The Systematic Write-Down of Premiums or Accretion of Discounts on Debt Securities

In investing, you get what you don't pay for. Costs matter enormously.

Securities Amortization refers to the gradual adjustment of the carrying value of debt securities (primarily bonds or other fixed-income investments) toward their face value over time. When a company purchases a bond at a price above par (premium) or below par (discount), the difference is amortized over the remaining life of the security. This amortization is recognized as an adjustment to interest income (or expense, if classified as held-to-maturity or available-for-sale under certain conditions), affecting reported earnings. It ensures that the effective yield (rather than the coupon rate) is reflected in financial results, providing a more accurate picture of investment performance.

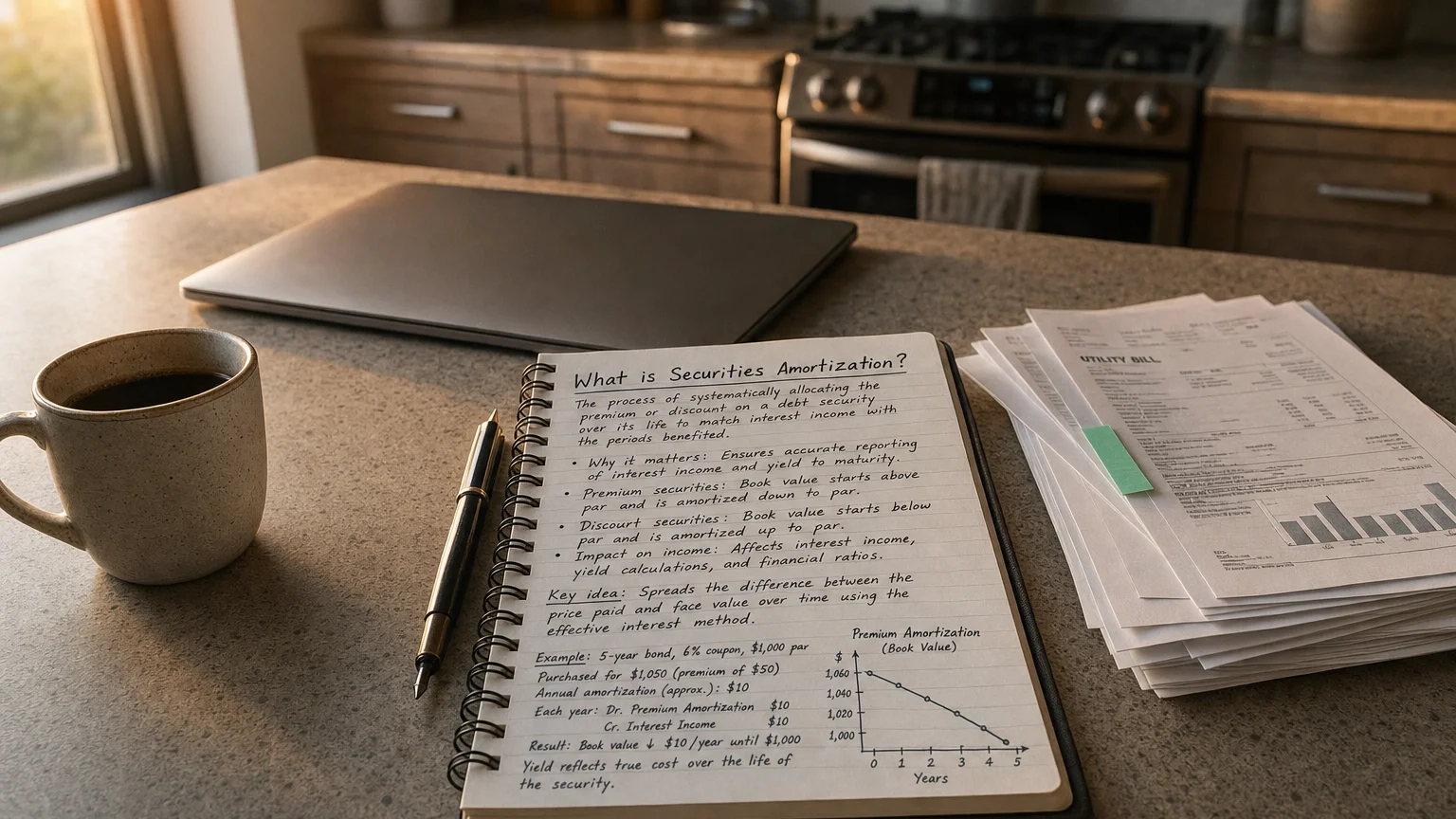

What is Securities Amortization?

Securities amortization is the process of systematically allocating the premium paid or discount received when purchasing a debt security over its remaining term to maturity.

A premium occurs when the purchase price exceeds face value (e.g., bond bought at 105 when par is 100). A discount occurs when the price is below face value (e.g., bought at 95).

Under US GAAP (ASC 320) and IFRS (IFRS 9), the preferred method is the effective interest method, which amortizes the premium/discount in a way that produces a constant yield on the carrying amount.

Amortization affects non-operating interest income for most corporate investors holding debt securities in their investment portfolio.

“In investing, you get what you don’t pay for. Costs matter enormously.”

— John C. Bogle, Founder, The Vanguard Group Common Sense on Mutual Funds (1999)

How Securities Amortization Works

Using the effective interest method:

Key Steps

- Determine the effective yield at purchase (internal rate of return)

- Calculate periodic interest income = Carrying Value × Effective Yield

- Cash coupon received = Face Value × Coupon Rate

- Amortization = Cash Coupon − Interest Income (for premium) or Interest Income − Cash Coupon (for discount)

Premium bonds: Amortization reduces interest income and carrying value. Discount bonds: Amortization increases interest income and carrying value.

