is a financial concept covered in this article. The Share of Subsidiary Earnings Attributable to Non-Controlling Shareholders

No asset is so good that it can't become a bad investment if bought at too high a price. And there are few assets so bad that they can't be a good investment when bought cheap enough.

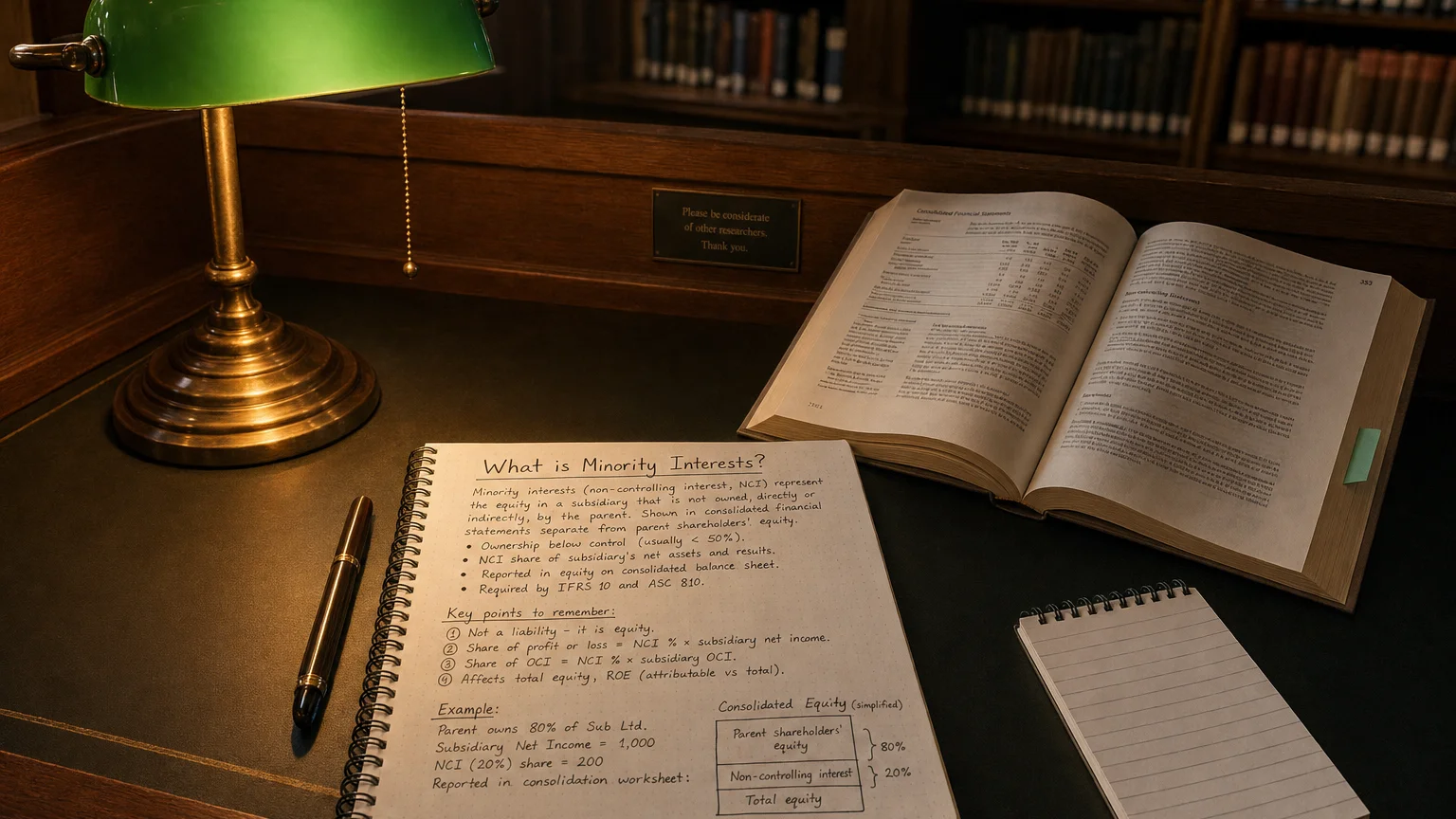

Minority Interests (also known as Non-Controlling Interests or NCI) represent the portion of a consolidated subsidiary’s net income (or loss) and equity that is owned by shareholders other than the parent company. When a company owns more than 50% but less than 100% of a subsidiary, the parent consolidates 100% of the subsidiary’s results but must allocate the portion belonging to outside owners as minority interests. This line item is deducted from consolidated net income to arrive at the earnings attributable to the parent’s shareholders, providing a clear view of the profits truly owned by the controlling entity.

What are Minority Interests?

Minority Interests arise in consolidated financial statements when the parent company controls (owns >50%) but does not fully own (100%) a subsidiary. Under US GAAP (ASC 810) and IFRS (IFRS 10), the parent must consolidate 100% of the subsidiary’s assets, liabilities, revenues, and expenses, even if ownership is only 60%.

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

The portion belonging to outside shareholders is recorded as minority interests (or non-controlling interests). On the income statement, this appears as a deduction after consolidated net income to show the amount attributable to the parent’s shareholders.

Since 2008 (SFAS 160/ASC 810), minority interests are presented in the equity section of the balance sheet, not as mezzanine or liability.

