is a financial concept covered in this article. After-Tax Earnings or Losses from Extraordinary Items (Historical Concept)

It does not matter how frequently something succeeds if failure is too costly to bear.

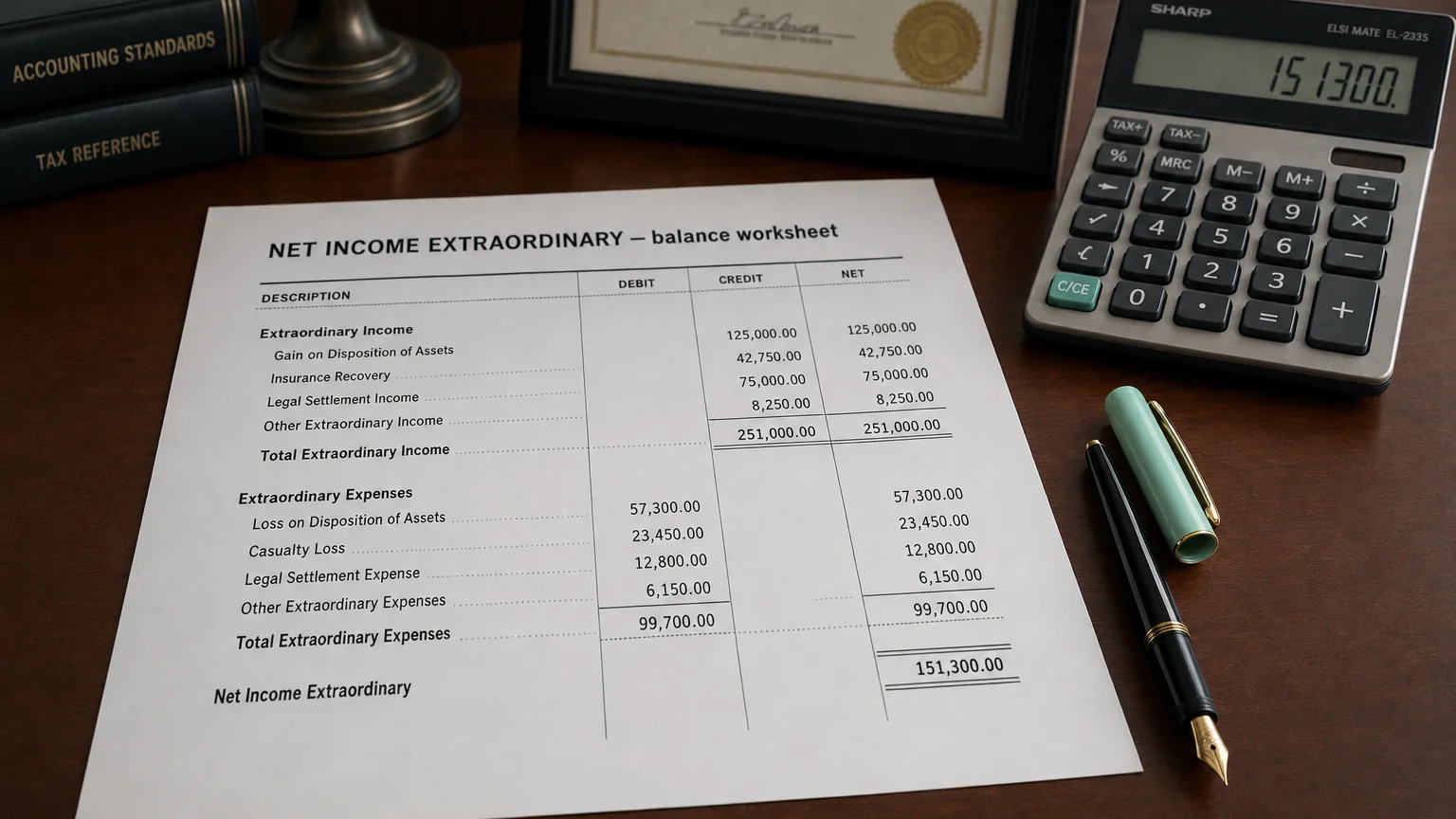

Net Income Extraordinary refers to the after-tax gains or losses arising from extraordinary items—events that were both unusual in nature and infrequent in occurrence. This line item captured the net impact of such rare events on the company’s bottom-line profitability. However, the classification of extraordinary items was officially eliminated from US GAAP in 2015 through ASU 2015-01, meaning this category no longer appears in modern financial statements. It remains relevant only for historical analysis of financial reports prior to 2015.

What Were Extraordinary Items?

Under pre-2015 US GAAP (APB Opinion 30), extraordinary items were strictly defined as events that were both unusual (abnormal and unrelated to ordinary business activities) and infrequent (not expected to recur in the foreseeable future).

Examples included major losses from natural disasters in areas not typically affected, government expropriation of assets, or one-time effects of significant new legislation. These items were reported separately, net of tax, to avoid distorting the company’s core operating performance.

Net Income Extraordinary was the after-tax amount of these rare events added to (or subtracted from) income from continuing and discontinued operations to arrive at total net income.

“It does not matter how frequently something succeeds if failure is too costly to bear.”

— Nassim Nicholas Taleb, Distinguished Professor of Risk Engineering, NYU Tandon School of Engineering Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets (2001)

Why Extraordinary Items Were Eliminated

The FASB removed the extraordinary items category in 2015 via ASU 2015-01 for several reasons:

Key Reasons

- Very few events met the strict dual criteria in practice.

- High subjectivity led to inconsistent classification across companies.

- Investors preferred detailed footnote disclosures over separate presentation.

- Simplification of financial reporting standards.

Post-2015, events previously qualifying as extraordinary are now included within income from continuing operations (often as unusual or infrequent items) with material events disclosed in footnotes.

IFRS never allowed a separate extraordinary items classification.

Historical Presentation and Calculation

In pre-2015 income statements:

Formula: Net Income = Income from Continuing Operations +/− Income/Loss from Discontinued Operations (net of tax) +/− Net Income Extraordinary (net of tax)

Extraordinary items were always shown net of tax, with the tax effect calculated separately.

Historical Examples

Example 1: Natural Disaster Loss

Major earthquake causes $300M pre-tax loss in a non-seismic region.

Tax benefit at 35%: 195M. This reduces total net income significantly.

Example 2: Expropriation Gain

Foreign government compensation exceeds book value, yielding $80M after-tax gain.

Net Income Extraordinary = +$80M. This boosts total net income.

Today, these would be reported in operating or non-operating income with footnote disclosure.

Relevance in Modern vs. Historical Analysis

In current financial statements (post-2015), this line is always zero. Similar events are embedded in continuing operations and often adjusted out in non-GAAP normalized net income.

For historical analysis (pre-2015 data):

- Explains large swings in total net income

- Should be excluded when assessing core or recurring profitability

- Aids in accurate trend and peer comparisons

Warning: Including historical extraordinary items in long-term earnings trends without adjustment can distort views of sustainable performance.

Q · 01What is Net Income Extraordinary?+