Net Income Including Non-Controlling Interests is a financial concept covered in this article.

When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.

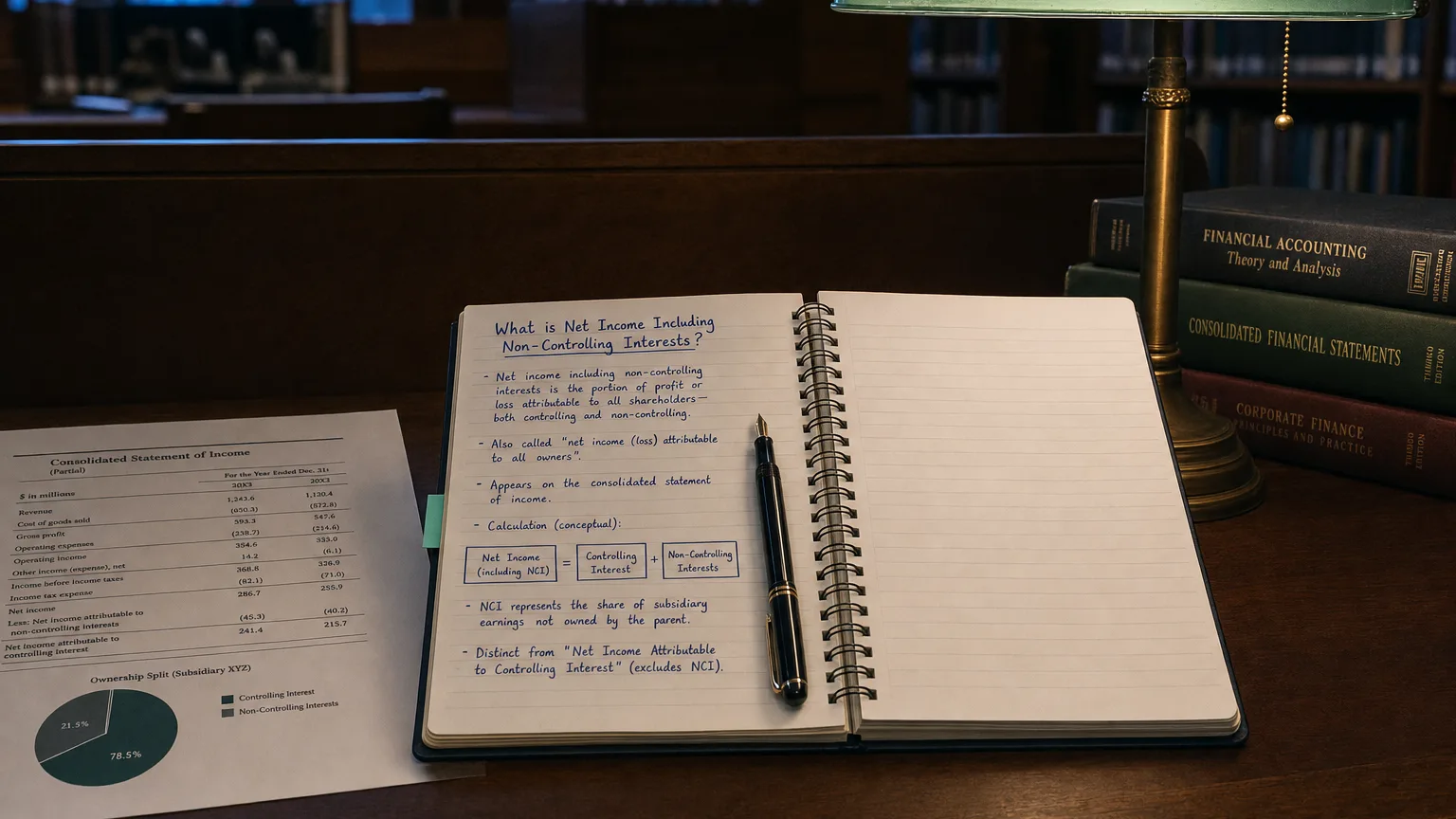

Net Income Including Non-Controlling Interests (sometimes called consolidated net income) is the total bottom-line profit of a parent company and all its subsidiaries, before splitting out any minority ownership share. In other words, it’s the net income of the entire group after all revenues, expenses, and taxes—including the portion of profit that belongs to shareholders outside of the parent company. This figure reflects the combined earnings of the group as if it were one entity. A non-controlling interest (NCI), formerly called minority interest, represents the equity ownership of less than 50% in a subsidiary that a parent company controls. When financial statements are consolidated, 100% of a subsidiary’s income is included, resulting in a net income figure that includes the NCI’s share.

How It Is Calculated and Presented

The calculation follows the normal income statement flow to arrive at net income for the entire consolidated group. The key is in the presentation on the income statement:

- First, a line for “Net income including non-controlling interests” is shown.

- Next, there is a deduction for “Net income attributable to non-controlling interests.”

- Finally, the remainder is shown as “Net income attributable to [Parent Company],” which is the amount belonging to the parent’s shareholders.

This presentation is required by accounting standards like U.S. GAAP and IFRS so that readers can distinguish between the total profit of the group and the portion that actually belongs to the parent company’s owners.

“When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1985 (1985)

Example: Splitting Net Income

The Walt Disney Company’s 2019 consolidated income statement provides a clear example of how net income is allocated.

Walt Disney Co. (2019)

Simplified Scenario

If Parent Co. owns 80% of Subsidiary X, and Subsidiary X earns **100. Then, it subtracts 80 as the net income attributable to Parent Co.’s shareholders.

Why This Distinction Is Relevant

Separating net income into these two pieces is important for transparency and accurate financial analysis.

- Complete View: Net income including NCI gives a complete picture of the group’s total profitability, which is useful for creditors and analysts assessing the earning power of the entire consolidated entity.

- Shareholder Relevance: From the perspective of the parent company’s shareholders, the net income attributable to the parent is more relevant, as it represents the earnings that actually belong to them.

- Accurate Ratios: Financial ratios like Earnings Per Share (EPS) are calculated using the net income attributable to the parent’s common shareholders to ensure the metric only reflects the profit share belonging to them.

- Clarity on Earnings: This presentation allows stakeholders to see how much of the consolidated profit was retained by the parent versus allocated to minority owners. If a large portion of profits is going to non-controlling interests, the parent’s shareholders can see that those earnings are not available to them.

Including NCI vs. Attributable to Shareholders

To summarize the key difference: Net income including non-controlling interests is the broadest measure of profit, encompassing all owners of the group’s subsidiaries. Net income attributable to shareholders of the parent is the bottom-line profit that belongs solely to the parent company’s shareholders, after removing the NCI’s portion.

The Pie Analogy

Think of it like a pie. The whole pie represents net income including NCI. One slice of that pie is set aside for the minority-interest owners. The remainder of the pie is the net income for the parent’s shareholders.