is a financial concept covered in this article. After-Tax Earnings or Losses from Discontinued Business Segments

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

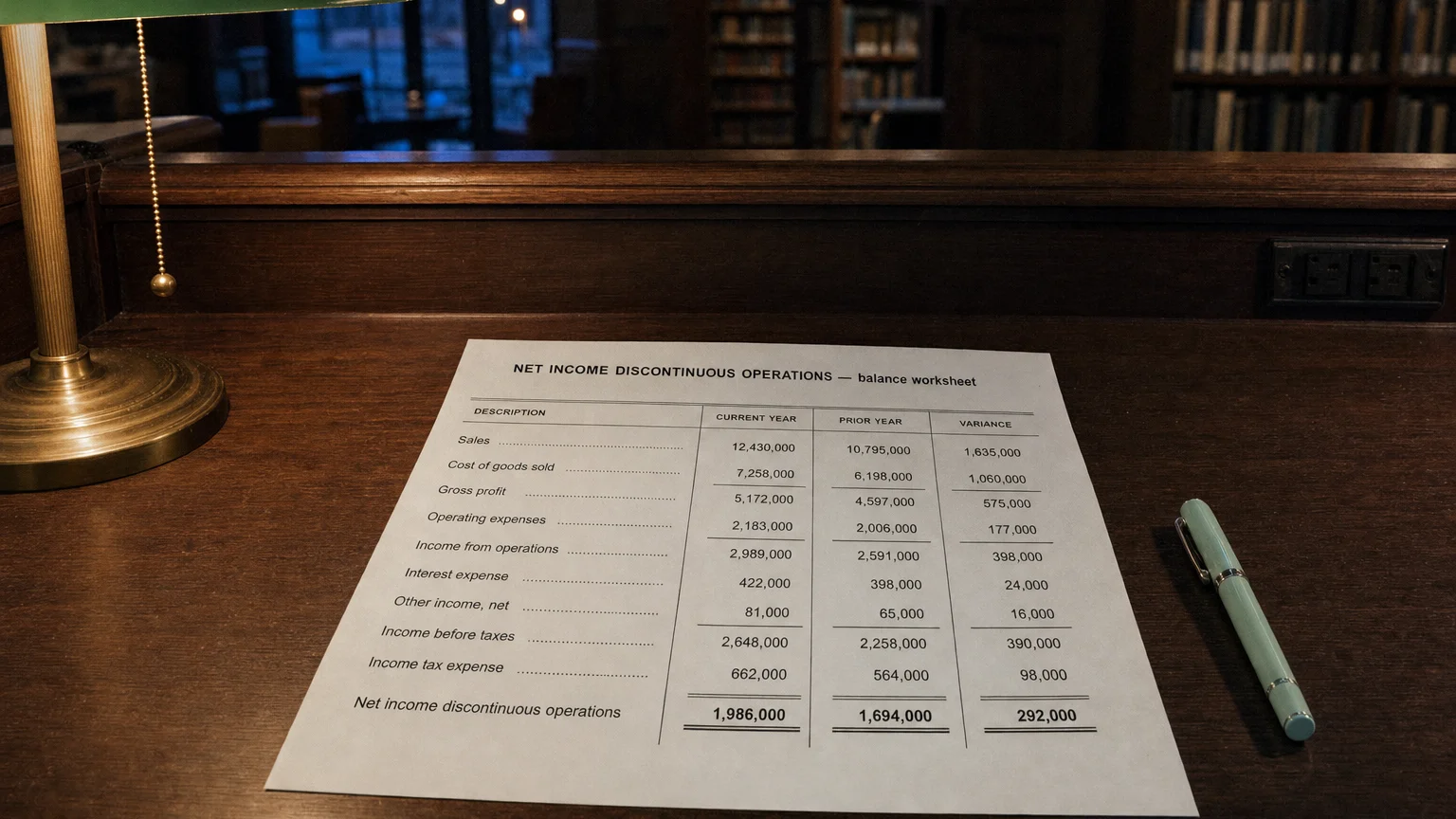

Net Income Discontinuous Operations (commonly referred to as Net Income from Discontinued Operations) represents the after-tax profit or loss generated by business components that a company has disposed of or classified as held-for-sale. These discontinued operations include operating results during the holding period, impairment charges, and any gain or loss on the actual disposal. This amount is reported separately, net of tax, to allow investors to focus on the performance of the company’s ongoing core businesses without the noise from exiting activities.

What is Net Income Discontinuous Operations?

Net Income Discontinuous Operations captures the after-tax financial impact of business segments or major lines of business that no longer form part of the company’s future operations. Under US GAAP (ASC 205-20) and IFRS (IFRS 5), these are components whose disposal represents a strategic shift with a major effect on operations and financial results.

The amount includes:

- Operating income or loss while the component was still owned

- Impairment losses when classified as held-for-sale

- Gain or loss on sale (proceeds minus carrying value) All presented net of applicable taxes and minority interests.

Separation ensures that core continuing operations reflect the sustainable ongoing business.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

How It Flows into Total Net Income

Standard income statement structure:

Formula: Total Net Income = Net Income from Continuing Operations +/− Net Income Discontinuous Operations +/− Other Special Items (historical)

This separate presentation prevents one-time divestiture effects from distorting trends in ongoing profitability.

Examples

Example 1: Profitable Divestiture

Company sells a non-core division.

Operating profit pre-sale: 500M; Book value: 150M. Tax on gain: 112.5M. Net Income Discontinuous Operations = 112.5M = +$152.5M.

Example 2: Costly Exit

Company shuts down an unprofitable factory.

Operating loss while held: −75M after-tax. Net Income Discontinuous Operations = −$100M.

Large positive values often accompany portfolio simplification; negative values reflect cleanup of legacy issues.

Importance in Financial Analysis

This metric is key for:

- Assessing core ongoing profitability (focus on continuing operations)

- Understanding strategic restructuring or portfolio changes

- Forecasting future earnings without transitory divestiture effects

Analysts typically exclude discontinuous operations when calculating normalized net income or forward estimates, as they are non-recurring by definition.

Warning: Frequent or large discontinuous operations may signal ongoing strategic challenges or poor past capital allocation.

Financial data providers clearly separate this amount to reconcile total net income with continuing performance.

Q · 01What is Net Income Discontinuous Operations?+