is a financial concept covered in this article. The Earnings Benefit Derived from Utilizing Prior-Year Net Operating Losses

You can't take the same actions as everyone else and expect to outperform.

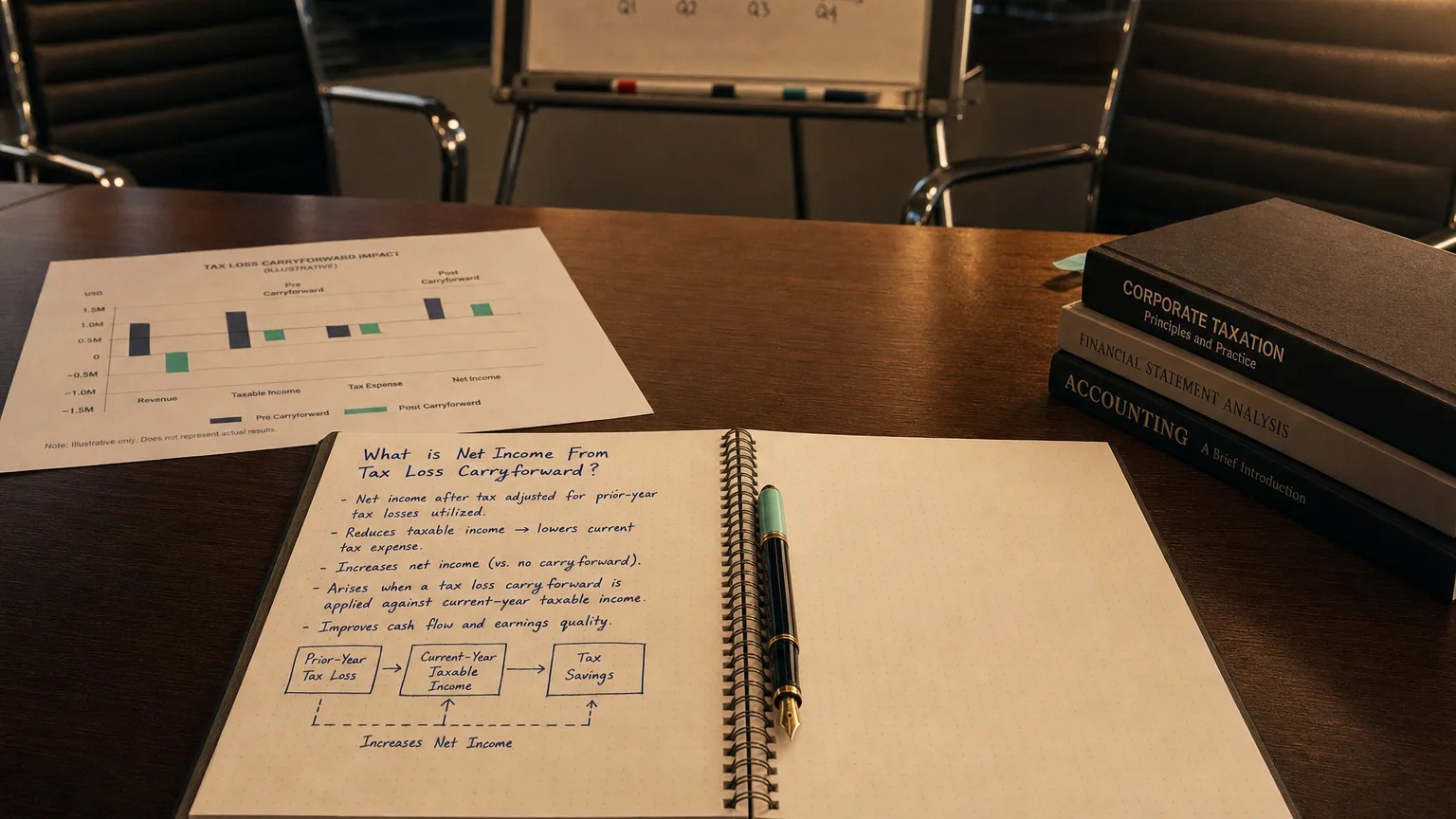

Net Income From Tax Loss Carryforward represents the positive impact on a company’s reported net income resulting from the utilization of net operating loss (NOL) carryforwards to offset current-period taxable income. These carryforwards are accumulated losses from previous years that reduce the current tax liability, effectively increasing after-tax earnings. This line item isolates the ‘tax savings’ contribution to net income, highlighting how historical losses provide a valuable tax shield during profitable periods, particularly for companies recovering from prior downturns.

What is Net Income From Tax Loss Carryforward?

Net Income From Tax Loss Carryforward is the amount by which reported net income is higher due to the reduction in tax expense from applying net operating loss (NOL) carryforwards. NOLs originate from years when tax deductions exceeded taxable income, creating a deferred tax asset that can offset future profits.

When utilized, the tax provision decreases by the amount of NOL applied times the applicable tax rate, directly boosting net income. This line item in detailed income statements separates this non-operating tax benefit from core operational earnings.

Common in turnaround stories, post-recession recoveries, or growth companies reaching profitability after early losses.

“You can’t take the same actions as everyone else and expect to outperform.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘Dare to Be Great’ (2006)

How It Is Generated

The benefit flows through the tax provision:

Formula: Net Income From Tax Loss Carryforward = (NOL Utilized × Applicable Tax Rate)

This amount reduces the tax provision (or creates a tax benefit), increasing net income. Under current US rules (post-TCJA 2017):

- Post-2017 NOLs carry forward indefinitely.

- Limited to offsetting 80% of taxable income annually.

Key Constraints

- 80% limitation on taxable income offset

- Section 382 restrictions after significant ownership changes

- Valuation allowances if realization is doubtful (no income benefit)

Tip: Tax footnotes detail available NOLs, utilization, and remaining balances.

Examples

Example 1: Partial Offset

Pre-tax Income: $300M

NOL Available: 240M Tax Rate: 21% Tax Benefit = 50.4M Net Income From Tax Loss Carryforward = +$50.4M Without NOL, tax expense would be higher by this amount.

Example 2: Full Allowed Utilization

Pre-tax Income: $100M

NOL Available: 80M (80% limit) Tax Benefit = 16.8M Net Income From Tax Loss Carryforward = +$16.8M Effective tax rate drops significantly.

This benefit is essentially ‘free’ earnings from past losses, but finite.

Importance in Financial Analysis

This metric reveals:

- Temporary earnings enhancement from tax attributes

- ‘Tax runway’ remaining before normalization

- Potential future tax rate increases as NOLs deplete

Analysts often exclude this benefit when calculating normalized net income or cash taxes paid, focusing on sustainable post-tax earnings at statutory rates.

Warning: High reliance on NOL benefits can overstate ongoing profitability—model the ‘tax cliff’ when carryforwards expire or are fully used.

Critical for valuing turnaround companies or those with large deferred tax assets.