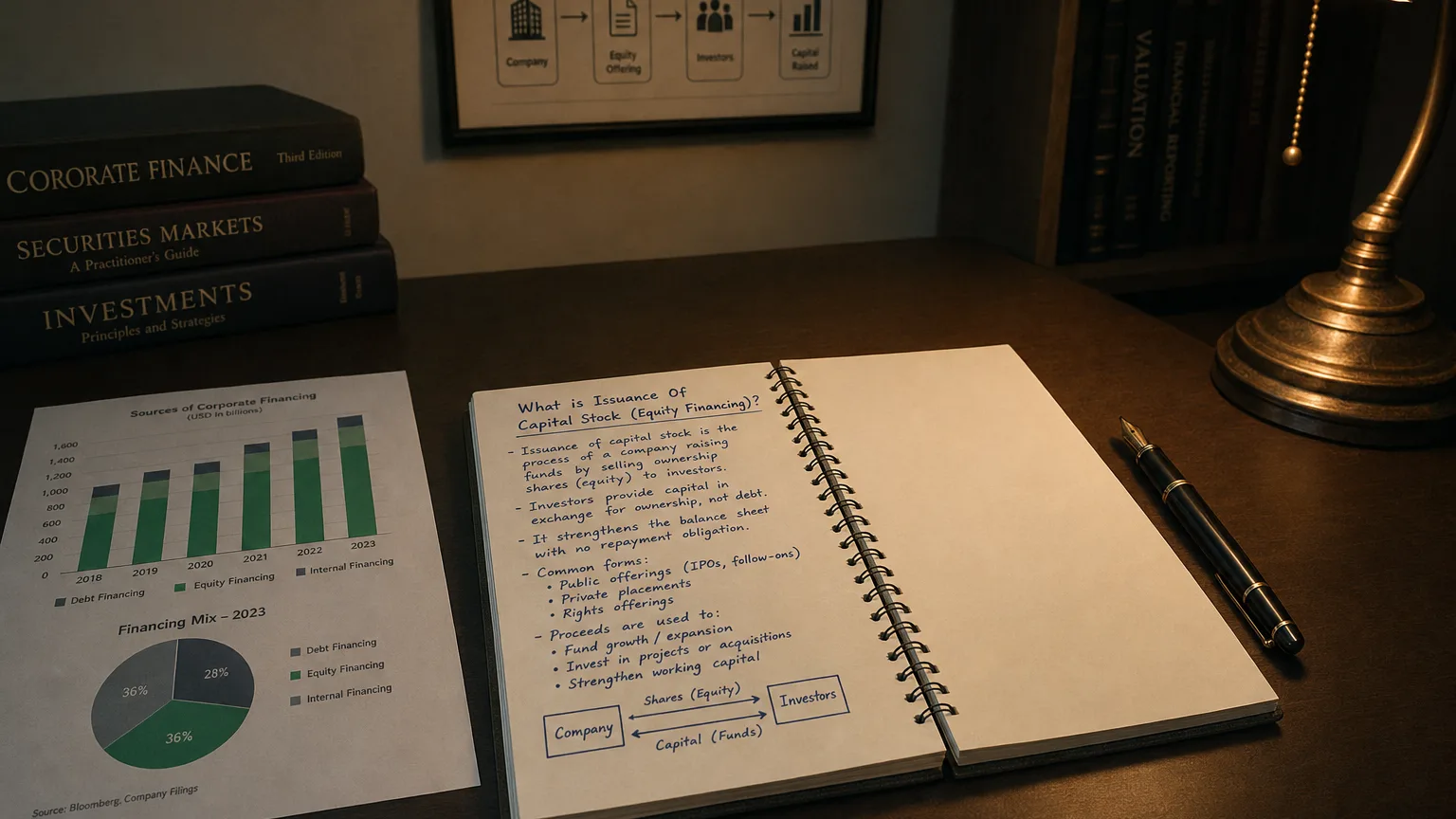

A core financing activity where a company raises permanent capital by selling new shares of its stock to investors, resulting in a cash inflow and an increase i

Show me the incentive and I'll show you the outcome.

