is a financial concept covered in this article. Long-Term Obligations for Defined Benefit Pensions and OPEB

From the standpoint of an institution, the existence of a risk manager has less to do with actual risk reduction than it has to do with the impression of risk reduction.

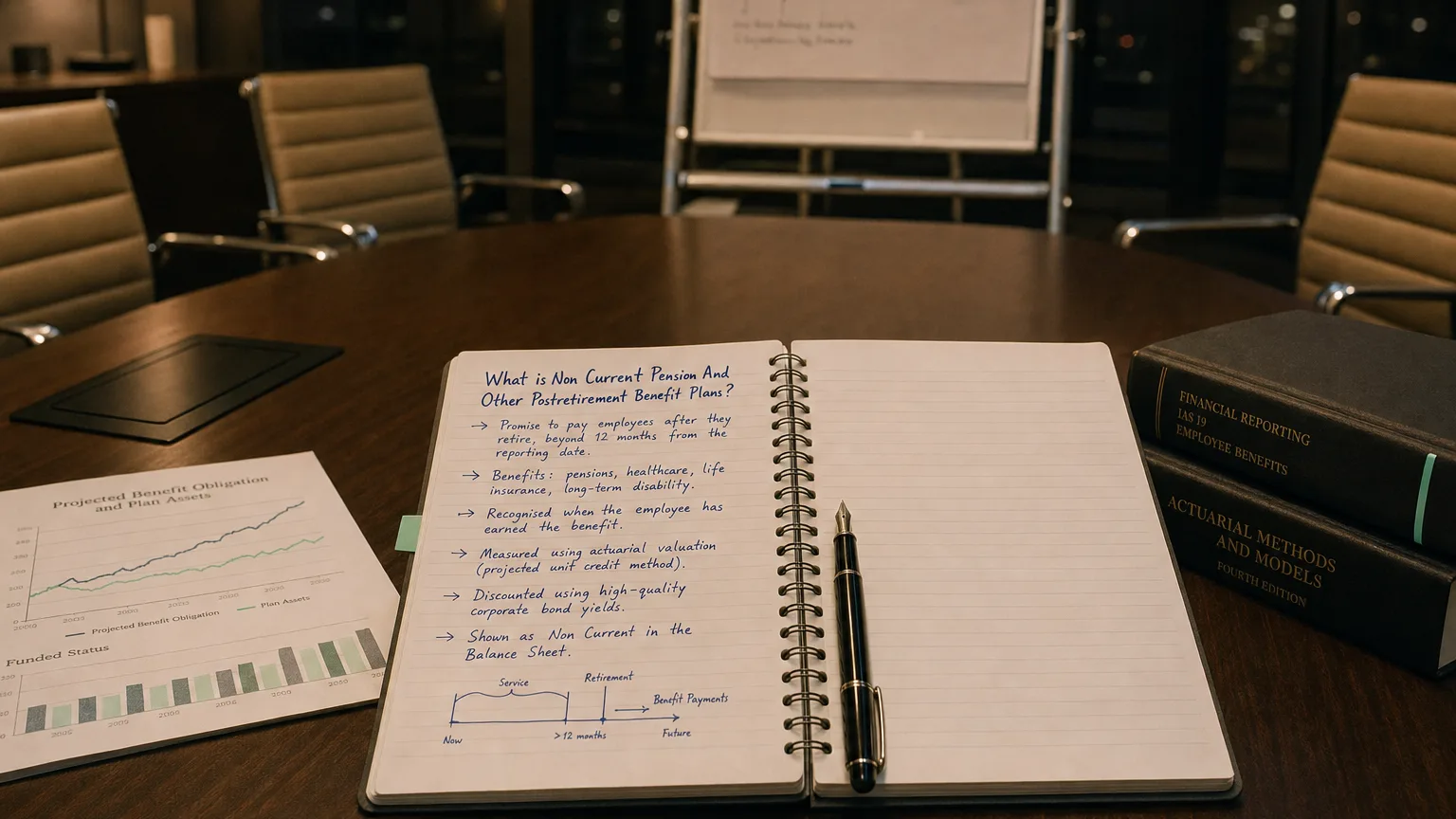

Non Current Pension and Other Postretirement Benefit Plans represent the long-term portion of a company’s obligations under defined benefit pension plans and other postretirement employee benefits (OPEB), such as retiree healthcare. These are the amounts expected to be settled more than 12 months after the balance sheet date, recorded as non-current liabilities reflecting the present value of future benefit payments minus plan assets (if underfunded).

What It Represents

This line captures the non-current portion of net liabilities from defined benefit plans where the company promises fixed or formula-based benefits to retirees.

- Pension plans: Retirement income based on salary/years of service

- OPEB: Post-employment benefits other than pensions (primarily healthcare)

The total obligation (Projected Benefit Obligation/PBO for pensions; Accumulated Postretirement Benefit Obligation/APBO for OPEB) is reduced by fair value of plan assets. Underfunded status → liability; overfunded → asset (rarely non-current asset).

Current portion (expected benefit payments within 12 months) is classified separately.

Accounting Treatment

Post-2006 (ASC 715/SFAS 158; IAS 19):

- Full funded status recognized on balance sheet

- Actuarial gains/losses, prior service costs initially to OCI (with amortization options under US GAAP)

- Service cost in operating expense; interest & expected return in non-operating

Discount rate based on high-quality corporate bonds; changes significantly impact liability size.

Lower discount rates increase liability (and vice versa).

“From the standpoint of an institution, the existence of a risk manager has less to do with actual risk reduction than it has to do with the impression of risk reduction.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

Balance Sheet Presentation

Shown under non-current liabilities as:

- ‘Non Current Pension and Other Postretirement Benefit Plans’

- ‘Long-Term Pension Obligations’

- Often aggregated with note breakdown

Extensive footnotes: PBO/APBO, plan assets, funded status, assumptions, expected contributions.

Key Components and Assumptions

- Discount rate (most sensitive)

- Expected long-term return on plan assets

- Salary increase assumptions (pensions)

- Healthcare cost trend rates (OPEB)

- Mortality/longevity tables

Small assumption changes can swing liability by hundreds of millions.

Analytical Implications

These obligations affect:

- Leverage and solvency (large hidden debt-like claims)

- Cash flow (required contributions)

- Earnings volatility (OCI recycling, assumption changes)

- Credit ratings and borrowing costs

- M&A valuation (adjust for off-balance risks historically)

Declining interest rates dramatically increase reported liabilities.