Held-to-Maturity Securities is a financial concept covered in this article. Debt Investments Intended to Be Held Until Maturity

If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes.

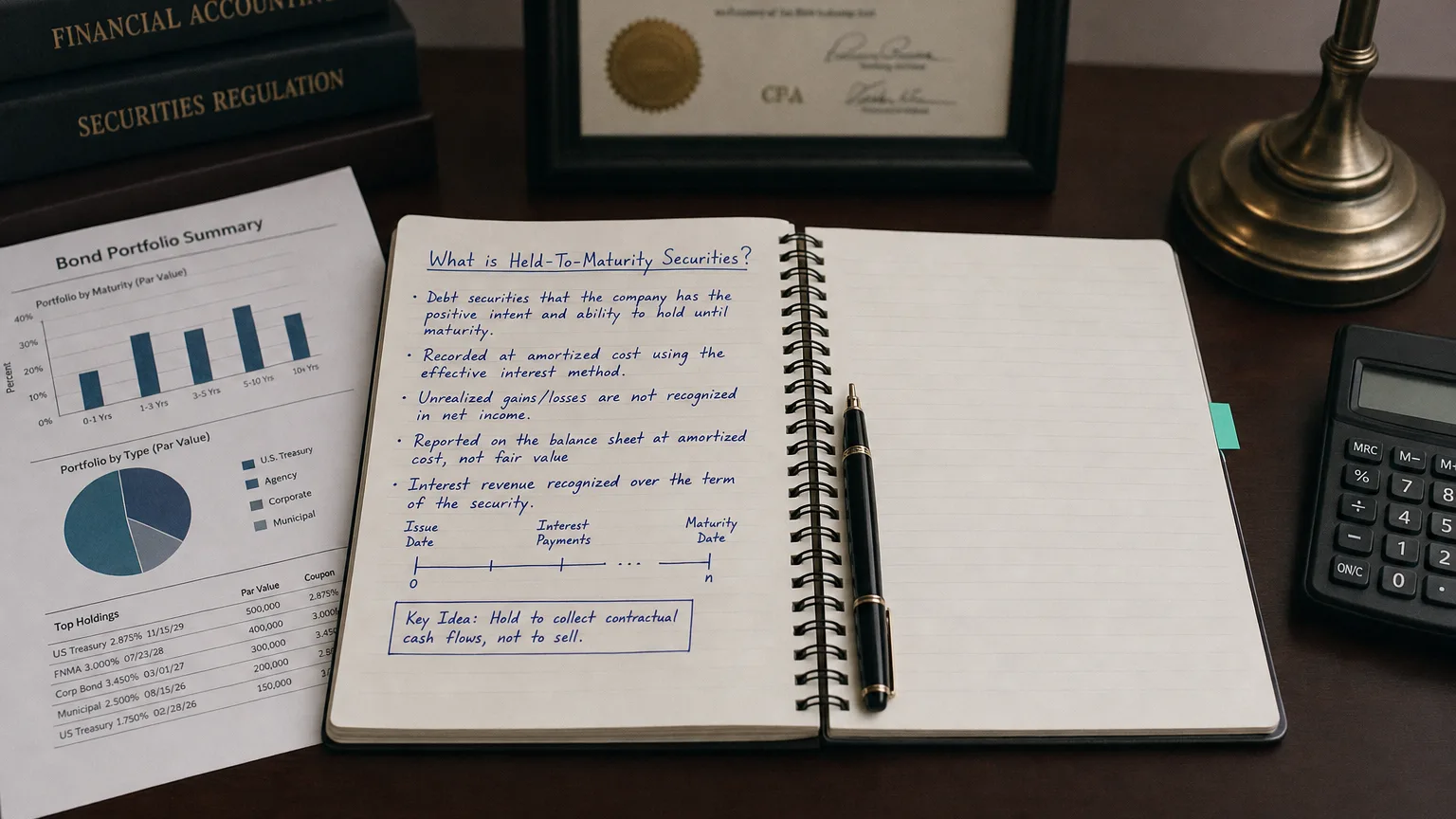

Held-to-Maturity (HTM) Securities are debt investments—like bonds or notes—that a company buys with the clear intent and ability to keep until they mature. Unlike stocks or trading bonds, these are not meant for quick sales. You record them at amortized cost on the balance sheet, not bouncing around with market prices every quarter.

Why Companies Choose HTM

Imagine you run a bank and buy a 10-year government bond paying 4%. You plan to collect every interest payment and get your principal back at the end. You don’t want market swings messing with your books every quarter.

HTM lets you lock in that steady yield and avoid volatility from interest rate changes. It’s perfect for matching long-term liabilities—like insurance claims or pension payouts—with predictable bond cash flows.

A Simple Example

Your company buys a 9.5 million. It matures in 8 years and pays 5% interest annually.

- Classify as HTM → record at $9.5M

- Each year: collect interest cash, amortize discount (add to carrying value)

- After 8 years: carrying value reaches 10M back

- Even if market rates drop and bond value jumps to $11M → your books stay calm at amortized cost

No mark-to-market noise—just steady interest income and gradual move toward face value.

If rates rise and bond falls to $9M on market → you still show close to original cost, no loss hits equity.