(sometimes labeled “Proceeds from issuance of common (or preferred) stock,” “Equity financing,” or simply “Share issuance”)

| Key Point | Summary |

|---|---|

| What it is | The cash a company receives from selling new shares of its own equity—common or preferred stock—to investors. |

| Where it appears | Financing Activities section of the Statement of Cash Flows, shown as a positive (inflow) amount because cash comes into the business. |

| Why companies do it | Raise permanent capital to: 1) fund growth projects or acquisitions, 2) strengthen the balance‑sheet (pay down debt, boost liquidity), 3) comply with regulatory capital requirements, or 4) give early investors a partial exit. |

| Impact on the financials | • Cash ↑ by the proceeds received. • Shareholders’ equity ↑ by the same amount (usually split between common/preferred stock at par value and additional paid‑in capital). • Shares outstanding ↑, which dilutes existing owners unless they buy additional shares. |

| Common forms | • Initial Public Offering (IPO) • Seasoned / secondary offering (new shares sold after the IPO) • Private placement to strategic or institutional investors • Employee option or warrant exercises (cash paid in on exercise shows up here) |

1. Definition and Mechanics

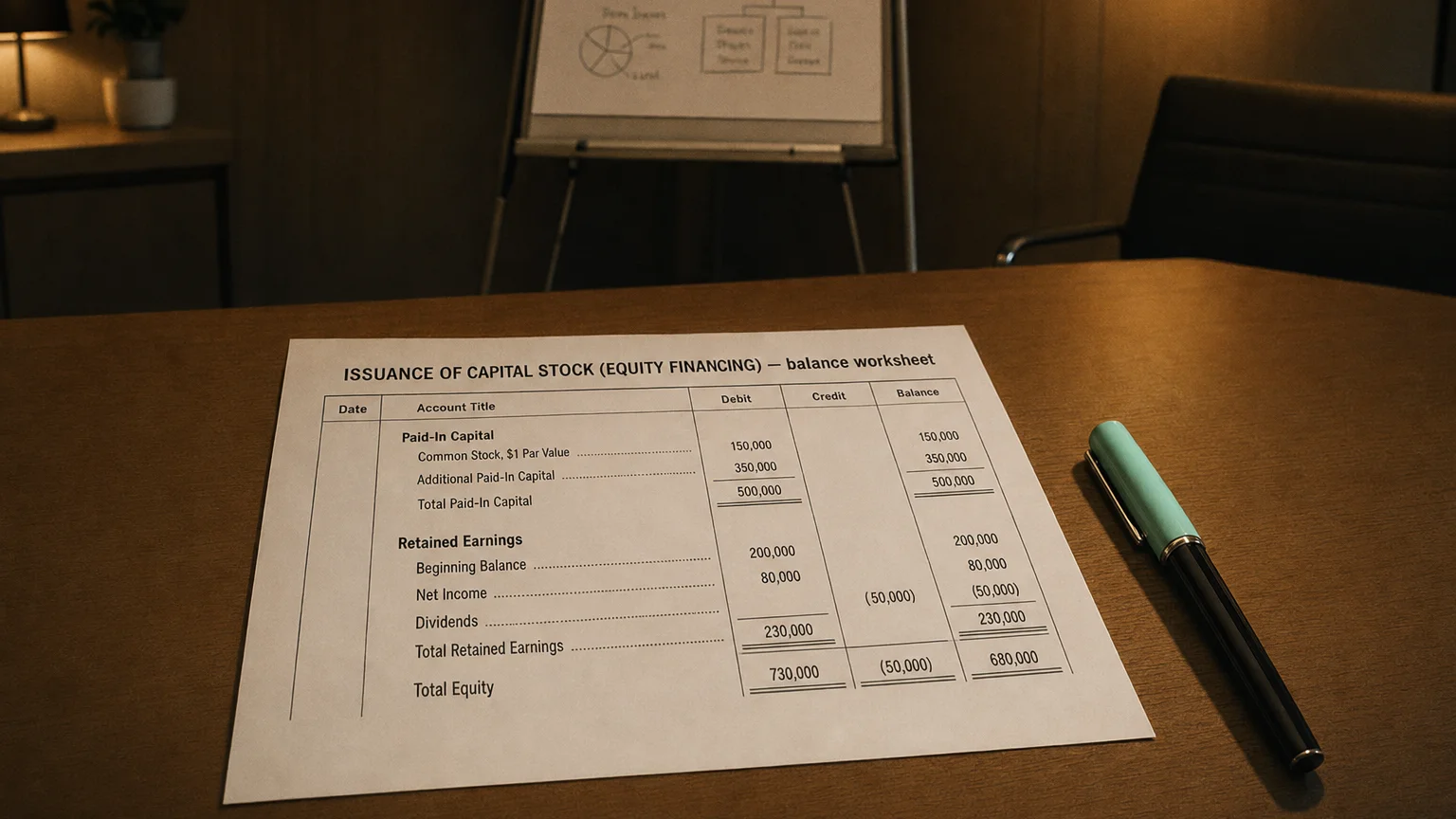

When a corporation issues (sells) its own shares, it is exchanging pieces of ownership for cash. Legally this creates contributed capital: a share capital account for par value and an additional paid‑in capital (APIC) account for any amount paid above par. The total cash received is what you see on the cash‑flow statement line “Issuance of capital stock.”

Example – If Alpha Inc. sells 1 million new shares at $20 each, it collects $20 million in cash:

• Cash‑flow statement (Financing): +$20 m

• Balance sheet: Common Stock (par) +$1 m, APIC +$19 m, Cash +$20 m, Shares outstanding +1 m

Issuance costs (underwriting fees, legal, filings) are usually netted against APIC rather than shown as an expense, so the cash inflow may be reported net of costs.

2. Placement in the Statement of Cash Flows

The Financing Activities section captures cash flows between the company and its providers of capital—both debt and equity. Equity inflows (stock issuances) and outflows (dividends, share buybacks) sit side‑by‑side with debt inflows/outflows. A typical snippet:

Cash flows from financing activities

Proceeds from issuance of common stock + 20,000

Dividends paid – 4,000

Repurchase of common stock – 3,500

Proceeds from long‑term debt + 10,000

Repayment of long‑term debt – 2,000

Net cash provided by (used in) financing + 20,500

3. Reasons Companies Issue Equity

| Situation | Rationale |

|---|---|

| Growth capital | Large projects, R&D, entering new markets, or funding acquisitions that exceed available cash or borrowing capacity. |

