Average Dilution Earnings is the after-tax interest expense saved on convertible debt — added to basic net income available to common stockholders — when calculating diluted EPS under the if-converted method.

It does not matter how frequently something succeeds if failure is too costly to bear.

What Is “Average Dilution Earnings”?

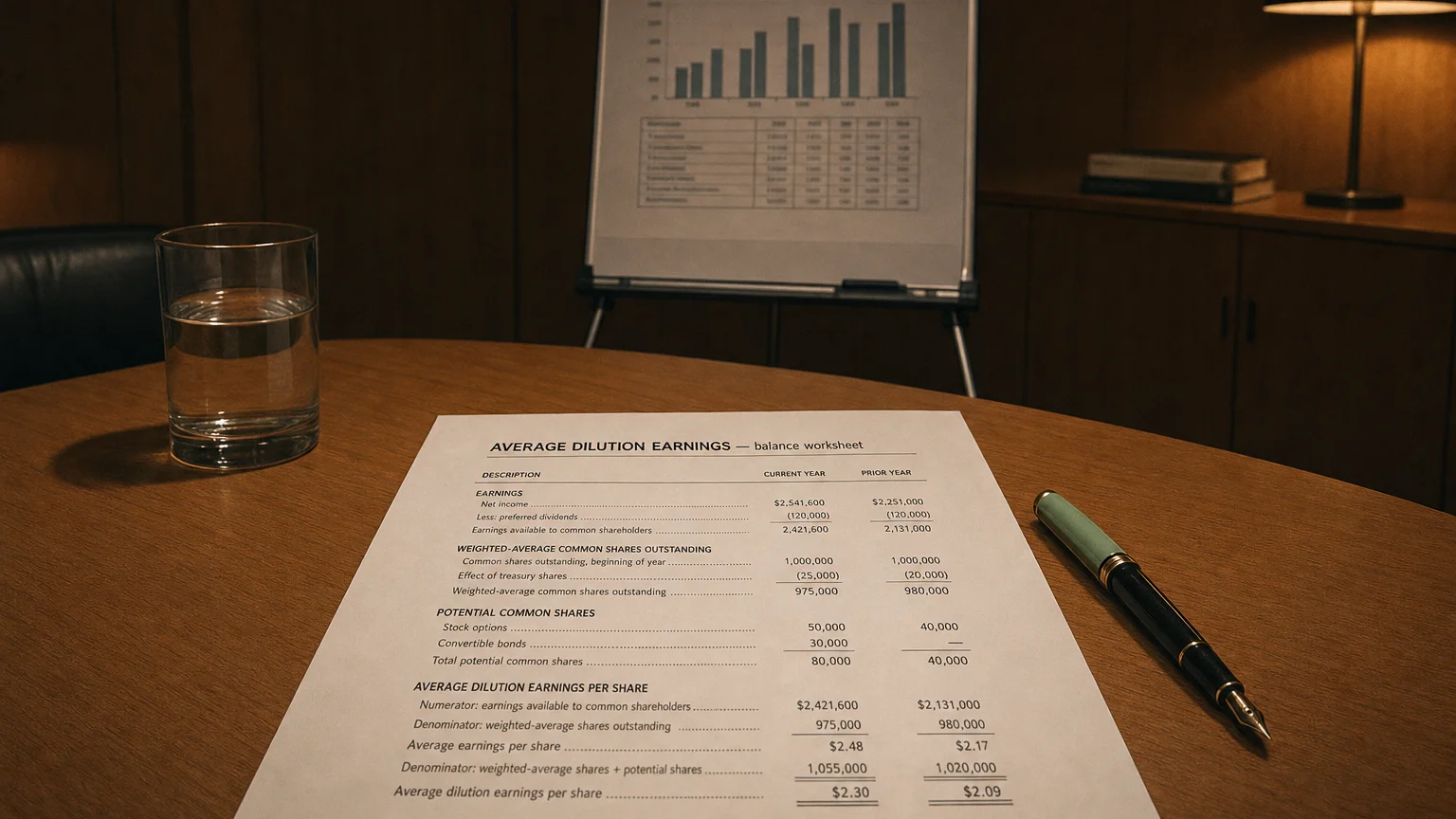

Average Dilution Earnings is a term sometimes seen on summarized income statements (e.g. on financial data platforms) that represents the adjustment made to a company’s earnings for the purpose of calculating diluted earnings per share (EPS). In essence, it bridges the gap between the net income available to common shareholders (used for basic EPS) and the adjusted net income used for diluted EPS. This figure accounts for any changes in earnings that would result if all dilutive securities (like convertible bonds or preferred stock) were converted to common stock. For example, IBM’s income statement shows net income to common shareholders of $5,590 million and an “Average Dilution Earnings” of -$2 million, resulting in a diluted net income available to common of $5,588 million. In practical terms, Average Dilution Earnings captures the numerator adjustment in the diluted EPS formula – such as adding back interest expense or dividends that would be saved upon conversion of dilutive instruments.

