Preferred Stock Dividends is a financial concept covered in this article. Priority Dividend Payments to Preferred Shareholders Before Common Stockholders

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

Preferred Stock Dividends represent the fixed or cumulative dividend payments that a company is obligated to pay to its preferred stockholders before any dividends can be distributed to common stockholders. These dividends are typically set as a fixed percentage of the preferred stock’s par value or a specified dollar amount per share. This line item is deducted from net income to arrive at the earnings available to common shareholders, directly impacting basic and diluted EPS calculations. Understanding preferred dividends is essential for assessing the true earnings power available to common equity holders.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

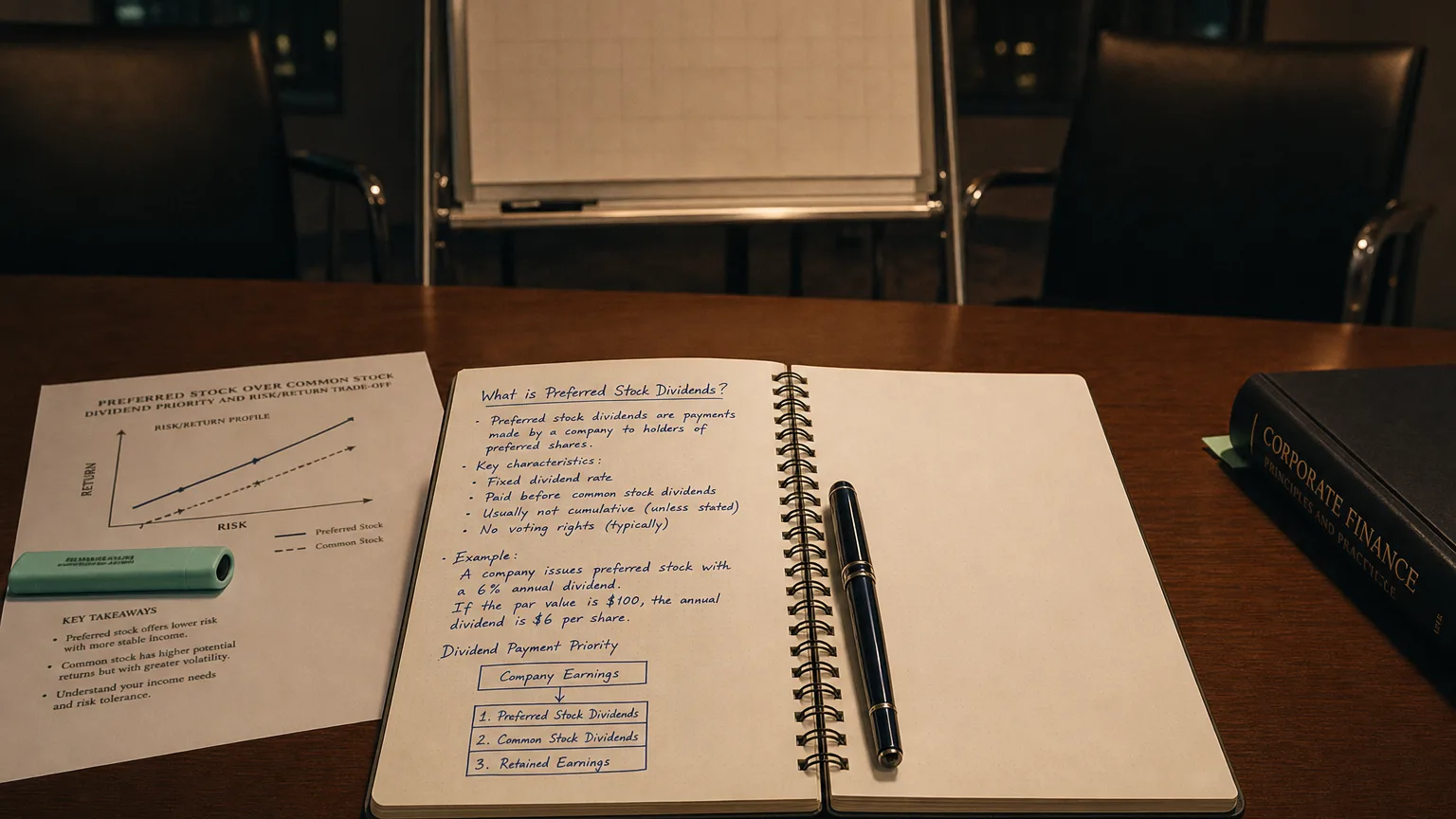

What are Preferred Stock Dividends?

Preferred Stock Dividends are the contractual dividend obligations associated with preferred shares, a hybrid security that has characteristics of both debt and equity. Preferred stockholders have a higher claim on earnings and assets than common stockholders but typically lower than bondholders.

These dividends are usually fixed (e.g., 6% of par value) and often cumulative, meaning if skipped in one period, arrears must be paid before any common dividends. Non-cumulative preferred dividends do not accumulate if missed.

In the income statement, preferred dividends are subtracted from net income to compute earnings available to common shareholders, even though they are not a tax-deductible expense.

How Preferred Dividends Affect Earnings Attribution

The standard flow is:

Formula: Net Income − Preferred Stock Dividends − Other Adjustments (if any) = Net Income Available to Common Stockholders

This reduced amount is then used as the numerator for basic EPS. For diluted EPS, additional adjustments (e.g., adding back dividends on dilutive convertible preferred) may apply.

Tip: Preferred dividends are declared by the board and may include current-period obligations plus any cumulative arrears.

Examples

Example 1: Simple Fixed Dividend

Company has $100M in preferred stock at 7% dividend rate.

Annual Preferred Stock Dividends = 7M. Net Income: 150M − 143M.

Example 2: Cumulative Arrears

Prior year skipped dividends: $5M arrears.

Current year obligation: 13M (arrears paid first). Net Income: 120M − 107M. No common dividends possible until arrears cleared.

Cumulative features protect preferred holders but can significantly reduce common earnings in tough years.

Importance in Financial Analysis

Analysts focus on this line to:

- Calculate true earnings available to common shareholders

- Assess the cost of preferred equity financing

- Evaluate dividend coverage and sustainability for common stock

Large preferred dividends relative to net income can limit common dividend growth or signal higher financial risk. Convertible preferred may have different treatment in diluted calculations.

Warning: Preferred dividends are non-deductible for tax purposes, unlike interest expense, making preferred stock more expensive than debt in many cases.