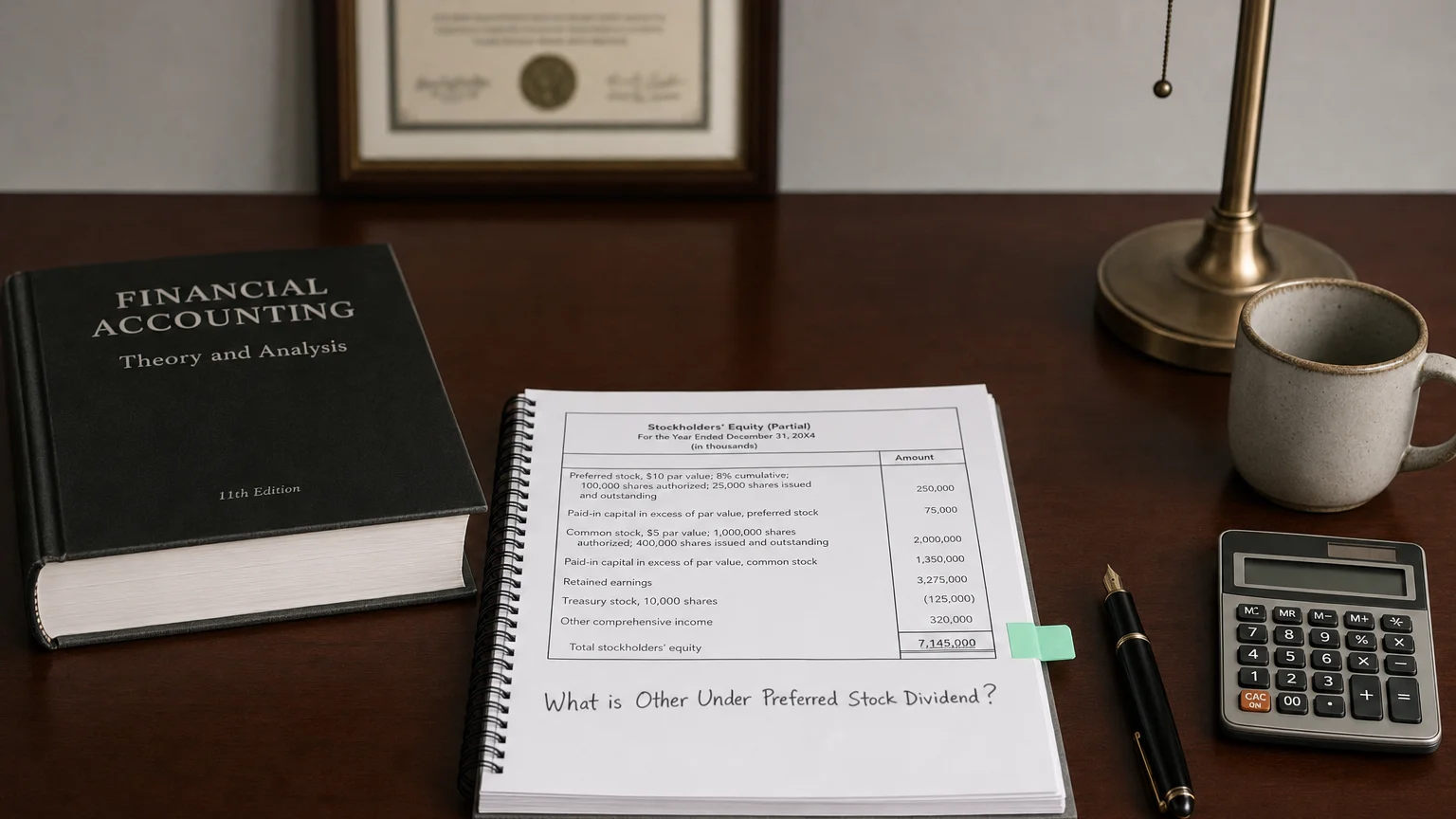

Other Under Preferred Stock Dividend is a financial concept covered in this article. Additional Adjustments and Charges Deducted After Preferred Dividends

The intelligent investor is a realist who sells to optimists and buys from pessimists.

