A key financing cash flow figure representing the net cash impact of a company issuing new common stock and repurchasing its own shares during a period.

If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes.

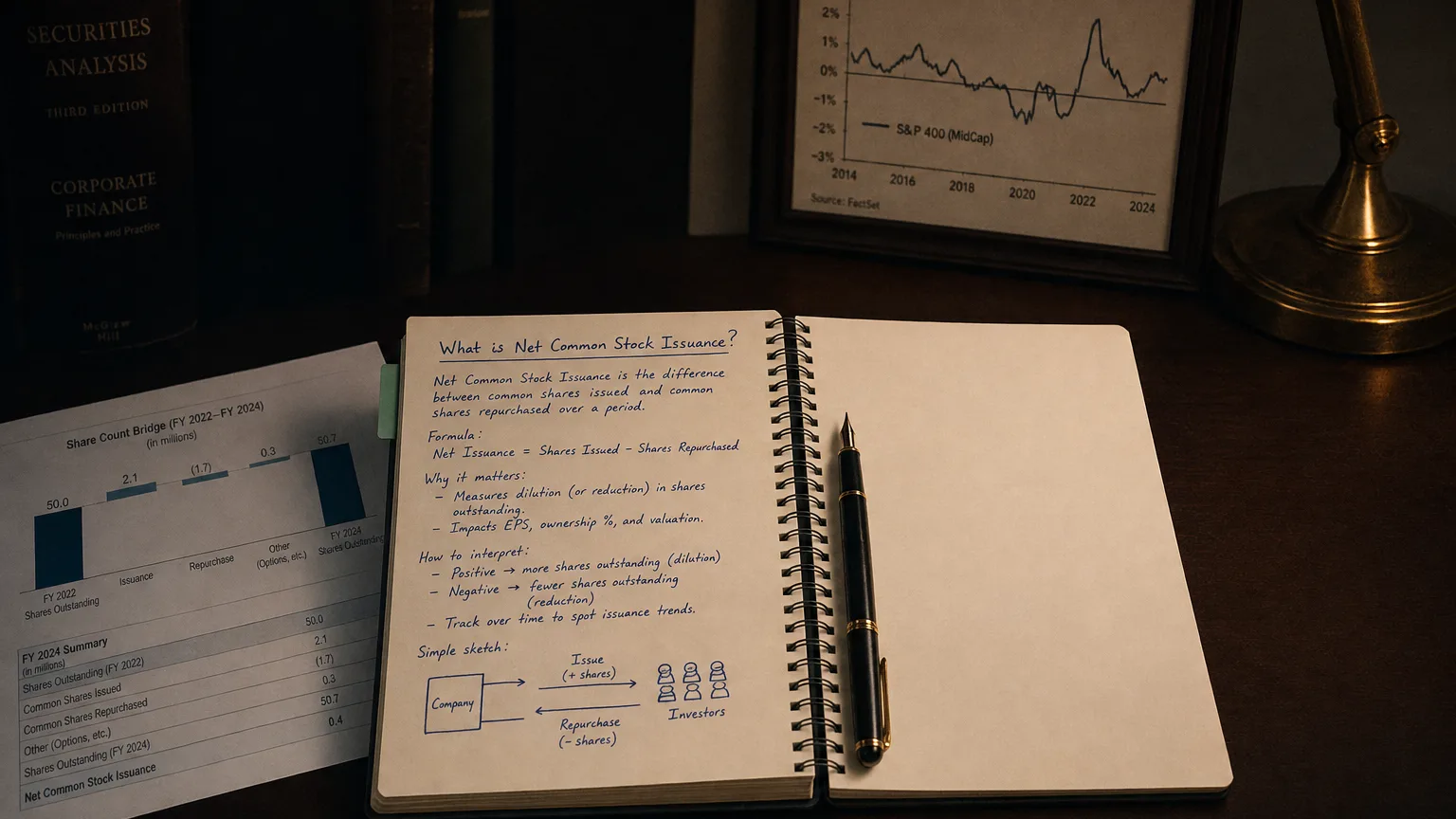

Net Common Stock Issuance refers to the net cash impact of transactions involving a company’s common stock during a period. In practical terms, it equals the total cash proceeds from issuing common shares minus the cash paid to repurchase common shares (buybacks). A positive net issuance means the company raised more cash from stock than it bought back, while a negative net issuance means the company spent more cash repurchasing shares than it issued. This line item is a key component of the financing section of the cash flow statement.

Calculation and Financial Statement Context

It is important to distinguish between gross and net figures. Gross issuance is the total cash a company receives from selling new shares. Gross repurchases is the total cash spent buying back shares. Net Common Stock Issuance simply nets these two opposing flows. While some financial statements show the gross inflow and outflow as separate lines, this ‘net’ figure provides a convenient summary of the overall direction of equity financing for the period.

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

Formula:

This line item deals exclusively with common stock. Any cash flows from issuing or redeeming preferred stock are typically reported separately. The term also directly relates to treasury stock, which are shares a company has repurchased. The cash used to buy these treasury shares is the negative component in the net issuance calculation.

The Strategic Decision: Why Issue vs. Why Repurchase?

The sign (positive or negative) of the net common stock issuance reveals a company’s capital strategy for the period.

Reasons Companies Issue Common Stock (Positive Net Issuance)

- To Fund Growth and Expansion: To raise permanent capital for R&D, new projects, or market expansion without the obligation of fixed repayments that come with debt.

- To Finance Acquisitions: To fund a major acquisition by issuing shares for cash or directly to the target company’s shareholders.

- To Strengthen the Balance Sheet: To raise cash to pay down debt (deleveraging) or to meet regulatory capital requirements, such as in the banking industry.

Reasons Companies Repurchase Common Stock (Negative Net Issuance)

- To Return Excess Cash: To distribute cash to shareholders as an alternative to dividends, especially if management believes the stock is undervalued.

- To Boost Per-Share Metrics: To reduce the number of shares outstanding, which mechanically increases Earnings Per Share (EPS) and can improve Return on Equity (ROE).

- To Offset Dilution: To counteract the dilutive effect of shares issued through employee stock compensation plans.

Implications for Cash Flow and Shareholders’ Equity

Net common stock issuance directly impacts both the cash position and the equity structure of a company.

Impact on Ownership

A positive net issuance increases the number of outstanding shares, which dilutes the ownership percentage and earnings claim of existing shareholders. A negative net issuance (net buyback) reduces the share count, concentrating ownership for the remaining shareholders.

A positive net issuance increases the company’s cash and total shareholders’ equity. Conversely, a negative net issuance decreases cash and total shareholders’ equity. Importantly, neither transaction directly affects the income statement, as they are considered financing decisions related to the company’s capital base, not its operational profitability.

GAAP vs. IFRS Reporting

Both U.S. GAAP and IFRS classify cash flows from issuing and repurchasing a company’s own equity as financing activities. There are no major conceptual differences. The primary variation may be in presentation. Some standards or companies prefer to show the gross inflows from issuance and gross outflows from repurchases as separate line items for maximum transparency. Others, or data aggregators, may present the single ‘Net Common Stock Issuance’ figure for simplicity. In either case, the underlying transactions and their impact on the total change in cash are the same.