The Per-Share Earnings Boost from Utilizing Prior Net Operating Losses on a Basic Share Basis

Our favorite holding period is forever.

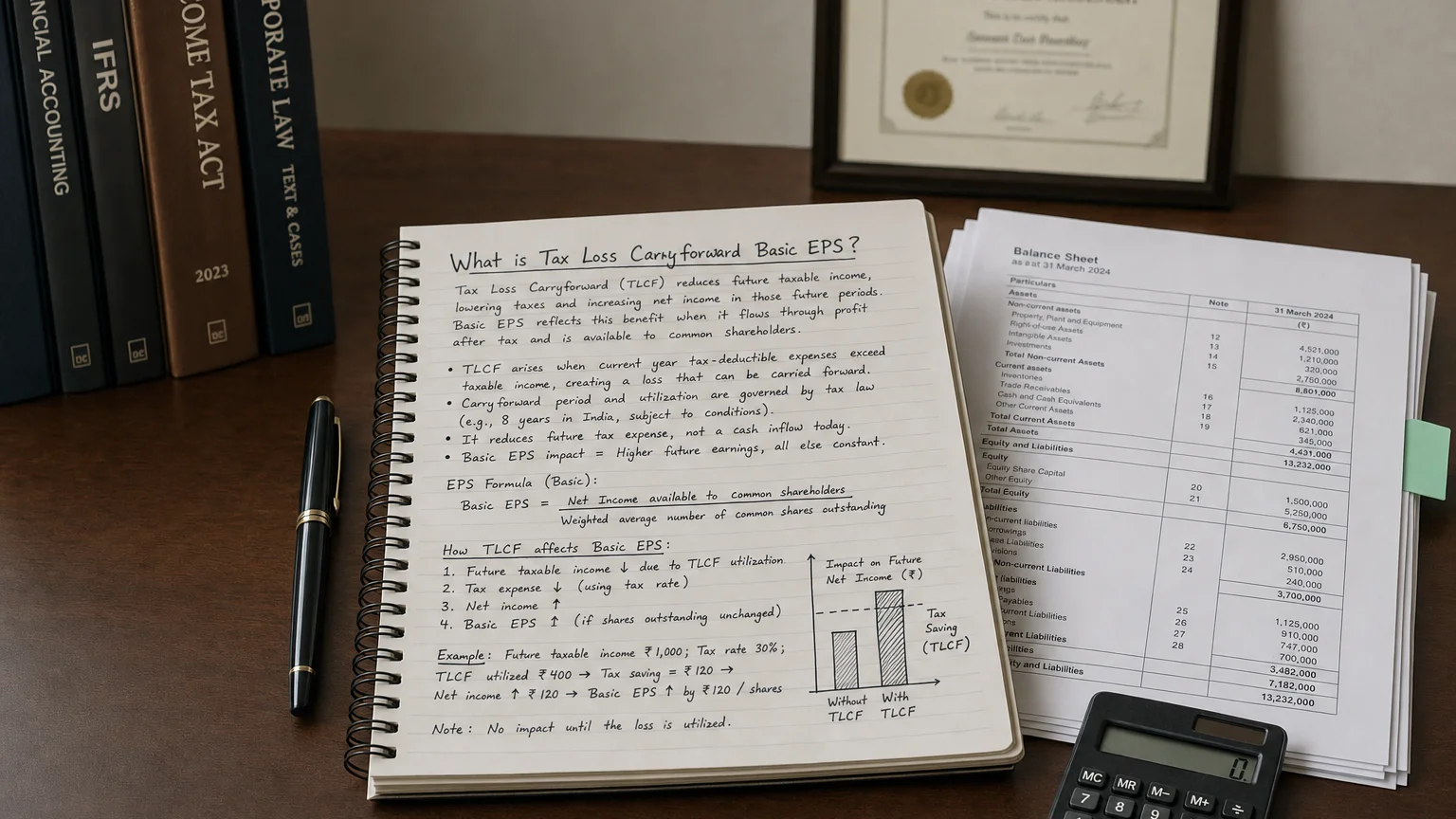

A tax loss carryforward (also called a net operating loss or NOL carryforward) is a tax provision that allows a company to use a current period’s losses to reduce taxable income in future periods. In other words, if a company incurs a tax-deductible loss in one year, it can carry forward that loss to offset taxable profits in later years, thereby reducing future tax bills. This concept creates a deferred tax benefit: the company has a future tax saving (recorded as a deferred tax asset on the balance sheet) because it can apply past losses against future taxable income. Under U.S. GAAP, these past losses are referred to as Net Operating Losses (NOLs), whereas in some other jurisdictions (e.g. Canada) they may be explicitly called tax loss carryforwards. The key point is that a tax loss carryforward represents a potential future tax deduction, which can translate into lower tax expense in profitable years.

