is a financial concept covered in this article. Short-Term Portion of Defined Benefit Pension and OPEB Obligations

It does not matter how frequently something succeeds if failure is too costly to bear.

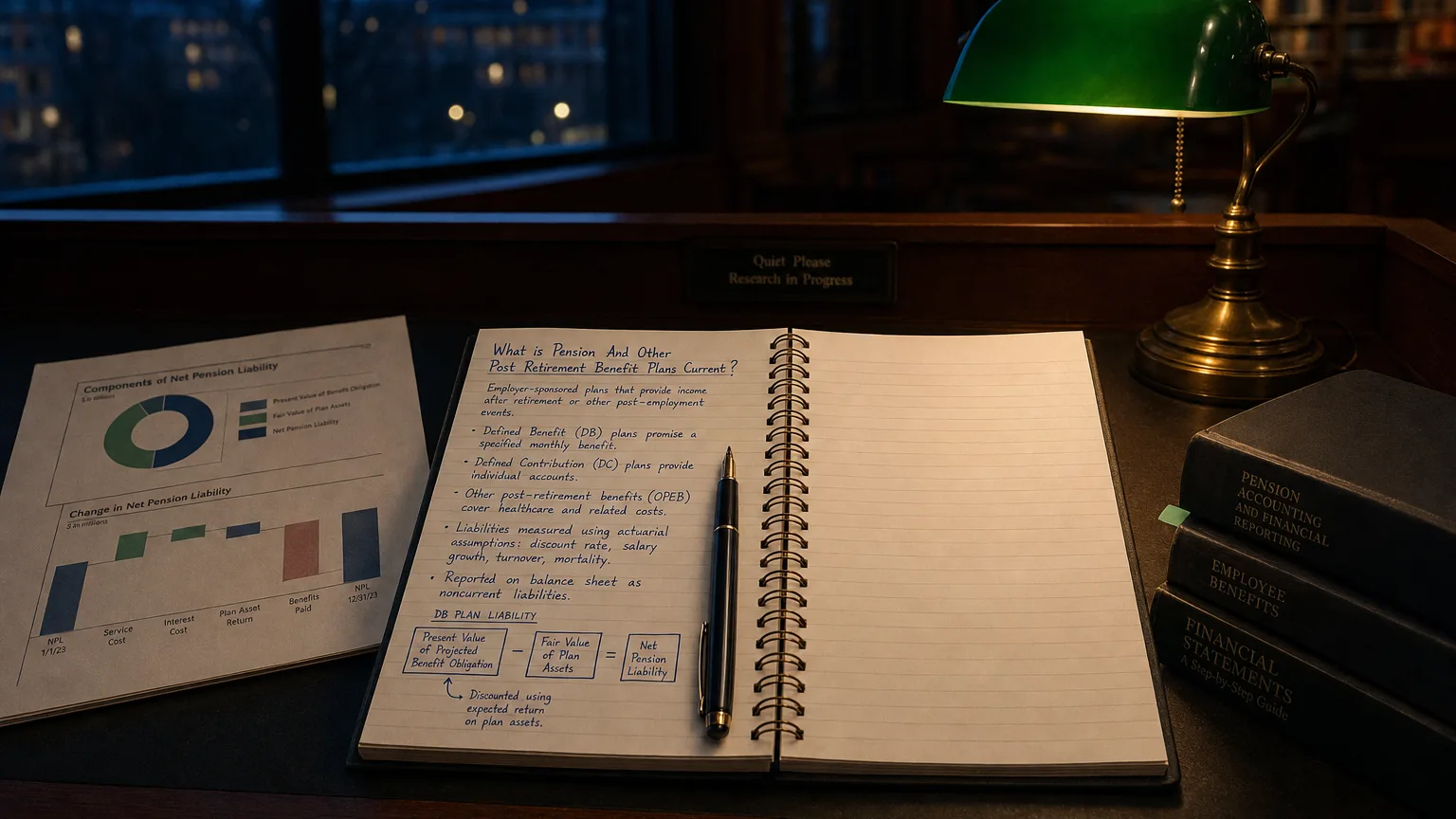

Pension and Other Post Retirement Benefit Plans Current represent the portion of a company’s net liability (or asset) from defined benefit pension plans and other postretirement employee benefits (OPEB, such as retiree healthcare) that is expected to be settled within the next 12 months or operating cycle. This current portion primarily covers anticipated benefit payments to retirees in the near term.

What It Represents

This line item captures the current portion of obligations under defined benefit plans, reflecting expected cash outflows for benefits in the coming year.

- Pension payments to current retirees

- Expected retiree healthcare claims (OPEB)

- Administrative costs payable short-term (sometimes included)

It is derived from the overall funded status but split based on expected timing of payments.

The bulk of pension/OPEB obligations is usually non-current due to long retiree lifespans.

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

Accounting and Classification

Under current standards:

- Full net funded status (PBO/APBO minus plan assets) on balance sheet

- Current portion = expected benefit payments within 12 months (undiscounted)

- No separate current liability if overfunded overall (rare)

- Contributions may reduce current portion

Expected payments disclosed in footnotes, driving current classification.

Balance Sheet Presentation

Appears under current liabilities as:

- ‘Pension and Other Post Retirement Benefit Plans Current’

- ‘Current Portion of Pension/OPEB Obligations’

- Sometimes aggregated in ‘Other Current Liabilities’

Footnotes provide expected payment schedule (next 5-10 years).

Key Drivers

- Number of current retirees

- Benefit formulas and healthcare usage

- Plan amendments or curtailments

- Actual vs. expected payments

- Demographic changes (mortality, retirement rates)

Analytical Implications

This current portion affects:

- Near-term liquidity (actual cash outflows)

- Working capital and current ratio

- Cash flow forecasting (operating vs. financing)

- Comparison to contributions (funding strategy)

- Overall leverage when combined with non-current

Rising current portion may indicate aging retiree population or underfunding catching up.