Pretax Income is a financial concept covered in this article. A Measure of Company Profitability Before Taxes

Survival comes first, truth, understanding, and science later.

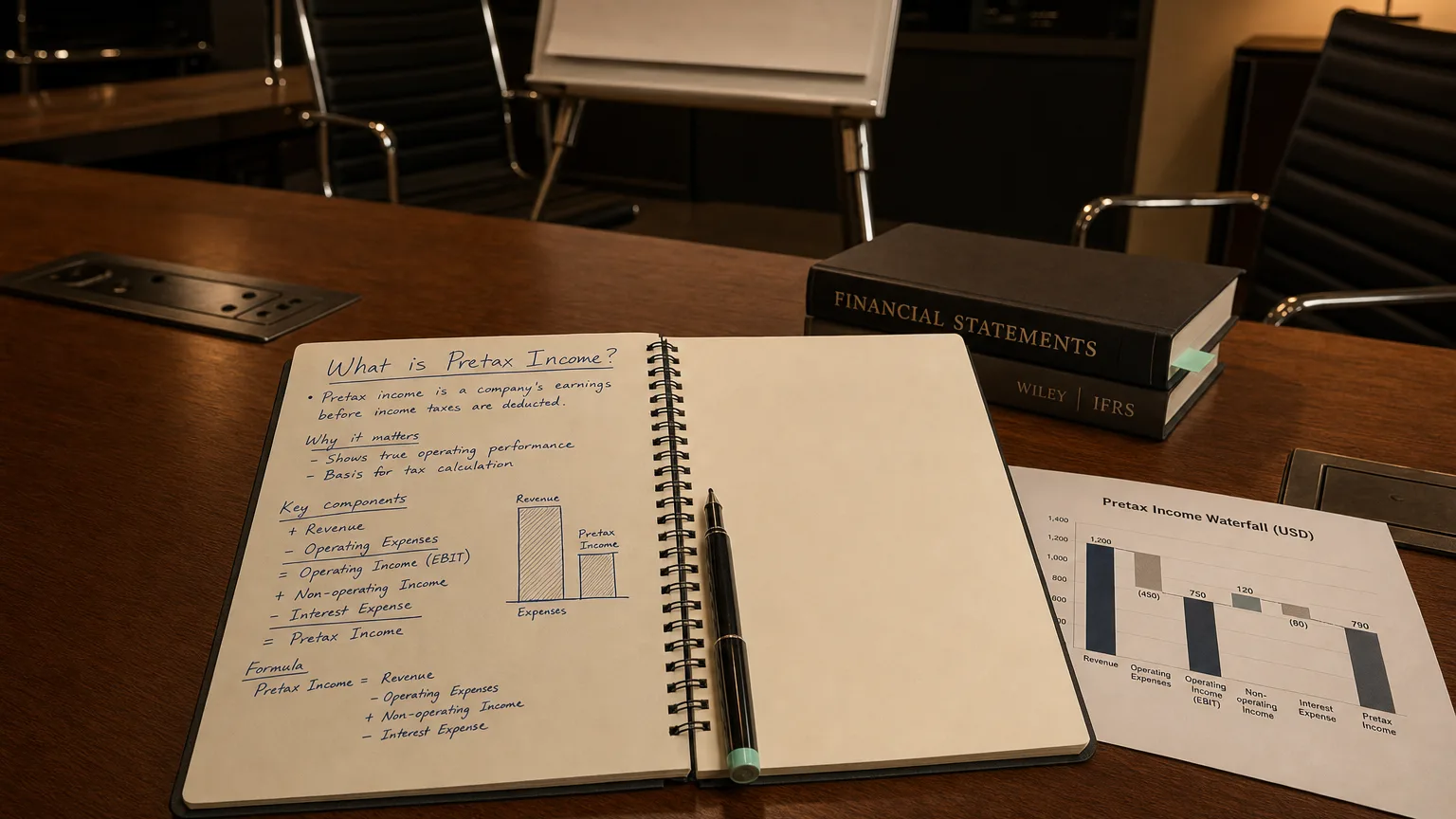

Pretax income (also called earnings before tax (EBT) or profit before tax) is the profit a company generates before accounting for income taxes. In other words, it’s the net income before the tax expense is deducted. This figure appears on a company’s income statement, typically as a subtotal labeled “Income Before Taxes” or “Earnings Before Tax”, right before the line where income tax is subtracted and net income is reported. Pretax income already takes into account all the business’s expenses except for taxes – it includes the impact of operating costs, interest on debt, and other expenses that have been incurred during the period.

How Pretax Income Is Calculated

In simple terms, pretax income is calculated as total revenues minus all expenses except income taxes. You start with the money the company earned from its sales or services, and then subtract every cost of running the business (except taxes). Mathematically, one way to express this is:

Pretax Income = Revenue – (Cost of Goods Sold + Operating Expenses + Interest Expense) + Other Income

This means pretax income includes the effects of all typical expenses like the cost of goods, salaries, rent, depreciation, and interest on loans, while adding in any extra income the company earned (for example, interest income). Another way to compute it is to take the operating profit (often called EBIT – Earnings Before Interest and Taxes) and then subtract interest payments and add any interest income to get pretax profit. (Alternatively, if you already know the net income after taxes, you can work backwards: Pretax Income = Net Income + Income Tax Expense.)

Key Components Affecting Pretax Income

Several line items on the income statement contribute to the pretax income figure:

-

Revenue: This is the total sales or income generated by the company. It’s the starting point – higher revenue increases pretax profit (all else being equal). Everything else will be subtracted from this amount.

