Tax Provision (Income Tax Expense) is a financial concept covered in this article. The Total Income Tax Expense a Company Reports for a Period

An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.

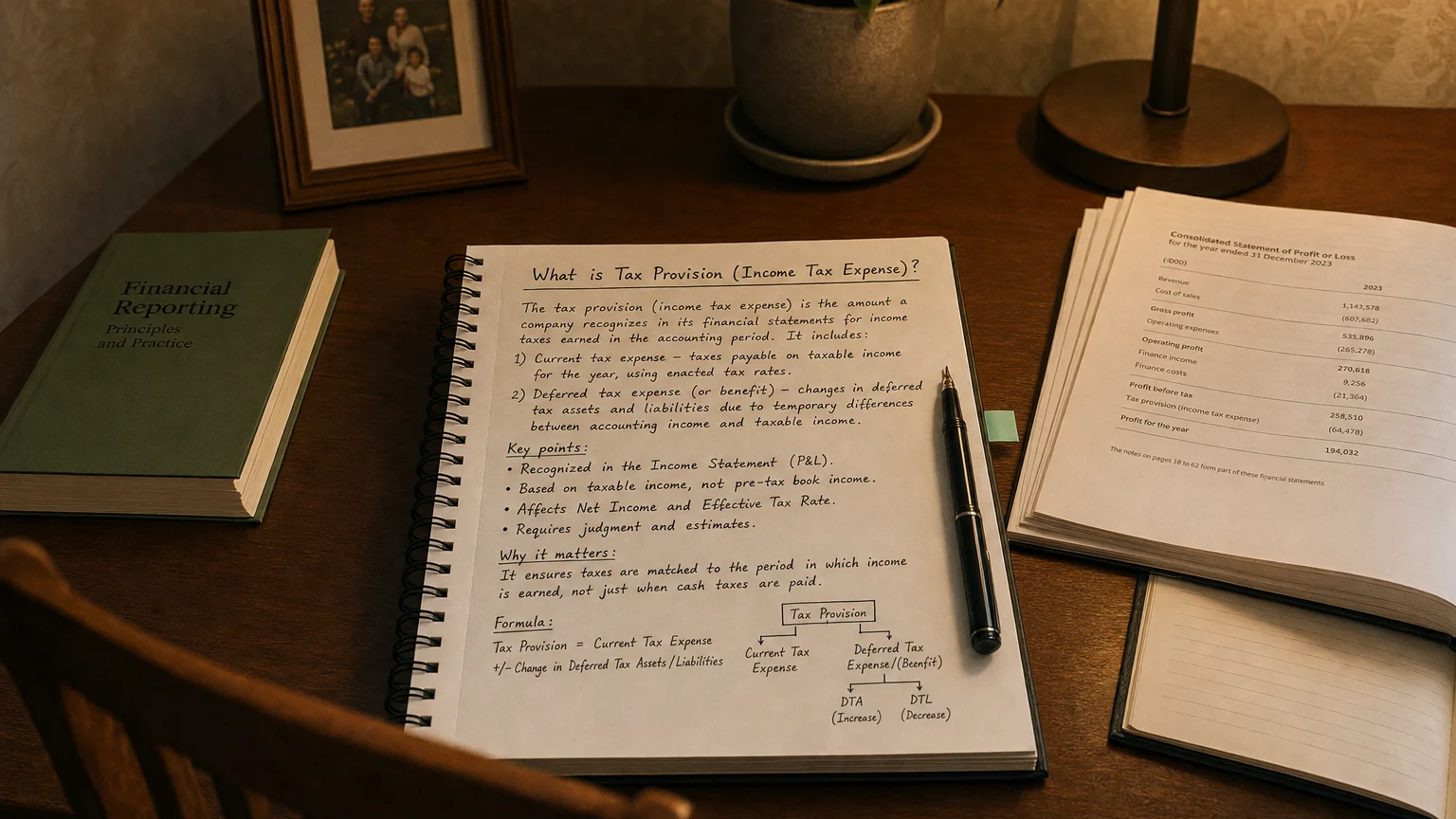

The tax provision (also called the provision for income taxes or income tax expense) is the total income tax expense reported for a given period in a company’s financial statements. It represents the amount of taxes the business expects to owe on its earnings for that period, including all applicable federal, state, local, and foreign income taxes. In other words, the tax provision focuses exclusively on income-based taxes (excluding other taxes like sales or payroll taxes) and is calculated according to accounting standards (e.g. ASC 740 under U.S. GAAP). The provision is typically comprised of two components: current income tax expense and deferred income tax expense.

