Company-Reported Adjusted Diluted Earnings Per Share Excluding Non-Recurring Items

From the standpoint of an institution, the existence of a risk manager has less to do with actual risk reduction than it has to do with the impression of risk reduction.

Reported Normalized Diluted EPS is a metric that combines three concepts – the earnings per share reported under official accounting (GAAP), adjustments to normalize earnings by removing one-off items, and dilution effects from potential shares. This measure shows a company’s per-share profit from normal operations, assuming all possible shares (from options, warrants, convertibles) are counted. Below, we break down each component, explain how this figure is calculated, compare GAAP vs. normalized EPS, discuss why analysts use normalized diluted EPS, and provide examples of typical one-time adjustments.

Key Definitions

-

Reported EPS (GAAP EPS): Reported earnings per share is the official EPS figure that a company must report in its financial statements under Generally Accepted Accounting Principles (GAAP). It is calculated as net income attributable to common shareholders divided by the weighted-average number of shares outstanding. Importantly, this GAAP EPS includes all revenues and expenses of the period – even unusual or one-time items – which can sometimes make it misleading. For example, a one-time gain from selling a subsidiary or asset would boost GAAP EPS for that period, while a large “unusual” expense might drag it down. Reported (GAAP) EPS is often provided in two forms: basic and diluted, both of which are required in SEC filings.

-

Normalized EPS (Adjusted EPS): Normalized earnings per share represents an adjusted EPS that excludes the impact of irregular or non-recurring items to reflect a company’s core, ongoing performance. In other words, it’s an EPS figure based on normal profit, stripping out one-off gains or losses, unusual charges, or seasonal variations. The goal is to present a clearer picture of the company’s underlying earnings power without the noise of extraordinary events. This metric (also called “ongoing,” “pro forma,” or adjusted EPS) omits items like one-time restructuring costs, asset sale gains, or other non-core impacts so that investors can gauge the sustainable earnings from core operations. Because normalized EPS is a non-GAAP measure, companies typically reconcile it to GAAP earnings in their reports, and investors use it to make apples-to-apples comparisons of performance over time.

-

Diluted EPS: Diluted earnings per share is the EPS calculated assuming all potential shares that could dilute ownership are in fact issued. It starts with the same net income figure (or adjusted net income, if looking at normalized EPS) and divides by a larger number of shares, including not just actual shares outstanding but also convertible securities (such as convertible bonds or preferred stock) and stock options/warrants that are “in the money”. Diluted EPS provides a more conservative measure of profitability per share, since it shows the earnings spread across the maximum possible number of shares. This means diluted EPS will be lower than basic EPS if a company has dilutive instruments, reflecting the potential reduction in each share’s claim on earnings. Analysts pay close attention to diluted EPS because it highlights the risk of share dilution and its impact on shareholder value. (If there are no dilutive securities, diluted EPS equals basic EPS.) Public companies must report both basic and diluted EPS, giving a comprehensive view of earnings per share.

