is a financial concept covered in this article. The Parent's Share of Earnings from Non-Consolidated Investments

You can't take the same actions as everyone else and expect to outperform.

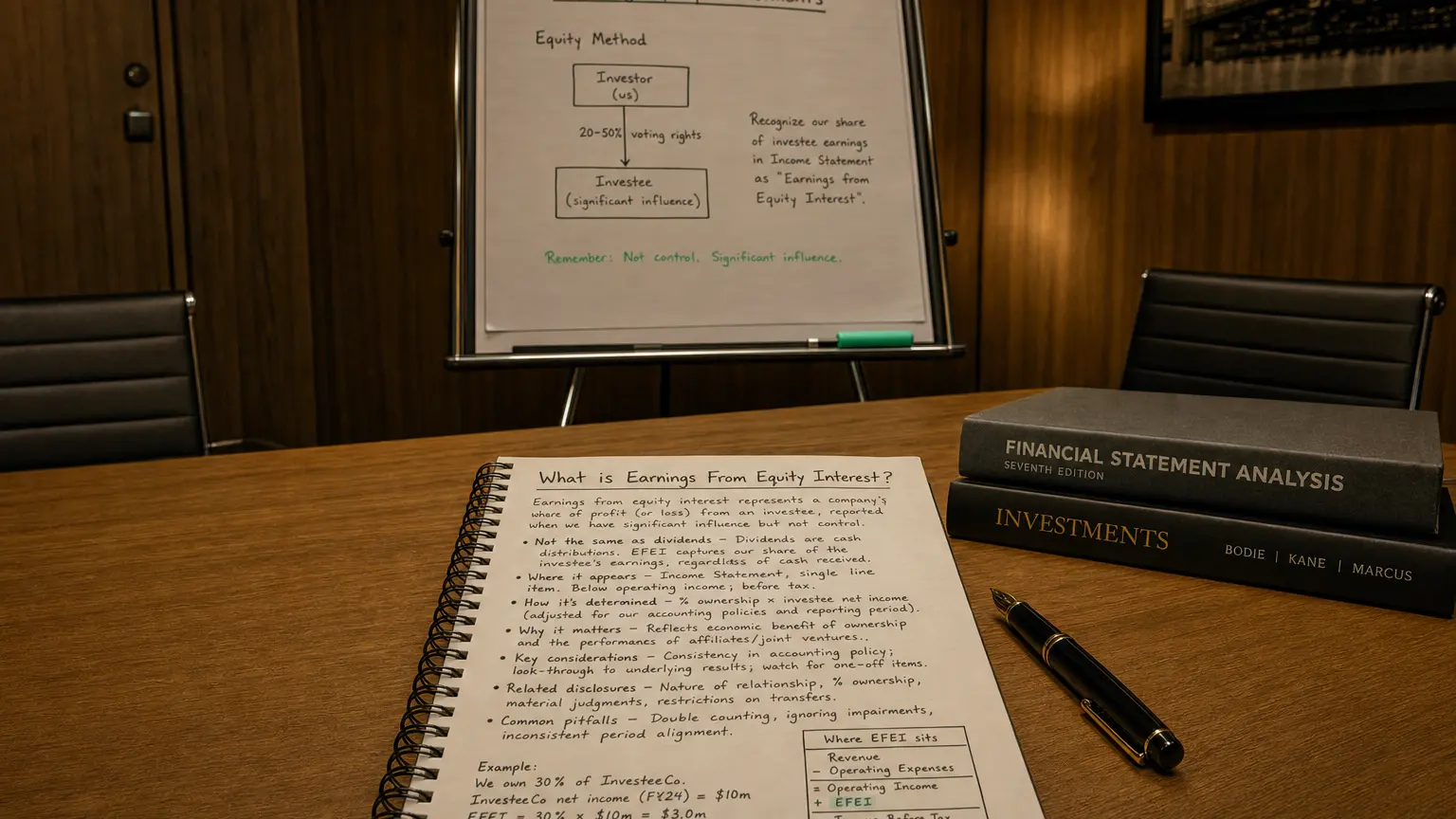

Earnings From Equity Interest represents a company’s proportionate share of the net income (or loss) generated by its investments in associates or joint ventures where it has significant influence but not full control (typically 20–50% ownership). Under the equity method of accounting, the investor recognizes this share as a single line item in the income statement, usually in the non-operating section. It increases (or decreases) the carrying value of the investment on the balance sheet and directly impacts the parent’s pretax income without consolidating the investee’s full revenues and expenses. This metric highlights the contribution of strategic investments to overall profitability.

What is Earnings From Equity Interest?

Earnings From Equity Interest is the investor’s share of an equity-method investee’s net profit or loss. It is recognized in the period the investee earns it, even if no dividends are received.

Under US GAAP (ASC 323) and IFRS (IAS 28), the equity method applies when significant influence exists—presumed at 20%+ voting power unless rebutted. The investor does not consolidate line-by-line but picks up its percentage of the investee’s bottom-line results.

This income is typically reported pre-tax at the investor level because the investee has already accounted for its own taxes.

Common in industries with alliances: automotive (supplier stakes), energy (joint ventures), beverages (bottling partners).

“You can’t take the same actions as everyone else and expect to outperform.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘Dare to Be Great’ (2006)

How the Equity Method Operates

Mechanics of recognition:

Key Accounting Steps

- Initial investment recorded at cost

- Increase investment and recognize income for share of investee earnings

- Decrease investment for dividends received (not income)

- Decrease for share of losses (generally not below zero unless obligated)

- Adjust for basis differences (e.g., fair value uplifts amortized)

Formula: Earnings From Equity Interest = Investee Net Income × Investor Ownership % ± Adjustments (e.g., intercompany profit elimination, amortization)

Tip: Dividends are cash inflow but reduce the investment balance—no P&L impact.

Examples

Example 1: Profitable Associate

Company owns 25% of Associate Z.

Associate Z net income: 160M × 25% = +40M.

Example 2: Loss-Making JV

Company owns 40% of JV W.

JV W net loss: −100M × 40% = −$40M. Reduces parent’s pretax income; investment balance decreases (to zero if fully eroded).

Example 3: Basis Adjustment

Purchase included $50M excess over book value attributed to depreciable assets.

Annual amortization: 30M. Adjusted Earnings From Equity Interest = 5M = +$25M.

Positive contributions enhance earnings without adding revenue; losses can drag even if investee is strategic.

Presentation and Impact

Typically reported as a single line in the non-operating section:

Common Labels

- Equity in earnings of unconsolidated affiliates

- Share of earnings from equity-method investments

- Earnings from equity interests

Flows directly into pretax income; no associated revenue or operating expenses.

Importance in Financial Analysis

This metric is valuable for:

- Gauging performance of strategic partnerships

- Understanding earnings sources beyond wholly-owned operations

- Assessing volatility from cyclical investees

- Evaluating ‘look-through’ earnings in conglomerates

Analysts often include it in core earnings (as recurring) but may adjust for non-controlling aspects. Large negative values warrant scrutiny of investee health.

Warning: Significant equity earnings can flatter margins (high ROE with low asset base)—compare consolidated vs. equity-method contributions.