Gain/Loss on Investment Securities is a financial concept covered in this article. Realized and Unrealized Changes in Value of Debt and Equity Investments

Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

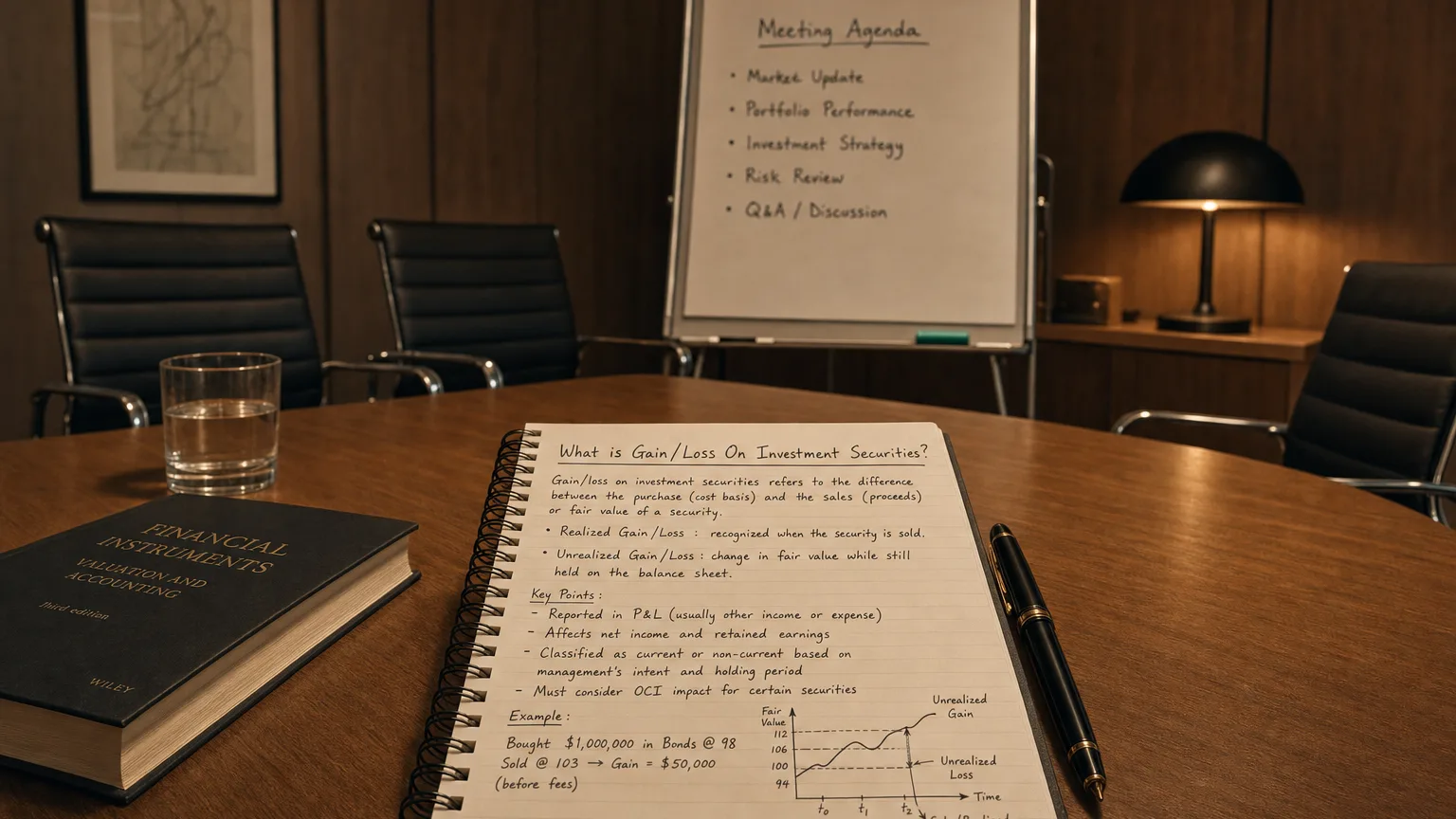

Gain/Loss on Investment Securities captures the net impact on earnings from changes in the value of a company’s debt and equity investment portfolio. It includes both realized gains/losses (from actual sales) and, depending on classification, unrealized mark-to-market adjustments. This line reflects investment performance and market volatility flowing through the income statement.

What Drives This Line

Every time a company sells an investment security, it locks in a realized gain or loss (sale price vs. carrying value).

For securities classified as trading or FVTPL, even holding them triggers unrealized gains/losses as fair value changes each period.

The net of all these flows through earnings, creating volatility unrelated to core operations.

“Only unpopular assets can be truly cheap. And those that are in favor are likely to be priced high.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

A Real-World Example

A bank holds a mix of bonds and stocks in its investment portfolio.

- Sells bonds bought at 11M cash → +$1M realized gain

- Trading stocks rise in value 2M unrealized gain

- Credit spreads widen on other bonds → -$1.5M unrealized loss

- Net Gain/Loss on Investment Securities: +$1.5M

Earnings boosted $1.5M from portfolio performance, not lending or fees.

Classification Determines Impact

Trading / FVTPL

- All changes (realized + unrealized) → P&L

- Highest earnings volatility

Available-for-Sale / FVOCI Debt

- Unrealized → OCI

- Realized → P&L on sale

Held-to-Maturity

- No unrealized

- Only realized on sale (rare)

Where It Appears

Income statement:

- ‘Net Gain/Loss on Investment Securities’

- ‘Investment Securities Gains/Losses’

- ‘Trading Revenue’ (banks)

- Often in ‘Other non-operating income/expense’

Cash flow: Realized portion in investing; unrealized non-cash.

Who Sees Big Numbers Here

- Banks (trading and investment portfolios)

- Insurance companies (large bond holdings)

- Corporate treasuries with active investment management

- Investment firms

What to Watch For

- Volatility trend (rate environment?)

- Realized vs. unrealized split

- Size vs. core earnings (distortion?)

- Link to interest rate moves

- Credit loss component (deteriorating holdings?)

Large gains can mask weak core operations; losses signal portfolio stress.