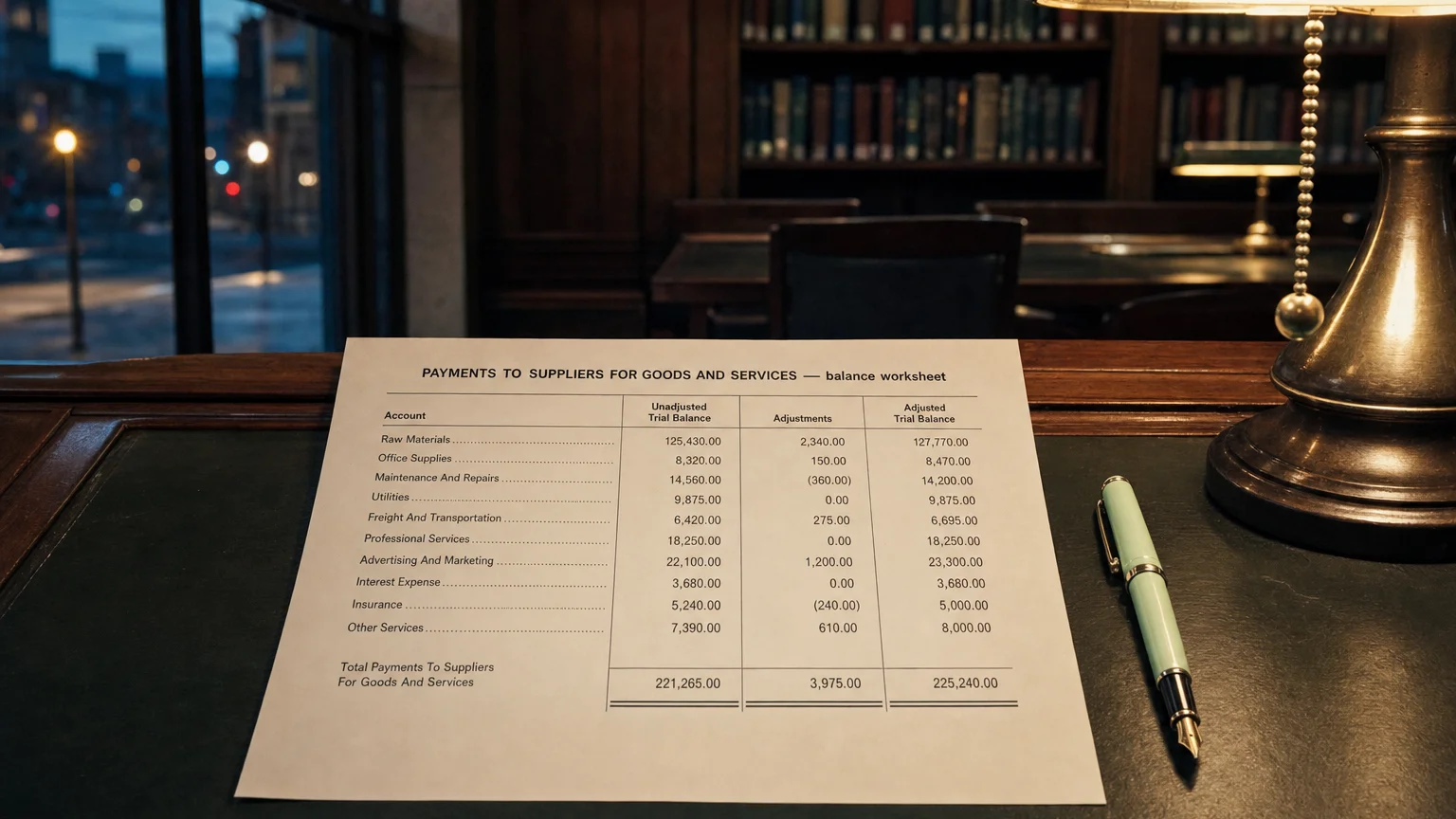

Payments to Suppliers for Goods and Services is a financial concept covered in this article. Cash Outflows to Vendors in Direct Method Operating Activities

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

Payments to Suppliers for Goods and Services is a major cash payment category in the direct-method cash flow statement. It represents the actual cash paid to vendors and suppliers for inventory purchases, raw materials, and operational services (like utilities, maintenance, or outsourced work) during the period. This line provides direct visibility into one of the largest operating cash outflows for most companies.

What It Represents

Payments to Suppliers for Goods and Services is the cash companies hand over to keep operations running—buying inventory to sell or materials to produce, plus services that support the business.

In the direct method, it’s one of the biggest payment lines, showing gross cash leaving for the supply chain.

Indirect method hides this in ‘Change in Inventory’ and ‘Change in Accounts Payable’.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

What Typically Goes In

- Purchases of inventory or raw materials

- Payments for freight, shipping, customs

- Outsourced manufacturing or assembly

- Utilities, telecom, maintenance contracts

- Professional services (non-employee, e.g., consulting, legal for operations)

- Marketing services or agency fees

Employee-related payments go to separate ‘Payments to/on behalf of employees’ line.

A Practical Example

Retail chain using direct method:

- Buys $800M merchandise from suppliers

- Pays $50M freight and duties

- Outsourced $20M store maintenance

- Payments to Suppliers for Goods and Services: -$870M

You see the true cash cost of goods and support services.

Direct Method Context

In direct method operating section:

- Cash receipts from customers

- Payments to Suppliers for Goods and Services

- Payments to/on behalf of employees

- Interest/taxes paid

- Other payments

- = Net operating cash flow

Gross view—see supplier cash separate from payroll.

Why It Matters

- Major operating cash drain visibility

- Supply chain cash commitment

- Comparison to inventory change (purchasing timing)

- Vendor payment terms insight

- COGS cash vs. accrual difference

What to Watch For

- Growth vs. sales (inventory buildup?)

- As % of receipts (gross margin pressure?)

- Trend with payables change (payment speed)

- Seasonality (pre-holiday inventory buys)

- Outsourcing shift (services rising?)

Payments rising faster than sales may signal cost inflation or overbuying.

Q · 01What is Payments To Suppliers For Goods And Services?+