Basic EPS in Financial Reporting

Basic Earnings Per Share (EPS) is a standard financial metric that measures the net income available to common shareholders for each share of stock. It is calculated by dividing the company’s net income (after subtracting any preferred dividends) by the weighted-average number of common shares outstanding during the period. Basic EPS is presented on the income statement for each period (for example, on a company’s annual or quarterly income statement, you’ll often see “Basic EPS” reported as a dollar amount). Importantly, Basic EPS reflects all components of net income – it doesn’t adjust for any specific sources of income or expense unless those are reported separately as discontinued operations or other special categories. Under both U.S. GAAP and IFRS, companies must present EPS for profit from continuing operations (if applicable) and for total net profit or loss, using the standardized calculation above.

Is “Tax Loss Carryforward Basic EPS” a Standard Term?

The term “Tax Loss Carry Forward Basic EPS” is not a standard financial reporting term defined by GAAP or IFRS. In authoritative accounting literature on EPS (e.g. ASC 260 in U.S. GAAP or IAS 33 in IFRS), there is no separate EPS metric specifically tied to tax loss carryforwards – only Basic EPS and Diluted EPS (and EPS from continuing or discontinued operations when required) are defined. Therefore, seeing “Tax Loss Carryforward Basic EPS” likely indicates a company-specific or analytical presentation, not a GAAP/IFRS mandated figure. For instance, a company or data provider might use this phrasing to highlight the effect of tax loss carryforwards on EPS (perhaps by showing an adjusted EPS figure excluding or focusing on the tax loss benefit). In practice, companies sometimes present non-GAAP or adjusted EPS metrics excluding unusual items (for example, excluding one-time tax benefits from NOL carryforwards) to give a sense of “underlying” performance. These adjusted figures are management-defined and must be clearly labeled and reconciled to GAAP EPS. In summary, “Tax Loss Carryforward Basic EPS” is not an official line item – it likely refers to EPS in the context of tax loss carryforwards, a disclosure or analysis rather than a standard term.

How Tax Loss Carryforwards Affect Net Income and EPS

Tax loss carryforwards can directly impact net income and thus Basic EPS through their effect on income tax expense. When a company has carryforward losses available and earns positive pre-tax income, it can use those losses to offset some or all of its taxable income. The immediate result is a lower income tax expense (potentially zero tax if the carryforward fully covers the taxable profit) for that period. A lower tax expense means higher net income all else equal, since net income = pre-tax income – tax expense. In essence, the carryforward provides a tax benefit that boosts after-tax earnings.

Under U.S. GAAP, the accounting rules ensure that the benefit of NOL carryforwards appears in the normal tax line of the income statement (within continuing operations). Specifically, any tax benefit from utilizing a loss carryforward is allocated first to reduce the income tax expense from continuing operations down to zero, and only if there’s more benefit beyond that would it be allocated to other categories (such as discontinued operations, etc.). This means that using a carryforward is reflected as a reduction of tax expense (or even a tax benefit if the carryforward causes a negative tax expense), which in turn increases net income for the period. As a result, Basic EPS will rise, since the numerator of the EPS calculation (net income available to common shareholders) is higher than it would have been without the tax loss carryforward. Put simply, reducing taxes increases earnings per share, because taxes are one of the largest costs for a company and any reduction in tax directly raises profit.

To illustrate the impact, consider a simple example of the same company in two scenarios: one with no carryforwards and one with a tax loss carryforward available:

-

Without a carryforward: Suppose the company has $100 of pre-tax profit and a 30% tax rate. It would incur $30 in income tax expense, leaving $70 in net income. If there are 100 common shares, Basic EPS would be $0.70 (calculated as $70 net income / 100 shares).

-

With a carryforward: Now suppose the company still has $100 pre-tax profit but also has sufficient tax loss carryforwards to offset that income. It could apply the NOL and owe no current taxes on that profit (tax expense reduced to $0 thanks to the carryforward). Net income would then be the full $100 (because the $30 tax was avoided). With 100 shares, Basic EPS in this case is $1.00 per share. This $0.30 per share improvement in EPS is directly due to the tax loss carryforward eliminating what would have been a tax expense.

In reality, the effect might be less dramatic if only a portion of the taxable income is sheltered by carryforwards, but the direction is the same: using carryforwards lowers tax expense and raises after-tax earnings, thereby increasing EPS relative to a scenario with no such tax benefit.

It’s worth noting that the timing of when the tax benefit is recognized can matter. If a company’s deferred tax asset for the loss was already recorded in a prior period (because management expected to use the loss), then the benefit may have been reflected earlier. In that case, when the carryforward is actually used to offset taxes, the company will also reduce its deferred tax asset (recording a deferred tax expense) – effectively, the saved current tax and the deferred tax expense offset each other in the income statement. No additional net income arises at the time of use because the benefit was recognized back when the loss occurred. On the other hand, if a company had not recorded any deferred tax asset (perhaps due to uncertainty about future profits), then when it finally utilizes the carryforward or decides it is realizable, it will recognize the tax benefit in the current period’s income. This can lead to a one-time jump in net income (a tax benefit appearing on the income statement), thus boosting EPS in that period. In either situation, however, the total economic benefit of the tax loss carryforward (reducing taxes paid) ultimately flows through to shareholders via higher cumulative earnings.

