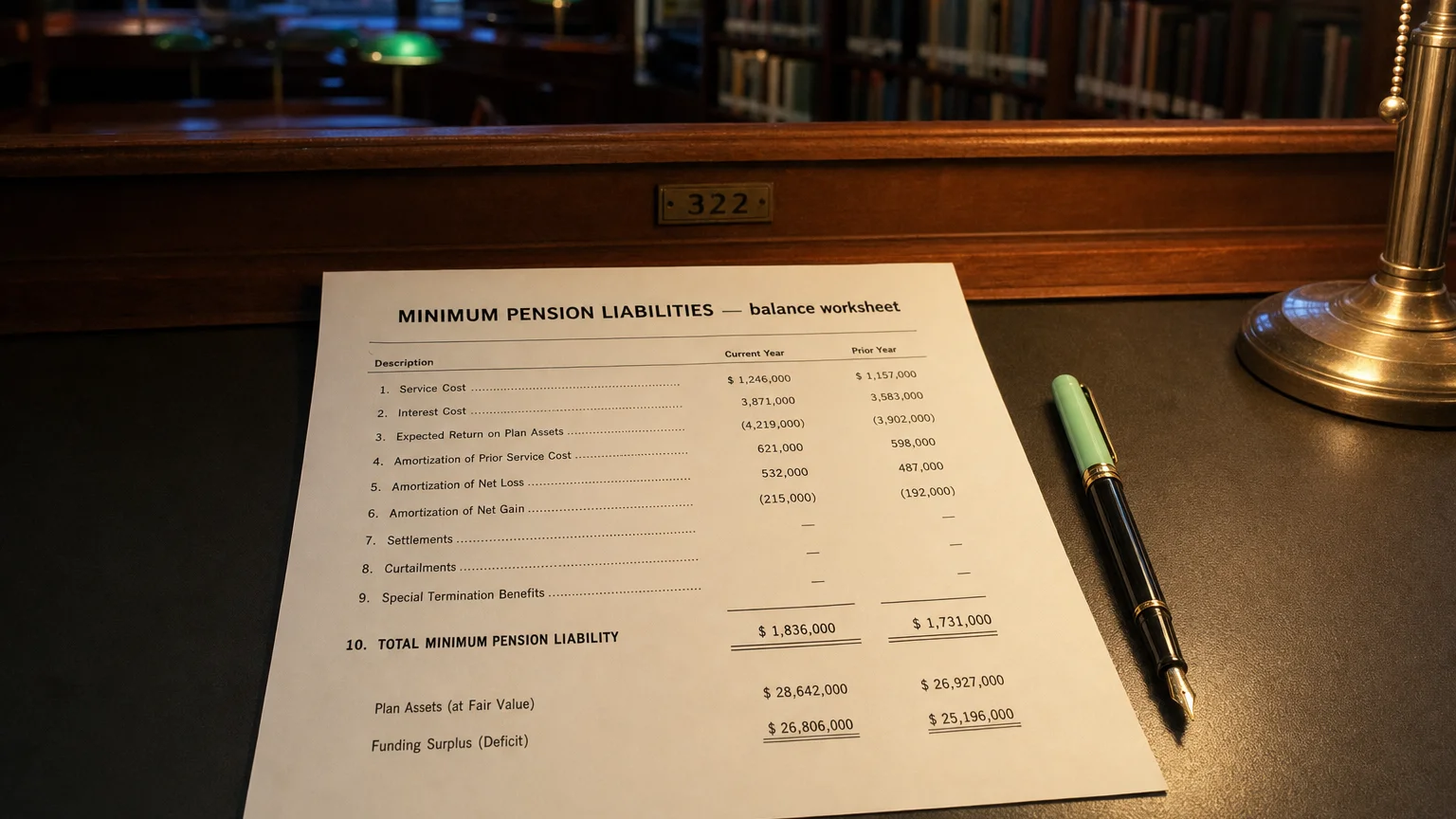

Calculation of Minimum Pension Liability

The additional minimum liability was computed as:

- Unfunded ABO = ABO − Fair value of plan assets

- Minimum liability = Unfunded ABO − (Existing accrued pension liability or + Existing prepaid pension asset)

- If result positive → Recognize additional liability

The offsetting entry was an intangible asset (up to unrecognized prior service cost) with the remainder to other comprehensive income (equity contra-item).

Balance Sheet Presentation (Historical)

When triggered:

- Additional liability shown under non-current liabilities (often as ‘Minimum Pension Liability’)

- Intangible asset (limited) in non-current assets

- Excess debited to OCI (accumulated other comprehensive loss)

This ensured minimum recognition of severe underfunding while deferring other actuarial gains/losses.

Evolution and Current Treatment

In 2006, SFAS 158 (now ASC 715) eliminated the minimum liability approach by requiring:

- Full recognition of funded status (PBO − Plan assets) as net pension liability/asset

- All actuarial gains/losses and prior service costs initially to OCI, with amortization options

Under current US GAAP and IFRS (IAS 19), the entire underfunded status is on the balance sheet as a non-current liability (or asset if overfunded).

Minimum pension liability line items are now rare—seen only in older filings or certain supplemental disclosures.

Why It Appears in Some Reports

You may still encounter ‘Minimum Pension Liabilities’ in:

- Historical financial data or comparative statements

- Certain international or legacy accounting frameworks

- Data providers aggregating pre-2006 information

- Supplemental pension disclosures

Analytical Relevance Today

Though obsolete, understanding it helps when:

- Analyzing pre-2006 financials or restatements

- Comparing old vs. new pension accounting impacts

- Evaluating off-balance-sheet obligations in historical context

- Interpreting OCI components related to pensions

Focus on current ‘Net Pension Liability’ under non-current liabilities for modern analysis.

Q · 01What is Minimum Pension Liabilities?+