How “Reported Normalized Diluted EPS” Is Calculated

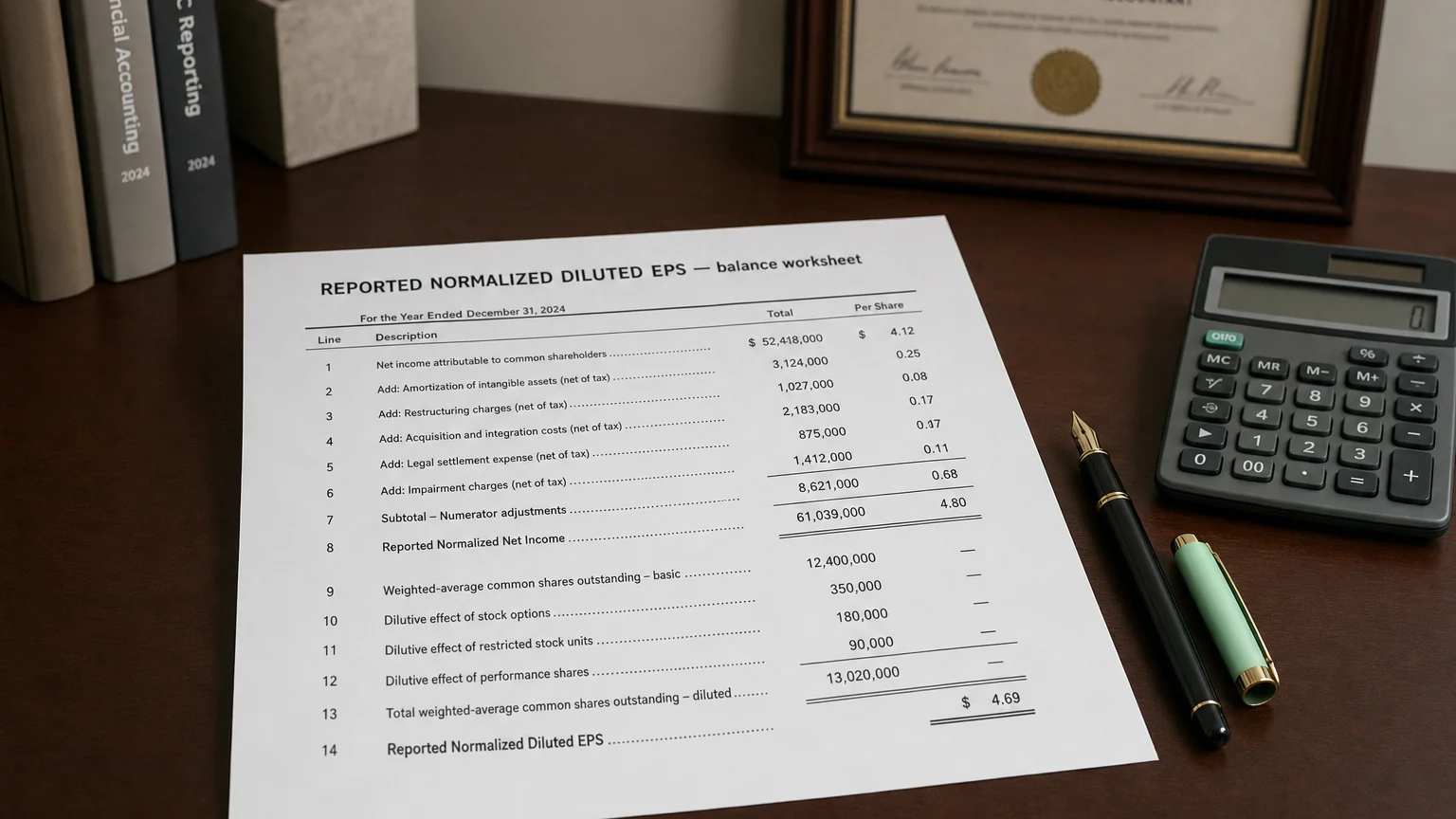

Calculating reported normalized diluted EPS involves adjusting earnings for one-time items and using the diluted share count. In practice, the calculation works as follows:

-

Start with GAAP Net Income: Begin with the company’s reported net income (or net earnings) attributable to common shareholders for the period. This is the profit figure that GAAP EPS would normally use.

-

Adjust for One-Time Items: Remove any non-recurring gains or unusual losses/expenses to derive normalized earnings. This means subtracting out any one-off income (e.g. a gain from selling a business unit) and adding back one-off losses or expenses (e.g. an impairment charge or restructuring cost) that are not expected to recur. The goal is to compute the earnings from normal operations. For instance, if net income included a $100 million gain from an asset sale, the normalized earnings would exclude that $100 million to avoid overstating ongoing profit. These adjustments yield Normalized Net Income for the period.

-

Include Potential Shares (Dilution): Determine the diluted weighted-average shares outstanding for the period. This starts with the basic weighted-average common shares and then adds all dilutive potential shares – for example, shares from convertible debt or preferred stock (if converted to common), and shares that would be created by exercised stock options or warrants. By assuming all these instruments are converted to equity, we get the total possible shares that could be outstanding. (Typically, the treasury stock method and if-converted method are used to calculate the incremental shares from options and convertibles, respectively, in accordance with accounting standards.)

