Excess Tax Benefit from Stock-Based Compensation is a financial concept covered in this article.

Pennies don't fall from heaven, they have to be earned here on earth.

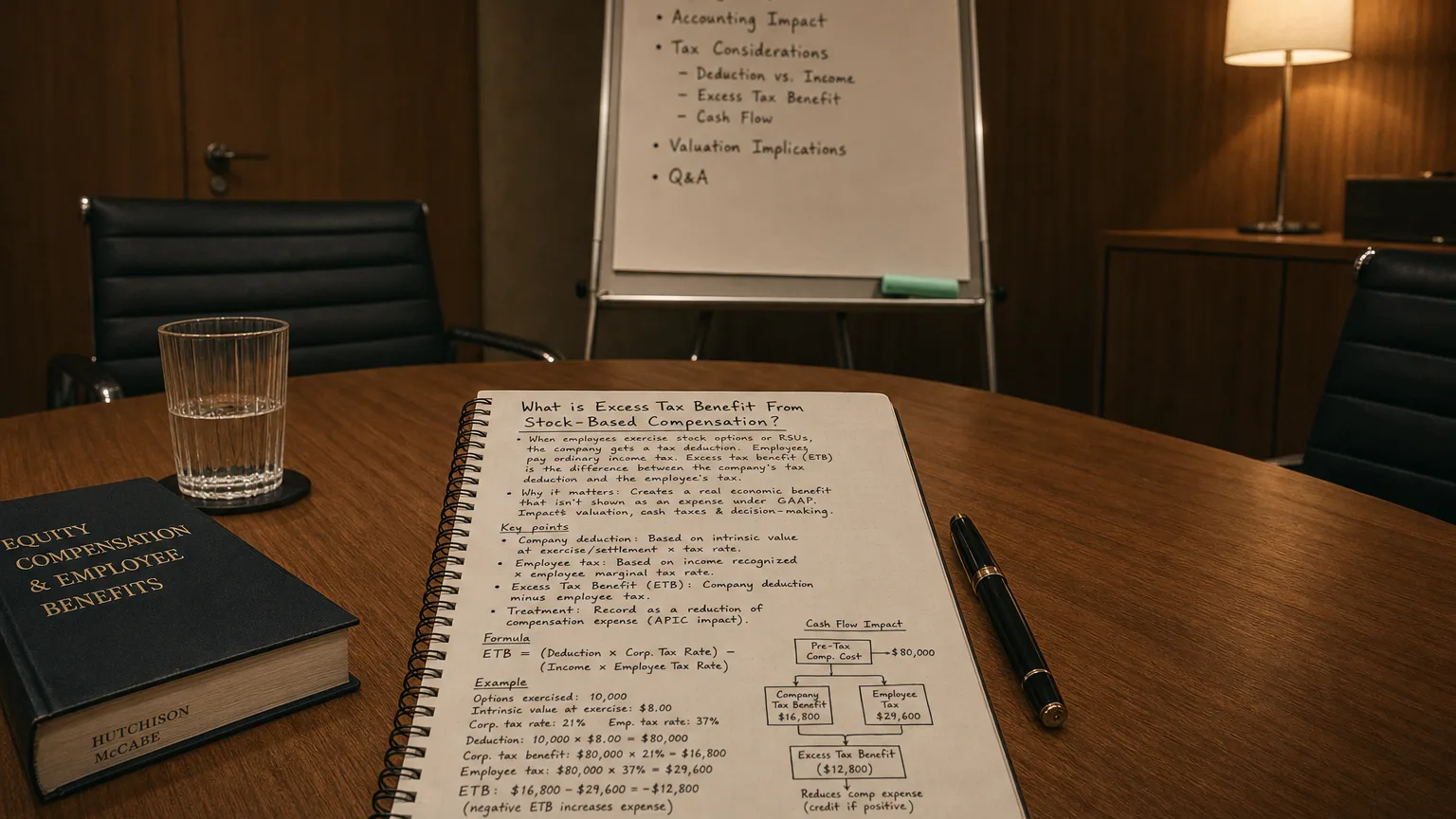

Excess Tax Benefit from Stock-Based Compensation (also called Windfall Tax Benefit) was the additional tax deduction a company received when employees exercised stock options or vested in restricted stock/RSUs at a share price higher than the grant-date fair value used for book expense. This ‘excess’ created a cash tax saving that was reported as a financing cash inflow under old US GAAP rules (pre-2017).

How It Used to Work

Before 2017, companies expensed stock options at grant-date fair value (book expense). When exercised, the actual tax deduction was based on the intrinsic value (market price − strike).

If market price was higher, the extra deduction created a tax shield—the ‘excess tax benefit’.

This windfall cash saving went to financing cash flow and increased Additional Paid-In Capital.

A Clear Example

“Pennies don’t fall from heaven, they have to be earned here on earth.”

— Margaret Thatcher, Prime Minister of the United Kingdom Speech to the Conservative Party Conference (1979)

Employee gets options on 10,000 shares at $20 strike.

- Grant-date fair value: 100k book compensation expense over vesting

- Exercise when stock 30/share = $300k tax deduction

- Tax rate 30% → $90k actual tax saving

- Book expense deduction only 100k × 30%)

- Excess Tax Benefit: $60k

Pre-2017: +60k reduces income tax expense (operating).

The Big Change in 2017

ASU 2016-09 eliminated the APIC pool and excess benefit concept.

- All tax effects (excess or shortfall) now in income tax expense (operating)

- No more financing cash flow boost from exercises

- Shortfalls reduce tax expense (can create volatility)

- Simplified but more earnings swings

Tech companies with big option programs felt the biggest shift.

Where You’d See It (Old Statements)

In pre-2017 cash flow statements:

- Financing section: ‘Excess Tax Benefit from Stock-Based Compensation’

- Often material for growth/tech firms

- Boosted financing cash flow and OCF indirectly (via APIC)

Now: All in operating tax expense—no separate line.

Why It Mattered

- Non-cash boost to financing cash flow

- Increased APIC (equity)

- Made OCF look stronger indirectly

- Rewarded rising stock prices with tax savings

- Common in Silicon Valley option-heavy cultures

What to Look For in Old Data

- Size relative to stock comp expense (high = big stock price gains)

- Trend with option exercises

- Impact on financing cash flow quality

- Comparison pre/post-2017 (OCF volatility increased)

Pre-2017 excess benefits flattered financing cash—now gone.