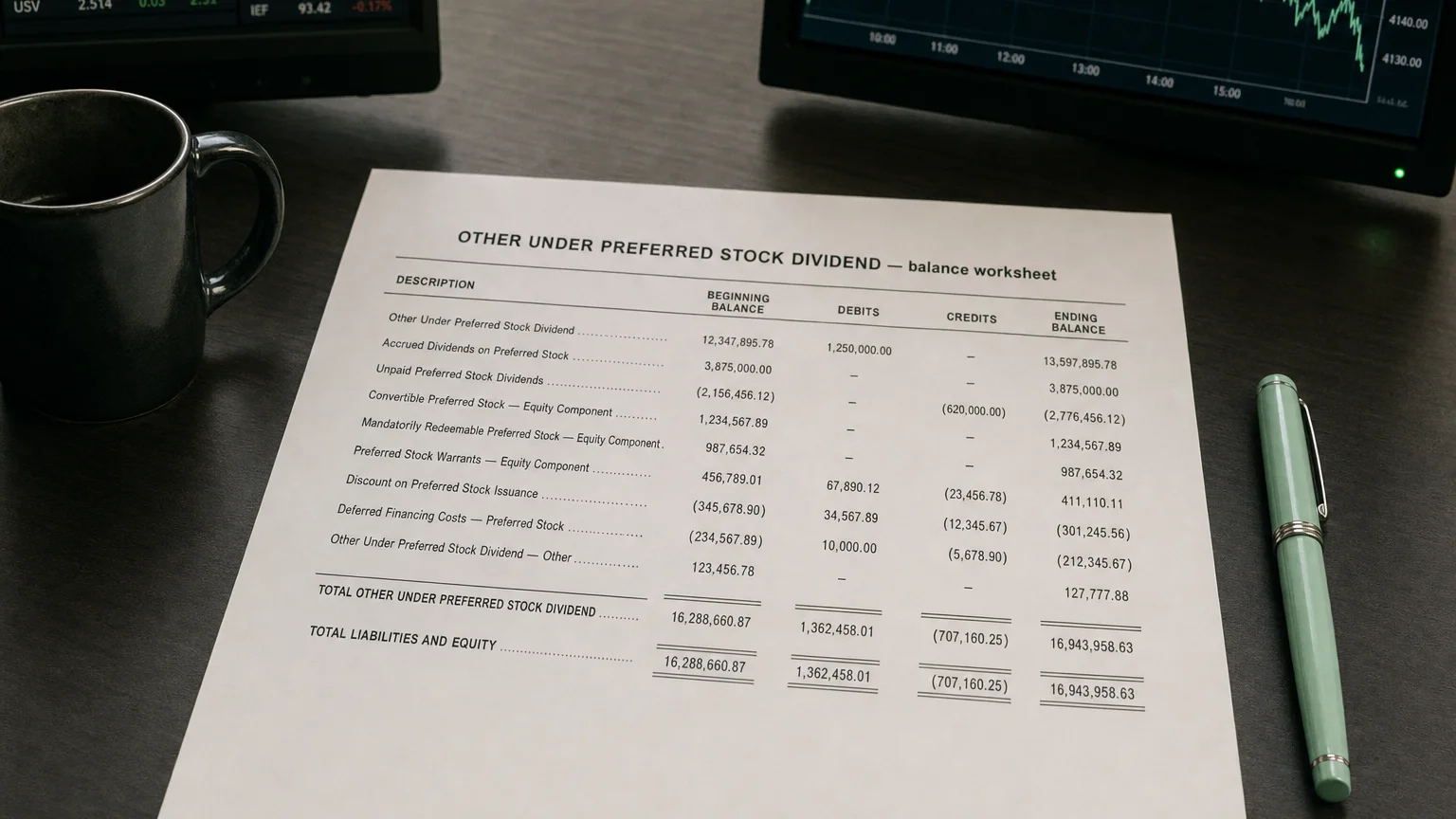

Other Under Preferred Stock Dividend refers to miscellaneous deductions or adjustments that are subtracted from net income after the deduction of preferred stock dividends but before arriving at the final net income available to common stockholders. These items typically include certain non-controlling interest adjustments, specific preferred stock-related charges beyond regular dividends, or other priority claims that rank below standard preferred dividends but above common shareholders. This line item ensures accurate allocation of earnings and is part of the detailed attribution of net income in complex capital structures.

What is Other Under Preferred Stock Dividend?

Other Under Preferred Stock Dividend captures additional deductions that occur in the net income attribution waterfall after regular preferred stock dividends have been subtracted but before the remaining earnings are allocated to common stockholders.

These can include accrued dividends on certain cumulative or participating preferred stock series, adjustments for redeemable preferred stock, or other contractually obligated payments that have priority over common shares but are not classified as standard preferred dividends.

This line is most commonly seen in detailed income statement breakdowns from financial data providers when companies have multiple classes of preferred stock or hybrid securities.

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

— Benjamin Graham, Author, The Intelligent Investor The Intelligent Investor (1949)

Common Items Included

Typical components may include:

Examples of Items

- Accrued but undeclared dividends on cumulative preferred stock

- Participating dividends where preferred holders get additional payouts

- Deemed dividends on redeemable or convertible preferred stock

- Adjustments for preferred stock issuance costs or discounts

- Certain non-controlling interest allocations related to preferred-like instruments

- Other contractual obligations ranking between preferred and common

The exact composition varies by company capital structure and accounting classifications.

How It Affects Net Income Attribution

The flow in the income statement attribution is:

Formula: Net Income − Preferred Stock Dividends − Other Under Preferred Stock Dividend = Net Income Available to Common Stockholders

This ensures that all priority claims are deducted before earnings reach common shareholders, impacting basic and diluted EPS calculations.

Tip: A non-zero value often indicates complex preferred equity instruments—review the equity footnotes for details.

Examples

Example 1: Participating Preferred

Net Income: $300M

Standard Preferred Dividends: 5M Other Under Preferred Stock Dividend: 300M − 5M = $275M

Example 2: Redeemable Preferred Adjustment

Company has redeemable preferred stock accounted for as mezzanine equity.

Accretion/deemed dividend adjustment: 12M Other Under Preferred Stock Dividend: 20M reduce earnings available to common.

Such adjustments can meaningfully reduce reported earnings available to common shareholders.

Importance in Financial Analysis

Analysts monitor this line to:

- Understand the full cost of preferred equity financing

- Accurately assess earnings truly available to common shareholders

- Evaluate capital structure complexity and potential dilution

Persistent or growing values may indicate increasing obligations to preferred holders, potentially at the expense of common shareholders.

Warning: These deductions are non-cash in many cases but still reduce reported EPS—distinguish from operating performance.

Q · 01What is Other Under Preferred Stock Dividend?+