Diluted Earnings Per Share (EPS) and Its Numerator Adjustment

Diluted EPS measures a company’s earnings per share assuming all possible dilutive securities are converted into common shares. This is a more conservative metric than basic EPS, providing a “worst-case” scenario for shareholders by showing the lowest possible EPS if all outstanding options, warrants, convertible bonds, and convertible preferred shares were exercised or converted. To ensure comparability, the diluted EPS calculation adjusts both the share count and the earnings figure:

-

Adjusted Earnings (Numerator): Start with net income available to common shareholders (after any actual preferred dividends). Then add back any expenses or charges that would not occur if dilutive securities were converted. For example, for convertible bonds, the after-tax interest expense is added back to earnings (since if the bonds convert to equity, the company would save that interest cost). Likewise, dividends on convertible preferred stock are added back if those shares are assumed converted to common. These adjustments are exactly what “Average Dilution Earnings” represents – the incremental earnings increase (or occasionally decrease) considered in diluted EPS. In IBM’s case above, the small negative adjustment implies a scenario where conversion slightly reduced net income to common (for instance, a special circumstance or rounding). More commonly, a positive adjustment indicates additional earnings available to common shareholders after adding back interest or dividend expenses saved by conversion. The result of these adjustments is often labeled “Diluted Net Income available to Common Stockholders”, reflecting the earnings figure used for diluted EPS.

-

Expanded Share Count (Denominator): Calculate the weighted average diluted shares outstanding, which includes all actual shares plus all potential shares from dilutive instruments. This means taking the weighted average common shares outstanding during the period (for basic EPS) and then adding the effect of all dilutive securities – stock options, warrants, convertible debt, convertible preferred stock, etc. – as if they were converted into common shares. For stock options and warrants, the treasury stock method is used: we assume those options are exercised and the hypothetical proceeds are used to repurchase common stock, with only the net new shares increasing the count. The outcome is an average fully diluted share count, often listed on financial statements as “Diluted Average Shares Outstanding”. This figure represents the denominator for diluted EPS and reflects the company’s total share base if all dilutive claims became common equity.

In formula form, Diluted EPS is essentially:

This formula shows how Average Dilution Earnings relates directly to diluted EPS – it modifies the earnings (numerator) to align with the expanded share count (denominator) used in the diluted EPS calculation.

Average Diluted Shares Outstanding (Diluted Share Count)

The term average diluted shares outstanding (also called weighted-average diluted shares) refers to the average number of shares outstanding during the period after accounting for all potential dilution. It is the share count used in the diluted EPS calculation. This metric includes not only the ordinary shares actually outstanding, but also additional shares that would be issued from the conversion or exercise of dilutive instruments (such as employee stock options, warrants, convertible preferreds, or convertible debt). The word “average” indicates that the figure is time-weighted over the reporting period, reflecting changes in the number of shares over time. In many financial reports, companies will explicitly disclose both the basic weighted-average shares and diluted weighted-average shares for the year or quarter. For instance, continuing the IBM example, the company reported Basic Average Shares of about 887.2 million and Diluted Average Shares of 892.8 million for 2020, indicating that roughly 5.6 million potential shares were added to the count for dilution effects. This dilutive share count is critical for computing diluted EPS and understanding the extent to which convertible securities could increase the share base and thus dilute existing shareholders’ ownership percentages.

How Diluted EPS is Calculated (Step-by-Step)

Analysts and accountants calculate diluted EPS by adjusting both earnings and shares to reflect dilution. The general process is:

-

Start with Basic Earnings: Take the company’s net income available to common stockholders for the period (after subtracting any preferred dividends). This is the numerator for basic EPS.

-

Add Back Convertible Expenses: Identify any dilutive securities and adjust earnings for them using the if-converted method. For convertible bonds, add back the after-tax interest expense to the net income (since if the bonds convert, that interest expense would be avoided). For convertible preferred stock, add back the preferred dividends (since those wouldn’t be paid if the preferred shares convert to common). These additions increase the earnings numerator and are captured in the “Average Dilution Earnings” line on some income statements. If no such securities exist (or if they are anti-dilutive), this adjustment would be zero.