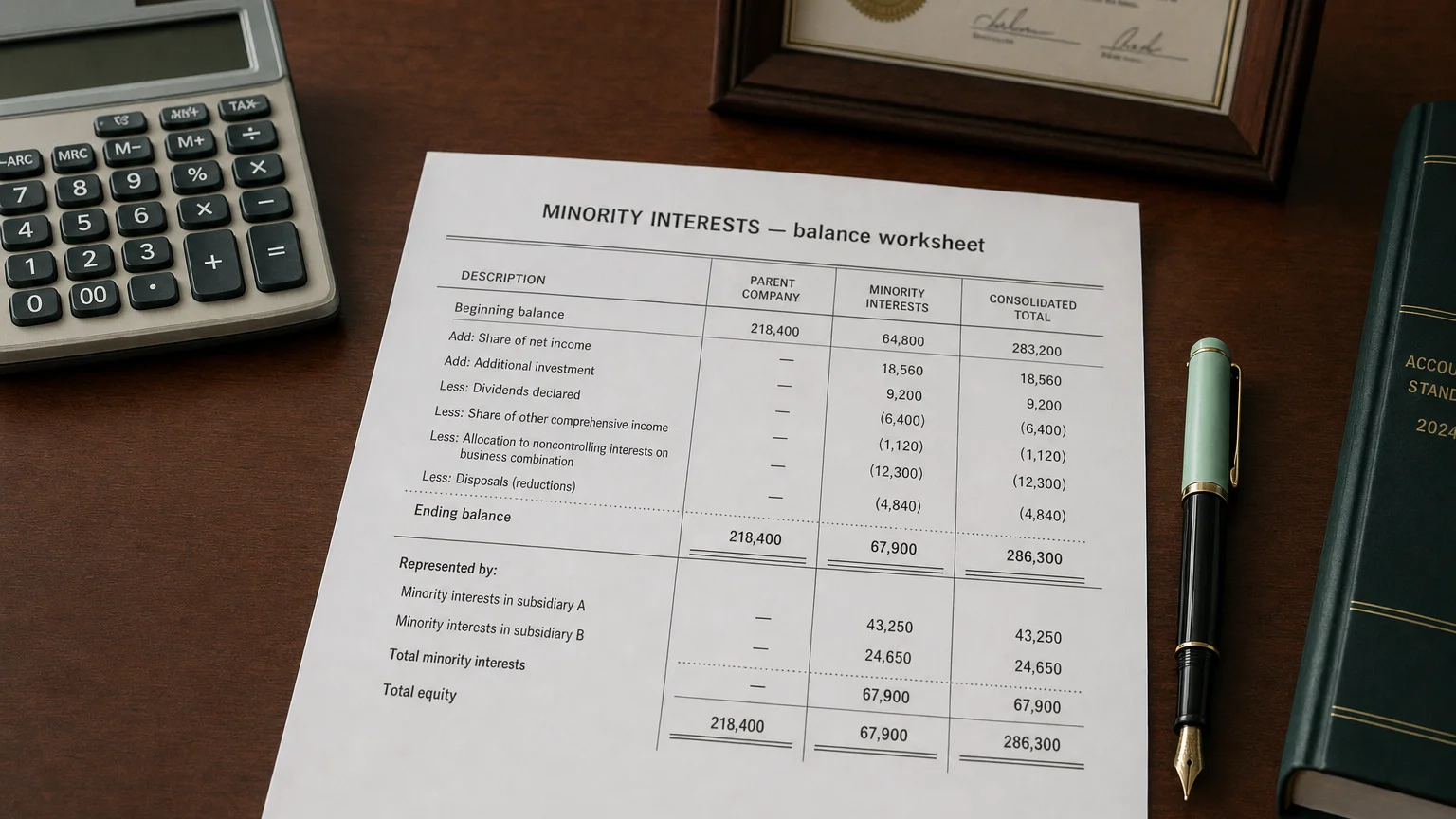

How Minority Interests Appear in Financial Statements

Income Statement flow:

Consolidated Net Income Attribution

- Consolidated Net Income (100% of parent + subsidiaries)

- − Minority Interests (share of subsidiary net income owned by outsiders)

- = Net Income Attributable to Parent Company

Balance Sheet: Minority interests are shown as a separate component of shareholders’ equity.

Minority interests can be positive (deduction when subsidiary profitable) or negative (addition when subsidiary loss-making).

Calculation of Minority Interests

Formula: Minority Interests in Net Income = (Subsidiary Net Income) × (1 − Parent Ownership Percentage)

If multiple partially-owned subsidiaries exist, the total minority interest is the sum across all.

Examples

Example 1: Profitable Subsidiary

Parent owns 80% of Subsidiary A.

Subsidiary A net income: 100M × 20% = 500M (includes full 500M − 480M.

Example 2: Loss-Making Subsidiary

Parent owns 70% of Subsidiary B.

Subsidiary B net loss: −50M × 30% = −$15M (negative deduction = addition). This increases parent’s attributable income by absorbing part of the loss.

Loss allocation to minority interests can make parent earnings appear stronger than economic reality.

Importance in Financial Analysis

Analysts examine minority interests to:

- Assess true earnings owned by parent shareholders

- Evaluate consolidation strategy and acquisition structures

- Understand leverage from partial ownership

High minority interests relative to consolidated income may indicate significant outside ownership in key subsidiaries, potentially affecting control or future buyout costs.

Warning: Negative minority interests (from losses) can inflate parent earnings—adjust for economic ownership in valuation models.

Q · 01What is Minority Interests?+