-

Cost of Goods Sold (COGS): If the company sells products, COGS represents the direct costs of producing those goods (materials, manufacturing labor, etc.). COGS is subtracted from revenue to find gross profit, so higher COGS will lower gross profit and, consequently, reduce pretax income.

-

Operating Expenses: These include the day-to-day expenses of running the business (for example, salaries, rent, utilities, marketing costs, and depreciation of equipment). All operating expenses are deducted from gross profit, reducing the company’s operating income. Because pretax income is calculated after subtracting operating costs, an increase in operating expenses will decrease pretax income. (Depreciation and amortization, while non-cash expenses, are still counted as expenses in the income statement and therefore also reduce pretax profit.)

-

Interest Expense: If the company has debt, the interest it pays on loans or bonds is an expense that comes out after operating profit. Interest expense is subtracted when calculating pretax income, which lowers the pretax profit. For instance, a large interest expense from heavy borrowing will drag pretax income down.

-

Interest Income (and Other Non-Operating Income): Conversely, if the company earned interest on investments or had other non-operating income (say, profit from selling an asset), that income is added in before taxes. Such income increases pretax profit. In many income statements, interest income and interest expense are combined into a single net figure; regardless, any net positive interest or other income will boost pretax income, while net interest costs will reduce it.

After accounting for all the above items, what you have left is pretax income. No tax has been applied to this figure yet – it’s the profit “before tax”. The next step (below pretax income on the income statement) would be to subtract the income tax expense, resulting in the final net income (the company’s profit after taxes).

Example: Calculating Pretax Income

To illustrate, consider a simple income statement for a hypothetical company:

-

Total Revenue: $1,000,000

-

Cost of Goods Sold: $400,000

-

Gross Profit: $600,000 (Revenue minus COGS)

-

Operating Expenses (e.g. salaries, rent, utilities, depreciation): $300,000

-

Operating Profit (EBIT): $300,000 (Gross Profit minus Operating Expenses)

-

Interest Expense: $50,000 (interest paid on the company’s debt)

-

Interest Income: $10,000 (interest earned from a bank account or investments)

Using these numbers, we calculate the pretax income step by step. Starting with $300,000 of operating profit, we subtract the $50,000 interest expense (a cost) and add the $10,000 interest income. This gives:

Pretax Income: $260,000 (profit before any taxes are applied)

If the company’s income tax rate is, say, 30%, it would then record an income tax expense of $78,000 (which is 30% of $260,000) on the income statement. After subtracting that tax, the net income would be $182,000. In summary, the pretax income of $260,000 represents the profit earned from all operations and financial activities before the government takes its share in taxes.

Why Pretax Income Is Important in Financial Analysis

Pretax income is a key metric that analysts and investors examine for several reasons:

-

Isolating Operational Performance: By looking at profit before taxes, one can see how well the company’s core business (plus any financing costs) is performing without the influence of tax effects. Taxes can fluctuate due to changes in tax laws or one-time tax credits, so pretax earnings give insight into the company’s true financial performance before those external factors come into play. In other words, it shows the underlying profitability from operations and interest costs, prior to any reduction for taxes.

-

Comparability Across Companies and Periods: Pretax income allows for apple-to-apple comparisons between companies that might have different tax rates or between different years for the same company. Tax expenses can vary widely by country, state, industry, or year (due to changing tax rates or special tax breaks). By comparing pretax incomes, analysts can evaluate which company is actually more efficient or profitable from a business standpoint, without tax differences clouding the picture. This makes peer comparisons and trend analysis more fair and “bias-free,” since one company’s higher net income might simply be due to a lower tax rate rather than better operations.

-

Assessing Tax Impact and Efficiency: Pretax income is the figure upon which taxes are calculated, so it’s used to derive metrics like the company’s effective tax rate (tax expense divided by pretax profit). By examining pretax vs. after-tax profits, stakeholders can see how much of the company’s earnings are absorbed by taxes. For example, if a company’s pretax profit is significantly high but net income is much lower, it indicates a heavy tax burden. Pretax profit margin (pretax income divided by revenue) is sometimes calculated to judge profitability ignoring taxes – this margin will naturally be higher than the net profit margin because it excludes tax costs. Comparing the pretax margin to the net margin can highlight the impact of taxes on the company’s results.

-

Better Indicator in Certain Cases: In some cases, pretax income is viewed as a more reliable indicator of a company’s performance than net income. Companies with unusual tax situations – for instance, large tax credits, loss carryforwards, or other tax incentives – might show a distorted net income (either unusually high or low) relative to their actual operating performance. By looking at pretax income, analysts can evaluate performance without those tax distortions. In other words, pretax profit shows what the company earned from its business activities before the influence of tax accounting, giving a clearer picture of operational success.

In summary, pretax income is an important subtotal on the income statement that represents a company’s profit before taxes. It is calculated by subtracting all expenses except taxes from revenue, incorporating costs like COGS, operating expenses, and interest. This metric is crucial for understanding a company’s financial health because it provides insight into performance without tax effects, serves as the basis for tax calculations, and enables more meaningful comparisons of profitability across different companies or periods. Analysts often examine pretax income to discern how effectively a business is operating and how significantly taxes are impacting the bottom line.

Sources:

-

Corporate Finance Institute – Pretax Income Definition & Formula

-

Investopedia – Profit Before Tax (Pretax Profit) Explanation

-

Corporate Finance Institute – EBT vs. Pretax Income Overview