-

Current income tax expense is the tax expected to be paid for the current period, essentially the tax liability computed as if preparing that period’s tax return under current tax laws.

-

Deferred income tax expense is an anticipated future tax cost or benefit that arises from timing differences between financial accounting and tax accounting. These deferred taxes result from temporary differences (items that are recognized in different periods for book vs. tax) and are recorded as deferred tax assets or liabilities on the balance sheet. The change in deferred tax assets/liabilities each period is recognized as deferred tax expense (or benefit) in the income statement.

Role and Significance in the Income Statement

On the income statement, the tax provision appears toward the bottom, after the pre-tax income line and before the final net income. It represents an expense – the estimated amount of income taxes owed on the period’s profits. Subtracting this income tax expense from income before taxes gives the net income (the company’s profit after taxes). For example, if a company’s income before taxes is $368,000 and its income tax expense (provision) is $77,000, the resulting net income would be $291,000 after accounting for taxes. This placement underlines the significance of the tax provision: it directly reduces earnings to reflect what will be paid out in taxes, giving stakeholders a view of after-tax profitability.

Beyond its numerical placement, the tax provision plays a crucial role in linking a company’s financial performance to its tax obligations. It provides an important bridge between GAAP financial reporting and the company’s actual tax liabilities. By including a tax provision, the income statement presents a more accurate financial picture to management and shareholders, showing the impact of income taxes on the company’s results. In essence, the tax provision ensures that the financial statements recognize the economic cost of taxes for the period, which is vital for fair presentation of net income and for informed decision-making by investors and management.

Calculation of the Tax Provision (Basic Principles & Example)

Calculating the tax provision involves determining the current tax expense based on taxable income and accounting for any deferred tax effects due to timing differences. In practice, companies follow a systematic process to compute the provision for income taxes. The basic steps include:

-

Start with Pre-Tax Book Income: Begin with the company’s net income before income taxes as determined by financial accounting (GAAP) for the period. This is the pre-tax profit figure from the income statement, which serves as the starting point.

-

Adjust for Permanent Differences: Identify any permanent differences between financial income and taxable income. Permanent differences are items of revenue or expense recorded under GAAP that are never taxable or deductible under tax law. Because they won’t ever reverse, these differences directly affect the current tax owed. Examples: fines and penalties, certain entertainment expenses disallowed by tax law, lobbying expenses, and tax-exempt income (such as municipal bond interest) are permanent differences. These items are added or subtracted from book income to arrive at taxable income, as appropriate (e.g. add back non-deductible expenses, remove tax-exempt revenues).

-

Adjust for Temporary Differences: Identify temporary differences (timing differences) between GAAP income and taxable income. These are revenues or expenses that are recognized in different periods for book vs. tax purposes, but will even out over time. For instance, an expense might be recorded in the financial books this year but not deductible for tax until a later year, or vice versa. Common temporary differences include differences in depreciation methods (e.g. accelerated tax depreciation vs. straight-line book depreciation), revenue recognition timing, provisions for bad debts or warranties (which may not be immediately tax-deductible), and accrued expenses not yet paid. For each temporary difference, the company determines how it modifies the current period’s taxable income (either increasing or decreasing it), with the understanding that the opposite effect will occur in a future period.

-

Calculate Taxable Income (after Differences): After adjusting pretax book income for all permanent and temporary differences, the result is the taxable income for the period. At this stage, the company may also apply any allowable tax credits or utilize net operating loss (NOL) carryforwards, which directly reduce the tax liability. These credits and NOLs are not expenses per se but are offsets allowed by tax law that reduce current taxes payable.

-

Apply Tax Rates to Compute Current Tax Expense: Multiply the taxable income (after all above adjustments) by the applicable tax rates to compute the current income tax expense. For a U.S. corporation, this typically means applying the federal corporate tax rate (e.g. 21% federal rate) plus any state (and local or foreign) tax rates on the portion of income taxable in those jurisdictions. The outcome is the amount of income tax the company expects to currently owe for the period’s income, before considering deferred effects. This current tax expense will correspond to the taxes payable to authorities for the year (recorded as a current tax liability on the balance sheet, unless prepayments or refunds create a receivable).