-

Divide Normalized Earnings by Diluted Shares: Finally, calculate Normalized Diluted EPS by dividing the adjusted earnings (from step 2) by the diluted share count (from step 3). This gives the profit per share on a fully diluted basis, using earnings from normal operations. In formula form:

as opposed to GAAP diluted EPS which would use the unadjusted net income. For example, Investopedia explains that diluted normalized EPS is essentially profit (less one-time gains) divided by the sum of actual and potential shares outstanding. Because the denominator is larger (due to dilution), the normalized diluted EPS will typically be lower than the normalized basic EPS for the same period. This calculation yields the “reported normalized diluted EPS” figure often seen in financial summaries, indicating what the company earned per share from its ongoing operations, on a diluted basis.

GAAP EPS vs. Normalized EPS (Reported vs. Adjusted)

It’s important to distinguish between GAAP EPS (as-reported EPS) and Normalized EPS (adjusted EPS):

-

GAAP EPS (Reported EPS) includes all items recognized under accounting rules for the period. This means that GAAP EPS reflects actual net income, which can be swelled by unusual gains or depressed by one-time losses. It is the EPS figure that appears in the official financial statements and is calculated strictly according to GAAP or IFRS. Every public company must report GAAP EPS in its income statement (both basic and diluted). However, GAAP EPS can sometimes paint a distorted picture of ongoing performance. For example, a large one-off gain from selling a division or a lump-sum legal settlement might significantly boost that quarter’s EPS under GAAP. Conversely, a company might incur a big expense and label it an “unusual” or “extraordinary” charge that still reduces GAAP net income (unless classified under discontinued operations). GAAP EPS is thus volatile to such events and may not repeat in future periods.

-

Normalized EPS (Non-GAAP EPS) strips out those irregular influences to focus on core earnings. Also called pro forma or adjusted EPS, it excludes unusual one-time gains or losses to show what the EPS would have been from normal operations. The idea is that by removing anomalies (like a big asset sale gain, an impairment loss, etc.), normalized EPS gives a better indication of the company’s recurring earning capacity. This makes period-to-period comparisons more meaningful. For instance, if a company’s GAAP diluted EPS was $2.00 but included a $0.50 gain from a lawsuit, the normalized diluted EPS might be only $1.50 after removing that gain – reflecting the underlying profit from regular business. Unlike GAAP EPS, normalized EPS is a non-GAAP metric, so it isn’t defined by standard accounting rules; companies define their own adjustments (which they must disclose). Investors should always check the reconciliation to see which items were excluded, since overly liberal “adjustments” can be misleading (some firms might label frequent expenses as “non-recurring” to inflate adjusted EPS). Nonetheless, when done in good faith, normalized EPS allows a clearer “core EPS” comparison across periods or against other companies without temporary distortions.

In summary: GAAP EPS (reported EPS) is required and all-inclusive, while Normalized EPS is supplemental and exclusive of irregular items. GAAP EPS shows actual earnings per share by accounting standards, whereas normalized EPS shows an arguably more economic earnings per share by removing noise. It’s common for a company’s normalized (adjusted) EPS to differ from GAAP EPS, and both figures can be useful: GAAP EPS for measuring real profitability including all costs, and normalized EPS for analyzing ongoing performance trend.

Why Use Normalized Diluted EPS vs. Basic or GAAP EPS

Analysts and companies often focus on normalized diluted EPS because it provides a more realistic and stable view of earnings per share, for several reasons:

-

Accounts for Full Dilution: Using diluted EPS (instead of basic) incorporates the impact of all potential shares. This matters to investors because it shows a “worst-case” scenario for EPS if all stock options are exercised and all convertible securities turn into shares. Diluted EPS is considered more conservative and comprehensive – if there is little difference between a company’s basic and diluted EPS, it signals low risk of future dilution; a big gap signals significant potential dilution that could reduce future EPS. Thus, analysts prefer diluted EPS to ensure they aren’t overestimating earnings per share. In fact, publicly traded firms are required to report both figures to give a full picture, and investors tend to value companies with stable diluted EPS more favorably. By using diluted shares in the EPS calculation, one can identify companies where lots of convertible debt or stock options could drag down EPS in the future.

