is a financial concept covered in this article. The 'Bottom Line' Profit of a Business

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

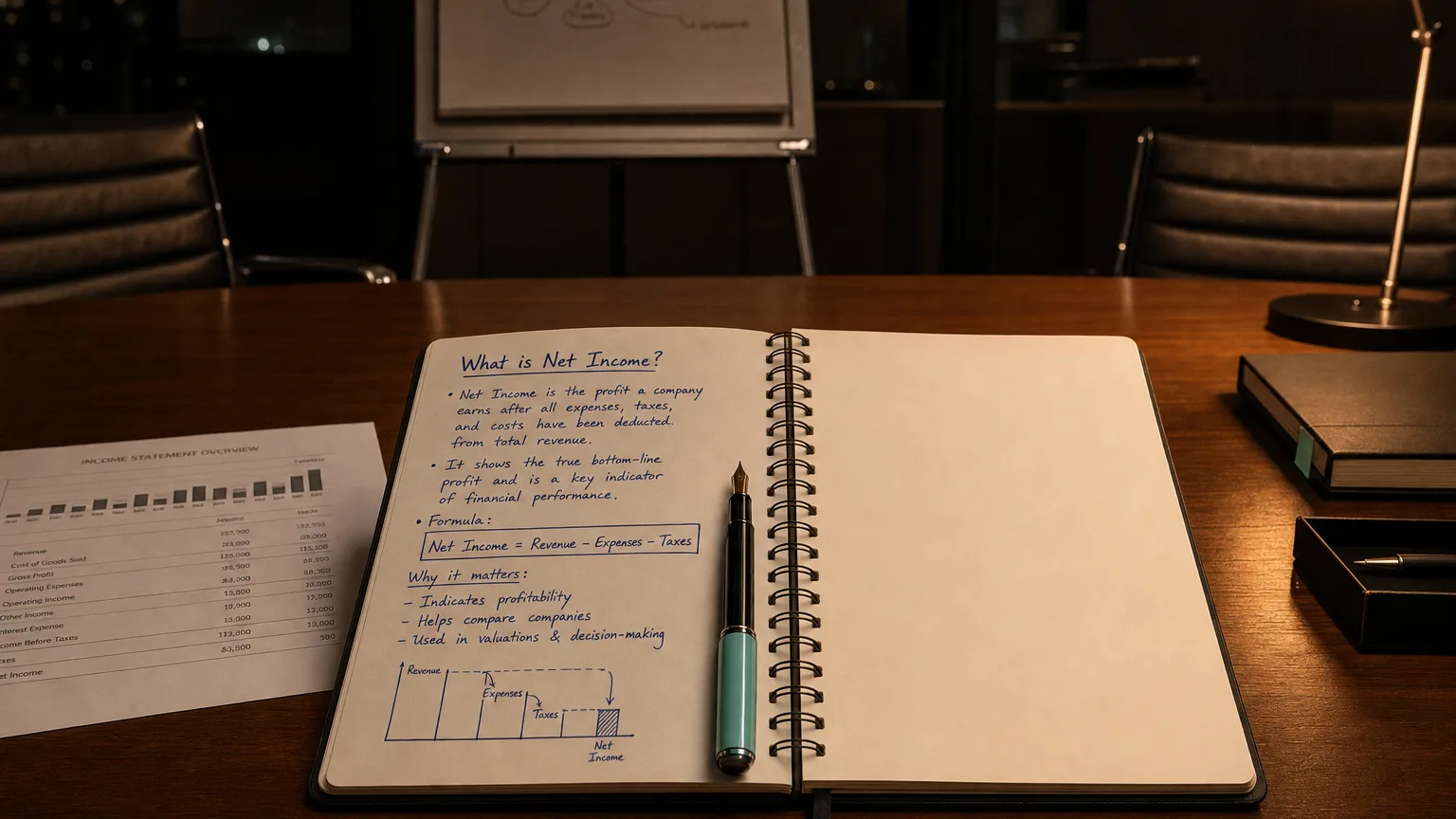

Net income is the total profit that remains after a company subtracts all of its expenses from its total revenues. In simple terms, it’s the amount of money a business earned during a period after paying all of its costs - including operating costs, interest on loans, and taxes. Net income is also commonly called net profit or net earnings, and it’s often referred to as the “bottom line” because it appears as the final line of the income statement.

Net Income Formula and Calculation

The formula for net income is straightforward, representing the difference between all revenues and all expenses.

Formula: Net Income = Total Revenues - Total Expenses

This means you start with all the revenue the company earned in the period and subtract every expense incurred to earn that revenue. If expenses are greater than revenues, the result is a negative net income, which is called a net loss. The calculation on an income statement is sequential, starting with revenue and progressively deducting different expense categories.

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

— Benjamin Graham, British-born American economist, professor and investor; founder of value investing Security Analysis (Graham & Dodd, 1st edition 1934); restated in The Intelligent Investor (4th rev. ed., 1973), Chapter 1, p. 18 (1934)

Components of Net Income

Net income is the final result after a series of deductions from revenue. The key components that feed into net income include:

- Revenue (Sales): The total income generated from selling goods or services. It’s the starting point or ‘top line’ of the income statement.

- Cost of Goods Sold (COGS): The direct costs of producing the goods or services sold. Subtracting COGS from revenue gives gross profit.

- Operating Expenses: The day-to-day costs of running the business, such as salaries, rent, and marketing. These are subtracted from gross profit to calculate operating income.

- Non-Operating Items: Income or expenses outside of main business activities, such as interest expense on loans or interest income from investments. These are factored in after operating income.

- Income Taxes: The last major deduction. The company’s tax expense is subtracted from pre-tax profit to arrive at the final net income.

Example Calculation of Net Income

Let’s look at a simple example for Wyatt’s Saddle Shop for one quarter:

Wyatt’s Saddle Shop - Q1 Financials

First, calculate gross profit:

Formula: 20,000 (COGS) = $40,000 (Gross Profit)

Next, subtract all other expenses (operating and interest) from the gross profit:

Formula: 19,000 (Operating Expenses) - 20,000 (Net Income)

Wyatt’s Saddle Shop earned a **net income of 20,000 of profit remained after all costs were covered.

Why Net Income Is Important

Net income is a vital metric for several reasons, and it matters to different stakeholders in different ways:

- For Businesses (Management): It is a key indicator of financial health and performance. A growing net income signals the company is on the right track; a shrinking net income is a warning sign that costs may need to be cut or strategies changed.

- For Investors/Shareholders: Investors use net income to evaluate profitability and to make comparisons. It is the basis for computing earnings per share (EPS), a fundamental metric for stock valuation. A strong net income means the company is generating value that can be paid out as dividends or reinvested for growth.

- For Financial Analysis: Net income is used in many important financial ratios. The net profit margin (Net Income / Revenue) shows what percentage of each dollar of revenue is kept as profit. It is also a key component in return on equity (ROE) and impacts the retained earnings on the balance sheet.