-

Determine New Shares from Conversion: Calculate the number of potential common shares from each dilutive security. For convertible instruments, use their conversion ratios to find how many new shares would result if converted. For stock options and warrants, apply the treasury stock method: assume all in-the-money options/warrants are exercised and use the proceeds to repurchase shares at the average market price, with the remainder yielding incremental shares.

-

Compute Weighted Average Diluted Shares: Add the incremental shares from step 3 to the actual weighted average common shares outstanding. This yields the weighted average diluted shares outstanding for the period.

-

Calculate Diluted EPS: Divide the adjusted net income (from step 2) by the diluted share count (from step 4). The result is the diluted earnings per share. Companies typically report this figure alongside basic EPS at the bottom of the income statement. If the company had no dilutive securities, diluted EPS will equal basic EPS; otherwise, diluted EPS will be lower than or equal to basic EPS (never higher) because the earnings are spread over more shares.

Throughout this process, Average Dilution Earnings is essentially the outcome of step 2 – it quantifies the total earnings adjustment made for dilution. If a company’s dilutive securities require adding $10 million of after-tax interest back to net income and adding back $2 million of preferred dividends, for example, the Average Dilution Earnings line might show $12 million. That would then be added to the basic net income to get the diluted net income numerator. (Conversely, a negative value in that line would imply the adjusted diluted earnings are slightly lower than the reported net income to common, though such cases are less common in practice.)

Usage by Analysts and Investors

Analysts and investors pay close attention to diluted EPS and its components because they provide insight into a company’s true earnings power and capital structure. Key points regarding usage include:

-

Assessing Dilution Impact: Diluted EPS is a crucial metric for evaluating how much a company’s earnings per share could be diluted by additional share issuance. A small difference between basic and diluted EPS signals that the company has little dilution risk, which can be viewed favorably (existing shares aren’t under threat of major dilution). A large gap, on the other hand, indicates significant potential dilution from convertibles or options, alerting investors to be cautious about the quality of the EPS number. Analysts will often compare basic vs. diluted EPS to gauge this risk.

-

Valuation and Ratios: When calculating valuation ratios like the price-to-earnings (P/E) ratio, practitioners commonly use diluted EPS (or an even more conservative figure if available) to ensure they are not overestimating earnings on a per-share basis. Using diluted EPS provides a more conservative estimate of value, as it reflects the earnings attributable to all shares that could be outstanding. For example, a stock’s P/E based on basic EPS might look slightly cheaper than based on diluted EPS if the company has many in-the-money options or convertibles; the diluted metric gives a clearer picture of value by accounting for those extra shares.

-

Financial Planning and Analysis: Corporate finance professionals also consider diluted shares and earnings when forecasting and planning. If a company expects to issue more stock (via option grants, convertible debt, etc.), the future diluted EPS helps in projecting shareholder value and in communicating realistic earnings guidance.

-

Regulatory Reporting: Public companies are required to report both basic and diluted EPS in their financial statements, typically at the bottom of the income statement or in the notes. They also disclose the weighted average shares used for each. This transparency allows analysts to reconstruct the EPS calculation and identify the contribution of any Average Dilution Earnings adjustments. The disclosure of the numerator adjustments (e.g. interest added back) is often found in the footnotes, giving further detail on what makes up that dilution adjustment.

In summary, Average Dilution Earnings is a component of the earnings per share calculation that ensures a company’s diluted EPS properly reflects all sources of potential dilution in both the earnings figure and share count. It is closely related to diluted EPS (the end result metric) and the average diluted shares outstanding (the expanded share base), and it represents the earnings adjustment needed when hypothetically converting dilutive instruments into common stock. By understanding Average Dilution Earnings in conjunction with diluted EPS, investors and analysts can better appreciate how things like convertible securities and stock options can affect a company’s per-share earnings and, ultimately, the value of each share of stock. The use of diluted EPS (with its associated earnings adjustments) is a standard part of financial analysis, ensuring that one measures a company’s performance on a fully diluted basis – a prudent way to gauge the firm’s profitability per share in a scenario that protects against optimistic overstatement of earnings.

Sources: Diluted EPS definition and significance; Calculation of diluted EPS and if-converted adjustments; Example of “Average Dilution Earnings” on income statement (IBM data); Definition of diluted shares outstanding; Analyst interpretation of dilution risk.

Q · 01How is Average Dilution Earnings calculated?+

Q · 02Why does Average Dilution Earnings increase diluted net income?+