GAAP and IFRS Considerations

Both U.S. GAAP and IFRS recognize the effect of tax loss carryforwards in the financial statements, but they have specific criteria for doing so. A tax loss carryforward gives rise to a deferred tax asset (DTA), since it represents future tax savings. Under U.S. GAAP (ASC 740), a company records a DTA for an NOL carryforward only if it’s more likely than not (greater than 50% probability) that the benefit will be realized through future taxable income. If there is significant doubt (e.g. the company might not generate enough profits before the carryforward expires), GAAP requires a valuation allowance to reduce the DTA to the amount expected to be usable. Any increase or release of this valuation allowance flows through income tax expense (for example, releasing a valuation allowance produces a tax benefit in the income statement, increasing net income). IFRS (IAS 12) uses a similar concept: a deferred tax asset for tax loss carryforwards is recognized only to the extent it is probable that future taxable profits will be available to utilize the losses. IFRS does not use a separate “valuation allowance” account – instead it simply doesn’t recognize a DTA beyond the probable recoverable amount – but the underlying principle is comparable. In short, both GAAP and IFRS ensure that tax loss carryforwards affect the income statement only once it’s likely the tax benefit will be realized (either by earlier recognition of a DTA or by waiting until taxable income arises). This means that companies cannot inflate earnings with dubious future tax benefits; the effects are recognized under consistent, prudent criteria.

Presentation-wise, tax loss carryforward benefits are included in the normal income tax line on the income statement under both GAAP and IFRS. Neither framework treats the use of a carryforward as an extraordinary item or a special credit outside of ordinary profit. In the past, U.S. GAAP had a concept of extraordinary items (for unusual, infrequent events), but even then, guidance stated that the tax benefit of an operating loss carryforward should be allocated to the source of income in the year it’s used – generally meaning it reduces the tax expense of continuing operations. Today, with extraordinary items eliminated, any tax relief from NOLs simply reduces income tax expense on the income statement, increasing the profit from continuing operations. IFRS follows an “intraperiod tax allocation” approach as well, where tax is allocated to continuing operations, discontinued operations, or OCI as appropriate. However, a tax loss carryforward used against normal operating profits will just show up as a lower tax charge in profit or loss. The result under both standards is that Basic EPS automatically reflects the benefit – since Basic EPS uses the bottom-line profit (or profit from continuing operations, if presented) as the numerator, it inherently includes any tax savings from NOL carryforwards.

Example Scenario and EPS Impact

Consider a company that in prior years had significant losses, but now has returned to profitability, carrying forward those past losses. In its first profitable year, it might pay little to no income tax because the previous losses offset its taxable income. For example, BioTech Co. earns $50 million in pre-tax income in 2025 but has ample loss carryforwards from earlier years. Its statutory tax rate is, say, 25%, so normally it would incur about $12.5 million in taxes. Thanks to the carryforwards, however, its actual tax expense is nearly zero (it uses the losses to wipe out most of its taxable income). This yields a much higher net income than expected – nearly $50 million instead of $37.5 million – and Basic EPS is correspondingly higher. Investors and analysts will notice that a portion of the earnings is coming from this tax break rather than core operations. Companies in this situation often explain the effect in their earnings disclosures. They might say, for instance, “Net income includes a $12.5 million ($0.05 per share) tax benefit from utilization of net operating loss carryforwards.” This is a way to communicate that EPS was boosted by a one-time tax factor. Indeed, such disclosure is purely informational; under GAAP/IFRS the official Basic EPS figure includes that benefit.

It’s also possible to imagine the inverse scenario: if a company had recorded all its loss benefits upfront (as deferred tax assets in the loss years), then its future EPS would not get an extra boost when those losses are used – because the benefit was already taken into account earlier. The key takeaway is that tax loss carryforwards shield income from taxes, and shielding income from taxes will either increase current period earnings or will have increased past earnings (depending on when the benefit is recognized). Either way, shareholders benefit through higher cumulative EPS than they would have without the ability to carry losses forward.

Summary

Tax loss carryforwards are a tax accounting mechanism that can enhance a company’s net income by reducing tax expense, thereby increasing Basic EPS. They are not a separate type of EPS; rather, their effect is embedded in the normal EPS calculation through the income tax line on the income statement. The term “Tax Loss Carryforward Basic EPS” isn’t an official GAAP or IFRS term, but likely refers to an EPS figure influenced by loss carryforwards or a management-adjusted metric highlighting the impact of those carryforwards. Under the accounting standards, any tax benefit from NOL carryforwards will be reflected in higher profits (assuming the company is confident it can use the losses, per GAAP/IFRS recognition rules). Basic EPS, being simply net income divided by shares, will naturally rise if net income includes tax savings from prior losses. Investors should understand that while carryforwards don’t improve pre-tax operating performance, they do affect after-tax earnings and EPS, sometimes materially. In financial analysis, one may look at EPS both with and without such tax benefits to gauge underlying performance, but only the inclusive figure is Basic EPS as defined by accounting standards.