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Annual Report (1996)

The Strict Rules

You can’t just slap HTM on anything—you must prove intent and ability to hold to maturity.

- No recent sales of HTM securities (taints the whole portfolio)

- Financial capacity to hold despite rate changes

- Positive intent—no plans to sell for profit or liquidity

- Securities must have fixed payments and maturity date

Break the rules (sell early) → you may lose HTM classification for all similar securities.

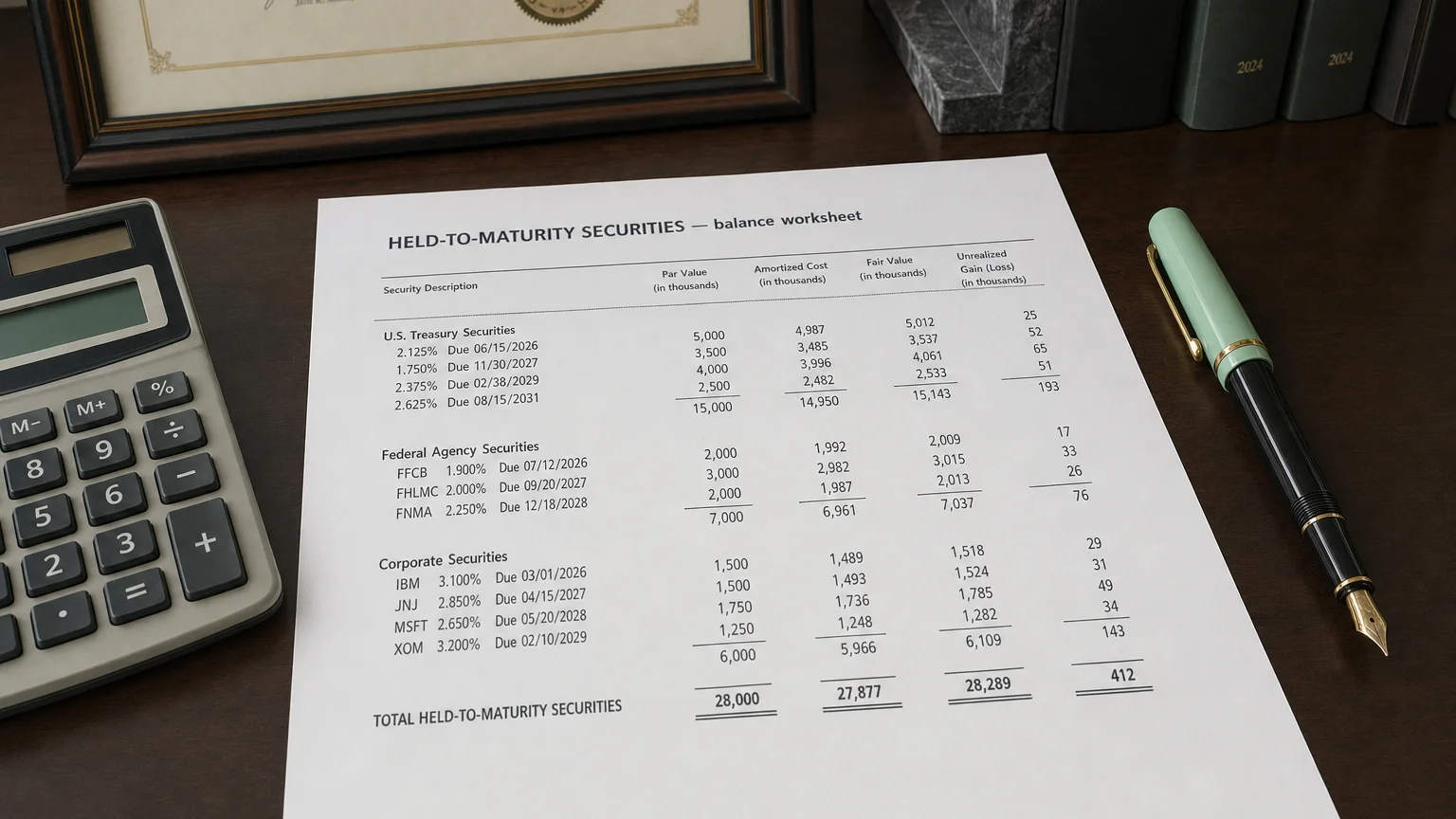

How It Looks on the Books

- Initial recording: purchase price (cost)

- Amortize premium/discount over life using effective interest method

- Interest income each period

- No fair value adjustments or OCI entries

- Impairment tested if credit loss expected

Balance sheet line: usually under non-current investments, separate from trading or available-for-sale.

Comparison with Other Categories

Held-to-Maturity

- Amortized cost

- No volatility

- Strict hold intent

Available-for-Sale

- Fair value

- Unrealized gains/losses to OCI

Trading

- Fair value

- Changes to income

What to Watch For

- Stable earnings (no market noise)

- Interest rate risk hidden (value can drop sharply if rates rise)

- Liquidity illusion (can’t sell without accounting penalty)

- Credit risk still matters (impairment possible)

- Banks/insurers love HTM for matching liabilities

Big HTM portfolio in rising rate environment = potential unrealized losses if forced to sell.

Q · 01What is Held-to-Maturity Securities?+