| De‑leveraging / liquidity boost | Reduce debt load, improve leverage ratios, or raise liquidity buffers—common after a downturn or before an upgrade in credit rating. |

| Regulatory or strategic requirements | Banks must meet capital adequacy ratios; utilities may issue equity to finance regulated asset bases. |

| Strengthening balance‑sheet before going public or acquiring | An IPO itself is an equity issuance; proceeds often repay debt or fund expansion. |

| Employee stock option exercises | Cash received from employees exercising options (if paid in cash) appears here—even though dilutive, it injects cash. |

4. Effects on Shareholders and Key Ratios

Positive for the company:

-

Cash reserves enlarge—immediate liquidity.

-

Interest burden avoided—unlike debt, equity has no mandatory repayment.

Potential downsides for existing shareholders:

-

Dilution of ownership—earnings and voting power spread over more shares.

-

Earnings‑per‑share (EPS) drop if profits do not rise proportionally with the new capital.

Key ratios influenced:

-

Debt‑to‑equity improves (equity numerator grows).

-

Return on equity (ROE) may fall initially if new equity is idle or yields lower returns than before.

-

Book value per share rises by the amount of proceeds ÷ new shares, provided shares are issued above book value.

5. Distinction from Related Financing Cash Flows

| Financing line | Cash direction | Typical impact on share count |

|---|---|---|

| Issuance of capital stock | Inflow | ↑ (dilutive) |

| Repurchase of capital stock (buyback) | Outflow | ↓ (anti‑dilutive) |

| Issuance of debt | Inflow | No effect |

| Repayment of debt | Outflow | No effect |

| Dividends paid | Outflow | No effect |

Understanding these distinctions helps analysts see whether a company is primarily funding itself via equity, debt, or internally generated cash, and how management balances dilution, leverage, and liquidity.

Take‑aways for Students and New Analysts

-

Issuance of capital stock = cash in, shares out. It boosts cash and equity simultaneously.

-

Look beyond the headline: Why is the firm raising equity now? Consider growth plans, leverage, industry conditions, and share price level.

-

Watch dilution versus return: More shares require higher earnings to keep per‑share metrics stable.

-

Trace the cash: Pair the financing inflow with where the cash goes (investing section for CapEx or acquisitions; operating losses; debt repayment). This reveals the company’s broader capital‑allocation story.

By tracking the “Issuance of capital stock” line, you gain insight into a firm’s funding strategy, its confidence in using equity markets, and the implications for existing and future shareholders.

Q · 01What is Issuance Of Capital Stock?+