The Core Profit Attributable to Parent Company Shareholders After Minority Interests

You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.

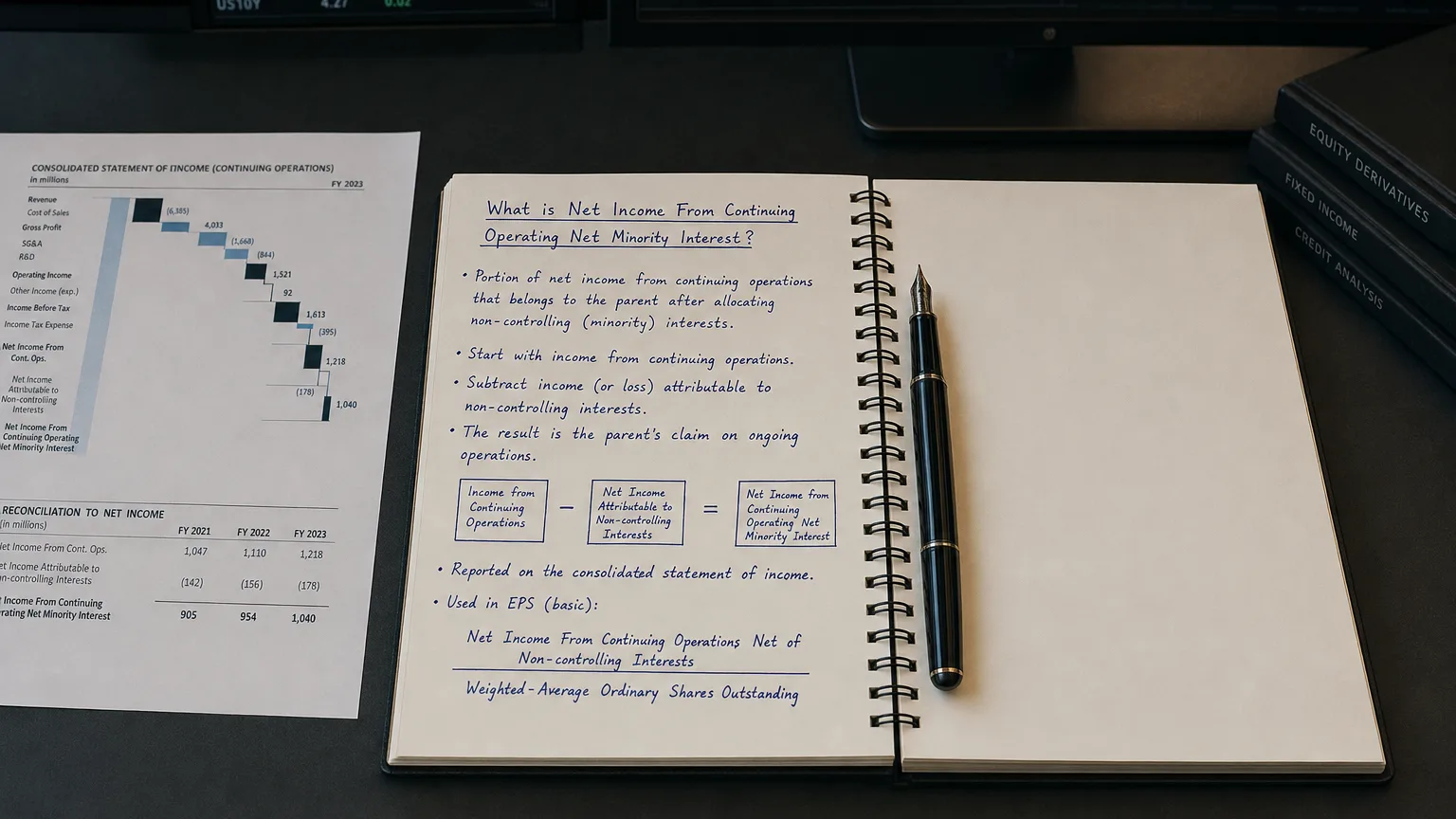

Net Income from Continuing Operations Net of Minority Interest (often abbreviated as Net Income from Continuing Operating Net Minority Interest in financial databases) represents the portion of profit generated from a company’s ongoing core business activities—after all operating expenses, taxes, and non-controlling (minority) interests—that is attributable to the parent company’s common shareholders. This metric excludes results from discontinued operations and provides a clean view of sustainable earnings power from continuing operations.

What is Net Income from Continuing Operations Net Minority Interest?

Net Income from Continuing Operations Net of Minority Interest is the bottom-line profit from a company’s regular, ongoing business activities after deducting all expenses, taxes, and the share of profits belonging to non-controlling (minority) shareholders in consolidated subsidiaries.

It excludes any gains or losses from discontinued operations or extraordinary items, making it a key measure of core operational performance. This figure is ultimately available to the parent company’s common shareholders and forms the primary basis for calculating earnings per share (EPS) from continuing operations.

This is one of the most important profitability metrics for investors because it reflects sustainable earnings from the businesses the company intends to operate long-term.

“You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

How It Fits in the Income Statement

The typical flow on a consolidated income statement is:

Income Statement Progression

- Net Income (total consolidated): Profit after all expenses and taxes, including minority interests.

- Minus: Minority Interests (non-controlling interests): Portion of subsidiary profits owned by outside shareholders.

- Equals: Net Income Attributable to Parent.

- Then, separate discontinued operations (net of tax and minority interest).

- Net Income from Continuing Operations Net Minority Interest = Total Net Income − Discontinued Operations − Minority Interests in Discontinued Ops (if any).

In many financial databases (e.g., Yahoo Finance, Bloomberg), this line is explicitly labeled to distinguish it from total net income.

Calculation Breakdown

Formula: Net Income from Continuing Ops Net Minority Interest = (Income from Continuing Operations before Tax − Tax Provision) − Minority Interest in Continuing Operations

Or, more comprehensively: Start with Pretax Income from Continuing Operations, subtract Tax Provision, then subtract Net Minority Interest related to continuing operations.

Minority interest deduction occurs after tax because minority shareholders share in the after-tax profits of the subsidiary.

Examples

Example 1: Company with Subsidiaries

Parent Co. owns 80% of Subsidiary A (20% minority interest).

Subsidiary A generates 500M. Minority share: 20% × 20M.

Net Income from Continuing Ops Net Minority Interest = 20M = 480M belongs entirely to Parent Co. shareholders.

Example 2: With Discontinued Operations

Total Consolidated Net Income: $600M

Includes 650M Minority Interest (all in continuing ops): $30M

Net Income from Continuing Ops Net Minority Interest = 30M = $620M

This metric helps investors ignore one-time divestiture impacts and focus on ongoing performance.

Importance in Financial Analysis

Analysts heavily rely on this figure because:

- It forms the starting point for normalized earnings calculations.

- It is used to compute EPS from continuing operations, a key valuation input.

- It enables better year-over-year comparisons by excluding discontinued segments.

- It reflects earnings truly available to common shareholders of the parent.

Growth in this metric is often seen as a sign of improving core business health, while declines may signal operational challenges.

Warning: Companies with complex structures and many partially-owned subsidiaries can have significant minority interest deductions—always check the magnitude relative to total profits.