-

Focuses on Core Earnings: Using normalized EPS (instead of GAAP) helps investors and management home in on the company’s core operating performance without the distractions of irregular events. This is particularly useful for forecasting and valuation. For example, when projecting next year’s earnings or calculating price-to-earnings ratios, one-time events from the past are not likely to recur, so normalized EPS provides a better base. It offers a “truer picture of underlying profitability,” as Investopedia notes, and is a more conservative yardstick for analysis and valuation than headline GAAP EPS. Analysts often track normalized (adjusted) EPS over time to gauge a firm’s earnings trend and compare it to peers, believing it reflects the sustainable earnings power of the business. Companies, for their part, frequently present a normalized or adjusted EPS in earnings releases to demonstrate how their ongoing business is faring, especially if GAAP results are skewed by outliers. This non-GAAP EPS can aid in equity valuation, making peer comparisons more fair and highlighting the effects of management decisions excluding extraneous events.

-

When It’s Used: Normalized diluted EPS is used in scenarios like equity research and valuation, where consistency is key. For instance, when computing valuation multiples (P/E ratios), using GAAP EPS that includes a big one-time gain could make a company look cheaper (lower P/E) than it truly is on a recurring basis. Adjusting earnings to normalize them ensures that such comparisons aren’t skewed. Similarly, management might use normalized EPS when setting performance targets or giving earnings guidance, to exclude known one-off impacts (e.g. “We expect FY25 normalized diluted EPS of $5.00”). Investors and rating agencies also look at adjusted earnings metrics to assess creditworthiness and dividend sustainability, reasoning that normalized earnings better indicate the company’s ability to generate cash consistently. In summary, normalized diluted EPS is preferred for evaluating ongoing performance and value, whereas GAAP EPS is used for compliance and an absolute measure of profit, and basic EPS might be seen as optimistic if a firm has dilution risk.

Typical One-Time Items Excluded in Normalization

When calculating normalized EPS, companies adjust for non-recurring or unusual items that are not indicative of the normal course of business. Here are some common one-time items that are often excluded (taken out of earnings) in normalization:

-

Restructuring Charges: Costs related to major reorganizations, such as layoffs, plant closures, or business restructuring efforts. These can include severance pay, facility exit costs, and fees for turnaround consultants. Such expenses are incurred during one-time corporate changes and are not part of regular operations.

-

Litigation Gains/Expenses: Large legal costs or settlement payments for lawsuits, or conversely one-time lawsuit awards/insurance recoveries. For example, a big penalty paid to settle a lawsuit (or a one-time gain from winning a court case) is treated as non-recurring. Companies remove these legal one-offs to avoid skewing the profit trend with an event that (hopefully) won’t repeat.

-

Asset Sale Gains or Losses: Profits or losses from selling a business unit, property, or investment that is not part of the company’s day-to-day revenue generation. For instance, if a manufacturer sells a factory or a subsidiary and records a gain, that gain is excluded from normalized earnings. Similarly, any loss on such disposal would be added back, since it’s a one-time transaction.

-

Impairments or Write-Downs: Significant write-downs of assets (e.g. goodwill impairment, inventory write-offs, or write-down of equipment). These accounting charges occur when an asset’s book value is permanently reduced due to loss of value. Impairment charges can be large and infrequent, so they are commonly added back for normalized EPS calculations.

-

Discontinued Operations: Income or loss from a business segment that the company has divested or shut down. By accounting rules, results of discontinued operations are often reported separately from continuing operations. In any case, since those operations are not ongoing, their earnings effect is removed to normalize the continuing EPS.

-

Merger & Acquisition Costs: One-time expenses related to mergers, acquisitions, or divestitures – such as investment banking fees, due diligence costs, or integration expenses for an acquired business. These M&A-related costs hit the income statement around the deal time and are not recurring, so normalized results will exclude them.

-

Extraordinary or Unusual Events: Any other infrequent events that significantly affect profit, such as natural disaster losses (e.g. a hurricane destroying a facility) or early debt retirement costs. Under U.S. GAAP, truly extraordinary items (both unusual and infrequent) used to be reported separately – while this classification is no longer allowed, companies still adjust for things like disaster-related losses or other rare events when presenting adjusted earnings. The idea is to remove the financial impact of events that are not expected to occur again in the foreseeable future.

Each company will specify which items it has excluded to arrive at its normalized (adjusted) EPS. The above are typical examples. By leaving out these one-time gains and losses, Reported Normalized Diluted EPS aims to show what the per-share earnings really look like from the company’s core operations on an ongoing, fully diluted basis. This helps investors make better-informed decisions by focusing on sustainable earnings rather than transient spikes or dips in profitability

Q · 01What is Reported Normalized Diluted Eps?+