Classes of cash payments groups operating outflows into categories—payments to suppliers, employees, interest, and taxes—under the direct method. This shows gross cash paid for each cost driver rather than simply adjusting net income.

Pennies don't fall from heaven, they have to be earned here on earth.

Classes of Cash Payments refers to the breakdown of major types of cash outflows in the direct method presentation of operating cash flows. Instead of a single net operating cash flow figure, the direct method lists gross cash payments grouped into logical classes—such as payments to suppliers, employees, interest, taxes, and others—to show exactly where operating cash is going.

What It Really Shows

“Pennies don’t fall from heaven, they have to be earned here on earth.”

— Margaret Thatcher, Prime Minister of the United Kingdom (1979-1990) Speech at Lord Mayor’s Banquet, London (1979)

The direct method turns the black box of operating cash flow into a clear list: here’s how much cash actually went out the door to keep the business running.

Classes of cash payments group similar outflows so you see the big buckets—suppliers (inventory/services), employees (wages/benefits), interest, taxes, and everything else.

Indirect method hides these details in working capital changes.

Typical Classes You’ll See

- Payments to suppliers for goods and services (inventory, overhead)

- Payments to and on behalf of employees (salaries, benefits, payroll taxes)

- Interest paid

- Income taxes paid

- Other operating cash payments (royalties, leases, insurance)

Companies add or combine lines based on materiality.

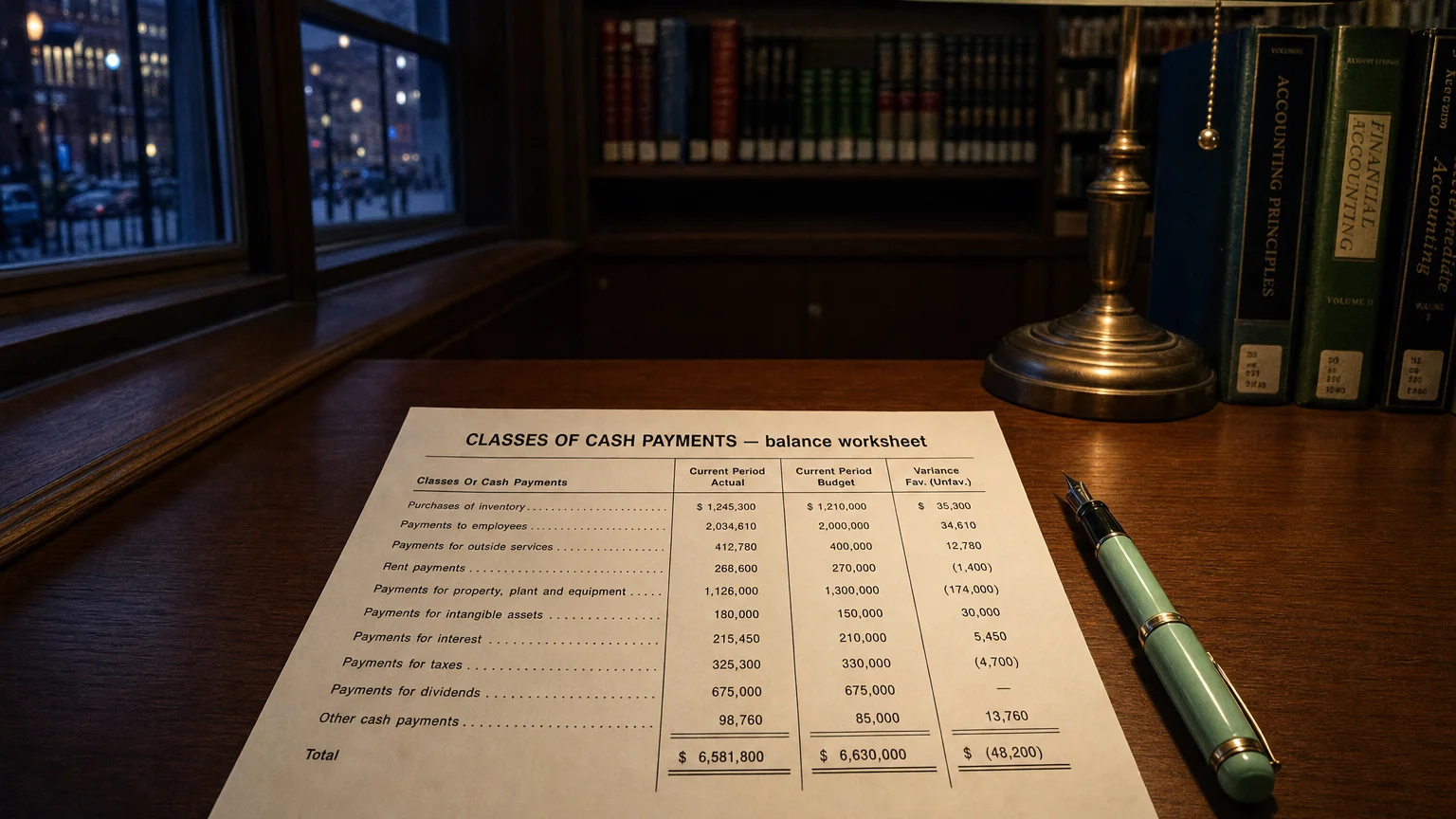

A Practical Example

Manufacturer using direct method:

- Payments to suppliers for goods and services: -$600M

- Payments to and on behalf of employees: -$300M

- Interest paid: -$40M

- Income taxes paid: -$50M

- Other operating payments: -$10M

- Total cash payments: -$1,000M

Pair with receipts to get net operating cash flow.

Why Some Companies Use It

- Clearer picture of cash operating cycle

- Better insight into major cost drivers

- Easier for non-accountants to understand

- Highlights supplier and employee cash timing

- IAS 7 encourages it

Still rare—most prefer indirect for simplicity.

Where It Appears

In cash flow statement operating section (direct method):

- Classes of cash receipts

- Classes of cash payments (detailed lines)

- Net cash from operating activities

IFRS companies sometimes provide it as supplemental.

What It Tells You

- True cash cost of goods sold and overhead

- Employee cash commitment

- Interest and tax cash burden

- Payment timing vs. accrual expenses

- Operational cash efficiency

Compare payments to suppliers vs. inventory change for purchasing patterns.

Q · 01How does the direct method differ from the indirect method?+

Q · 02Which accounting standards require classes of cash payments?+