Formula: New Carrying Value = Previous Carrying Value + Discount Amortization − Premium Amortization

Straight-line amortization is allowed only if results are not materially different from effective interest method.

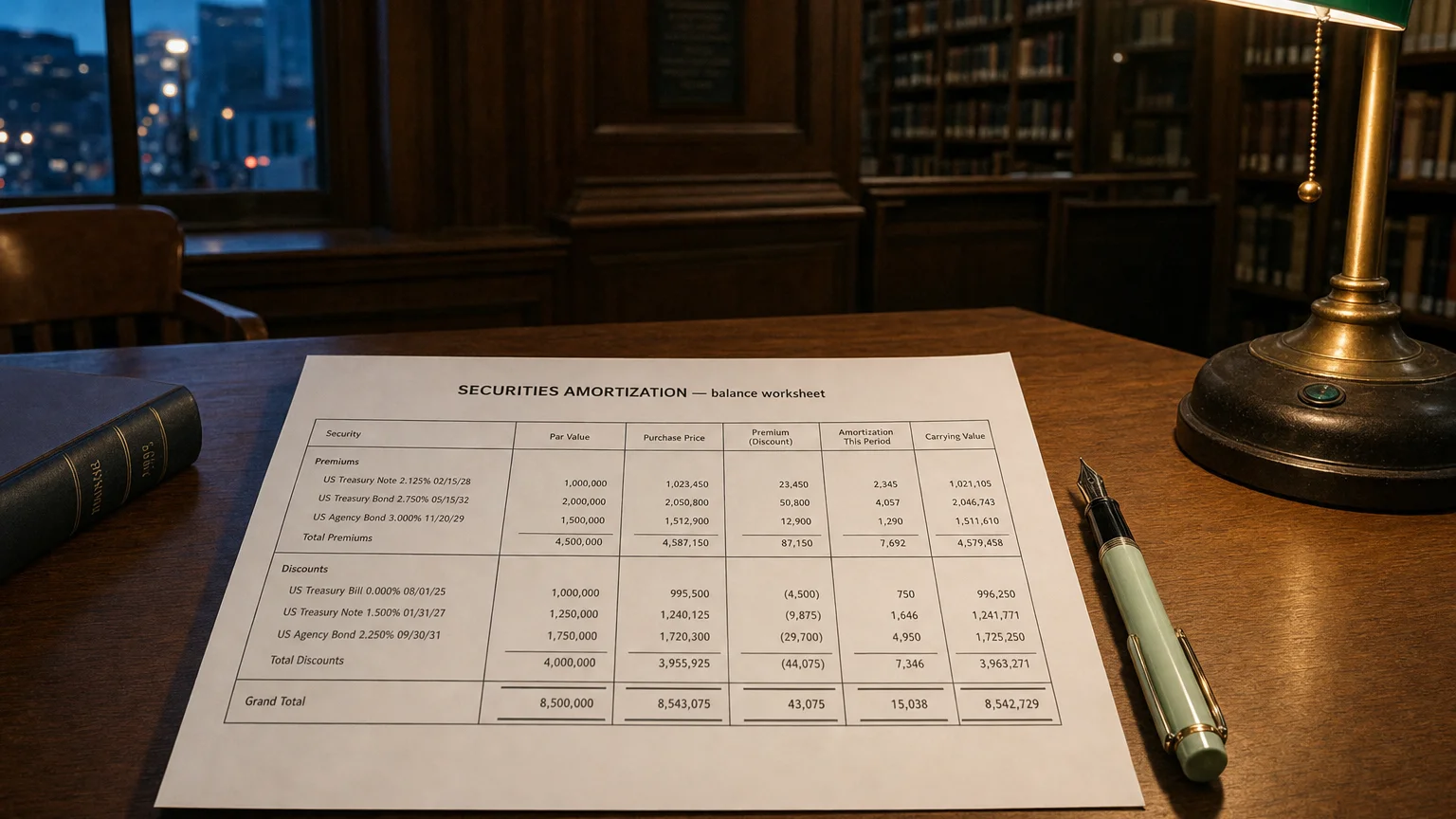

Examples of Securities Amortization

Example 1: Premium Bond

Company buys 10.5M (premium $0.5M), 5-year maturity, 4% coupon, effective yield 3%.

Annual cash coupon: 315,000 (10.5M × 3%) Premium Amortization: 315K = 10.415M.

Example 2: Discount Bond

Buys 9.5M (discount $0.5M), 5-year, 4% coupon, effective yield 5.4%.

Annual cash coupon: 513,000 (9.5M × 5.4%) Discount Amortization: 400K = 9.613M.

Over life, carrying value converges to $10M face value at maturity.

Classification and Reporting

Amortization typically appears as an adjustment within:

Common Line Items

- Interest Income (most corporate investors)

- Interest Income Non-Operating

- Other Non-Operating Income/Expenses

It contributes to net non-operating interest income and ultimately pretax income.

Importance in Financial Analysis

Analysts consider securities amortization because:

- Premium amortization reduces reported interest yields

- Discount accretion inflates yields

- Large portfolios can materially affect non-operating income

- Cash interest received differs from reported income

Cash-rich companies (tech, pharma) often hold large bond portfolios—amortization can swing non-operating results without cash impact.

Warning: Falling interest rates increase bond premiums (more amortization drag); rising rates increase discounts (accretion boost).

In normalized earnings, amortization is usually left in as it reflects economic yield on investments.

Q · 01What is Securities Amortization?+