is a financial concept covered in this article. A Clean Measure of Core Earnings Per Share Excluding Non-Recurring Items

I don't want a lot of good investments; I want a few outstanding ones.

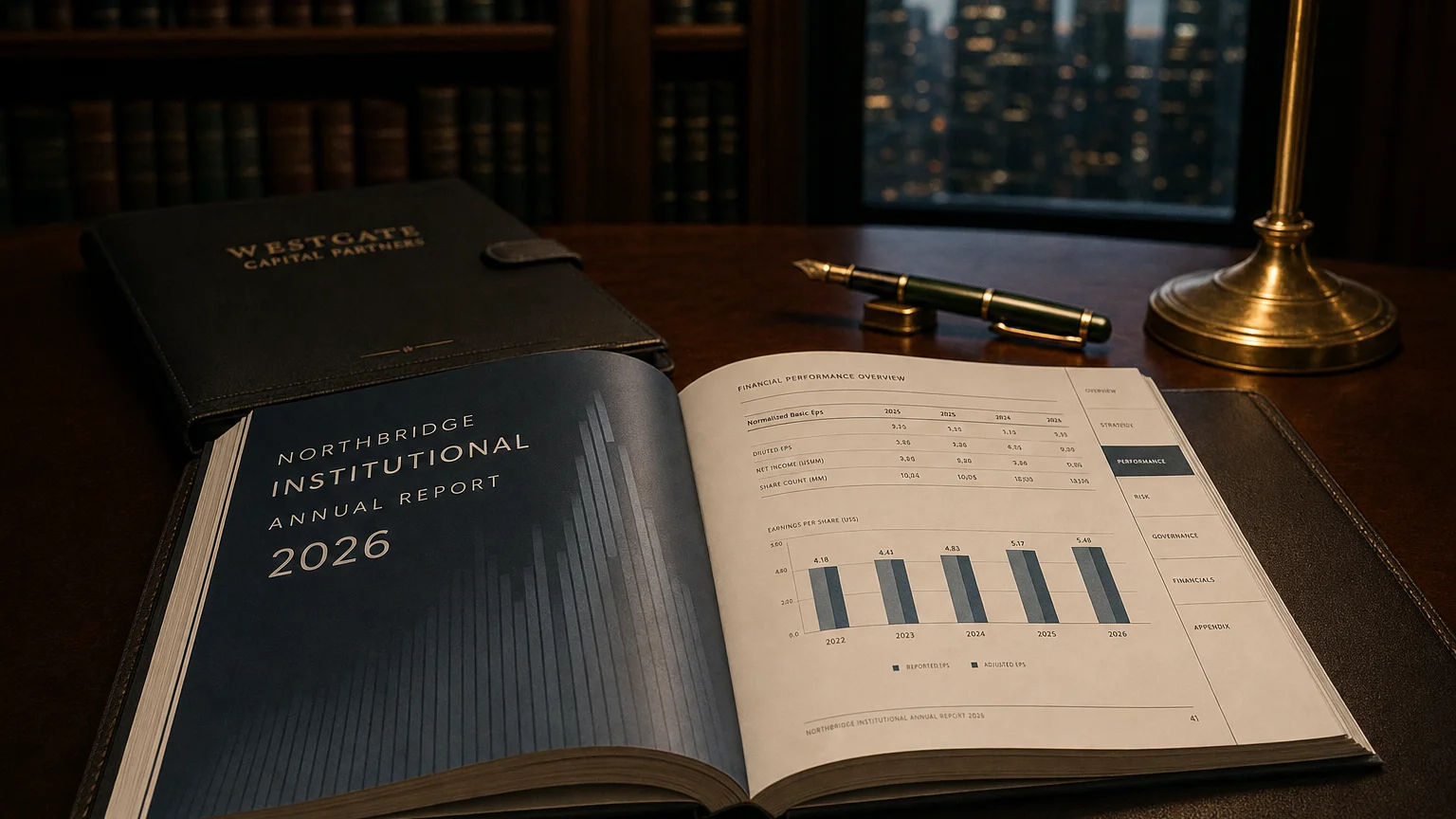

Normalized Basic EPS (Earnings Per Share) is a widely used non-GAAP metric that reflects a company’s sustainable, recurring profitability on a per-share basis by removing the impact of unusual or non-recurring items from reported earnings. Unlike diluted EPS, the basic version uses only the actual weighted average common shares outstanding and ignores potential dilution from convertible securities, options, or warrants. This provides a straightforward, less conservative view of core earnings that analysts and investors use to assess ongoing performance and compare companies more accurately.

What is Normalized Basic EPS?

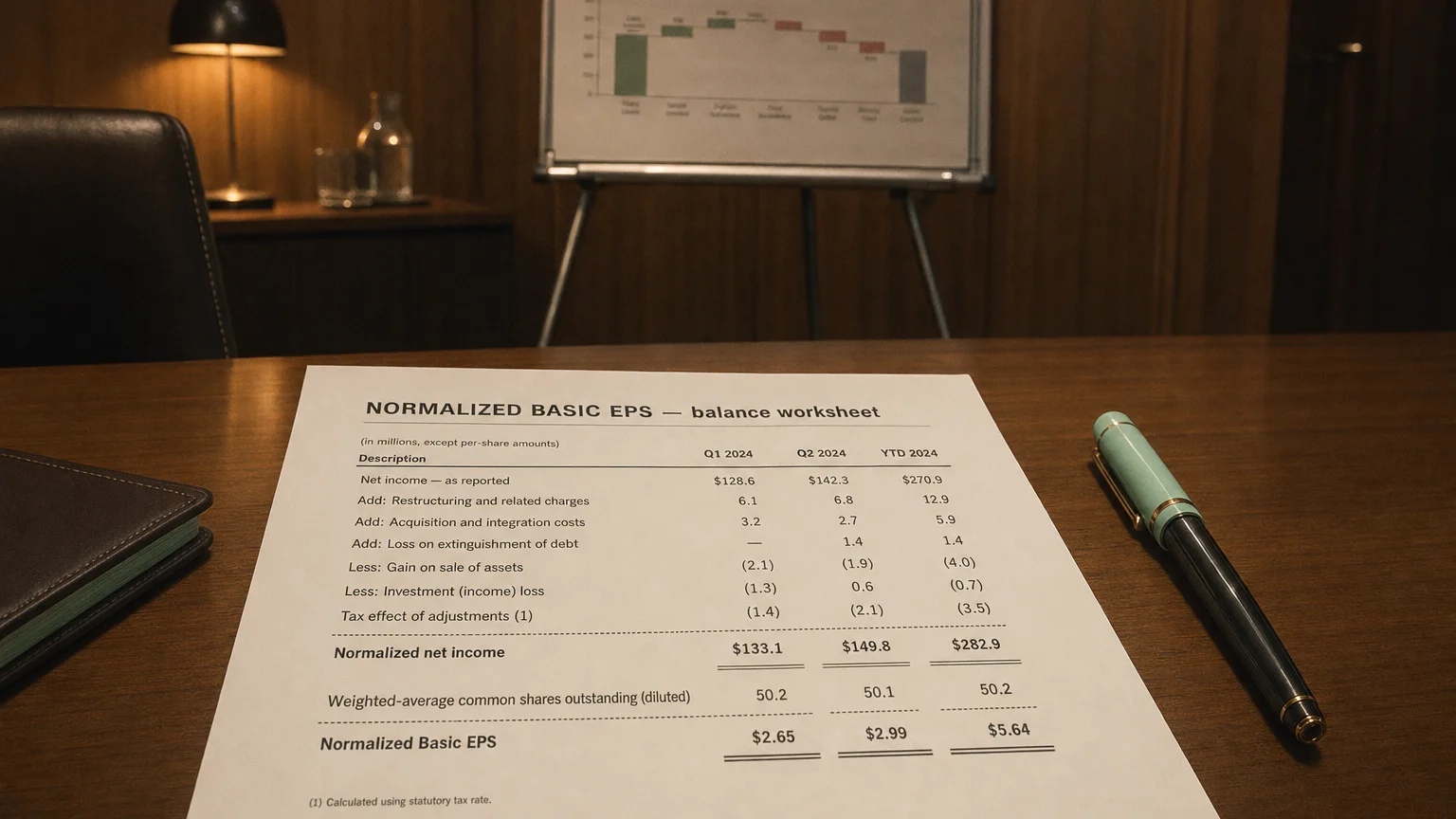

Normalized Basic EPS adjusts the company’s reported net income by adding back or subtracting non-recurring (unusual) items—net of their tax effects—and then divides the resulting normalized earnings by the basic weighted average number of common shares outstanding during the period.

This metric strips away temporary noise such as restructuring charges, asset impairments, litigation settlements, or gains from business sales, giving a clearer picture of the earnings generated from core operations. Because it uses basic shares, it does not assume conversion of potentially dilutive securities, making it simpler and often higher than its diluted counterpart.

Companies frequently highlight normalized basic EPS in earnings releases and investor presentations to emphasize sustainable profitability.

How is Normalized Basic EPS Calculated?

The calculation involves two main steps: normalizing the income and then applying the basic share count.

Formula: Normalized Basic EPS = (Normalized Net Income Available to Common Shareholders) ÷ (Basic Weighted Average Shares Outstanding)

Where:

- Normalized Net Income = Reported Net Income ± After-tax Unusual Items

- Net Income Available to Common = Normalized Net Income − Preferred Dividends

Step-by-Step Process

- Start with reported net income.

- Identify unusual items (e.g., restructuring, impairments).

- Adjust for tax effect of those items.

- Add back unusual expenses or subtract unusual gains (net of tax).

- Subtract any preferred dividends.

- Divide by basic average shares (no dilution adjustments).

Tip: The exact adjustments can vary by company—always refer to the reconciliation table in financial filings.

“I don’t want a lot of good investments; I want a few outstanding ones.”

— Philip Fisher, Author, Common Stocks and Uncommon Profits Common Stocks and Uncommon Profits (1958)

Examples of Normalized Basic EPS

Practical examples demonstrate how normalization affects the metric.

Example 1: Unusual Expense Adjustment

Company XYZ reports net income of 30M pre-tax impairment charge. Tax rate: 30%. Basic shares: 50M.

After-tax impairment: 21M. Normalized Income: 21M = 100M / 50M = 121M / 50M = $2.42.

Example 2: Unusual Gain Adjustment

Company ABC reports 40M pre-tax gain on asset sale. Tax rate: 25%. Basic shares: 60M.

After-tax gain: 30M. Normalized Income: 30M = 150M / 60M = 120M / 60M = $2.00.

These adjustments help reveal the earnings power from ongoing operations rather than one-time events.

Importance in Financial Analysis

Normalized Basic EPS is a key input for valuation models, especially when calculating forward price-to-earnings (P/E) ratios based on expected core earnings. It facilitates better year-over-year and peer-group comparisons by removing distortions.

Analysts often prefer normalized metrics for forecasting because recurring earnings are more predictable. A consistently higher normalized EPS versus reported EPS may indicate frequent non-recurring charges, warranting further investigation.

Warning: Excessive or recurring ‘unusual’ items can suggest poor underlying performance—normalized figures should not be taken at face value without scrutiny.

Financial data providers frequently list both reported and normalized basic EPS side-by-side in income statement breakdowns.

Q · 01What is Normalized Basic Eps?+