-

Compute Deferred Tax Expense/Benefit: Next, account for the deferred tax effects of the temporary differences identified earlier. The total cumulative temporary differences (the aggregate amount of income or expense that has been recognized for book purposes but not yet for tax, or vice versa) is multiplied by the relevant tax rate to determine the deferred tax liability or asset associated with those differences. The deferred tax expense for the period is the net change in the deferred tax liability/asset balance that results from current period temporary differences. In practice, this means if the company had certain revenues/expenses that will become taxable or deductible in the future, it records a deferred tax expense (or benefit) now to reflect the future tax impact. This deferred portion is reported on the income statement alongside the current tax expense, and the corresponding deferred tax asset or liability is updated on the balance sheet. (A deferred tax expense increases the total tax provision, reflecting taxes that will be paid in the future due to current period timing differences, whereas a deferred tax benefit reduces the tax provision, indicating an expectation of future tax savings.)

The total tax provision reported in the income statement is the sum of the current tax expense and the deferred tax expense (or benefit) computed in the above steps. To illustrate these principles with a simplified example, consider a company with $1,000 of pretax accounting income and a statutory tax rate of 21%:

-

No Differences Scenario: If there are no permanent or temporary differences, taxable income equals $1,000. The tax provision would simply be $1,000 × 21% = $210. This $210 would be recorded entirely as current tax expense (since there are no timing differences to create deferred tax). The effective tax rate in this simple case is 21%, equal to the statutory rate.

-

With a Permanent Difference: Suppose $50 of the expenses included in pretax income are not tax-deductible (a permanent difference). In this case, taxable income would be $1,050 (because the $50 expense cannot be deducted for tax). Applying the 21% rate, current tax expense becomes $220.5. The total tax provision is $220.5, which is higher than it would have been with no differences. The effective tax rate rises to about 22.05% ($220.5 ÷ $1,000) because the nondeductible expense caused the company to pay taxes on more than its book profit. (Permanent differences directly increase or decrease the tax provision and affect the effective tax rate since they do not reverse in future periods.)

-

With a Temporary Difference: Now assume instead that $50 of revenue in the $1,000 pretax income is taxable only in a future period (e.g. it was recognized in book income now, but tax law allows it to be taxed later – a temporary difference). In the current year, taxable income would be $950 (the $50 is not taxed now). Applying 21%, the current tax expense is $199.5. However, because that $50 will be taxed in the future, the company must also record a deferred tax expense of $10.5 (which is 21% of $50) to account for the future tax liability. The total tax provision remains $210 ($199.5 current + $10.5 deferred), the same as if no timing difference had existed, but it is now split between a current component and a deferred component. The effective tax rate in the current financial statements is still 21% in this case, since the temporary difference didn’t ultimately change the total taxes attributable to the $1,000 of book income – it only deferred $10.5 of tax to a later period. This demonstrates how temporary differences affect when tax is recognized (and whether it is current vs. deferred), but not the total tax ultimately paid on that income, assuming tax rates don’t change.

In summary, the tax provision calculation starts from accounting profit and navigates through various book-vs-tax adjustments to arrive at both the current tax due and the deferred tax implications. It requires careful consideration of the tax code and accounting rules to ensure that all differences are properly accounted for. The outcome is an income statement charge for taxes that reflects both the taxes payable on the current period’s taxable income and the expected future tax impacts of current period timing differences.

Current vs. Deferred Tax Provisions

It’s important to distinguish between the current and deferred portions of the tax provision, as they have different meanings and balance sheet implications:

-

Current Tax Provision (Current Tax Expense): This is the amount of income tax expense currently payable based on this period’s taxable income. It is calculated by applying the current tax laws and rates to the company’s taxable income or loss for the period. In essence, the current provision is the same figure one would compute on the corporate tax return for the period – it reflects the tax that is due to tax authorities for the year (or the refund receivable, if the company has a tax loss and paid estimates). This current tax expense is reported on the income statement and also appears as a current liability (Income Taxes Payable) on the balance sheet until the taxes are paid (or as a receivable if payments/withholding exceed the liability). Because it is tied to the taxable income of the period, the current portion is often described as the “true” tax on this year’s earnings, and it can be reconciled to the actual tax return filed with the IRS and other taxing jurisdictions.

-

Deferred Tax Provision (Deferred Tax Expense/Benefit): The deferred portion of the tax provision arises from temporary differences – items that will cause taxable income in future periods to be higher or lower than book income in those periods, due to timing. Deferred tax expense represents the increase in taxes in future years as a result of the current period’s temporary differences (a deferred tax benefit is the opposite: a decrease in future taxes due to current differences). These future tax effects are recorded on the balance sheet as deferred tax liabilities (for future tax increases) or deferred tax assets (for future tax reductions). The deferred tax expense or benefit each period is the change in those deferred tax balances that needs to be recognized to account for the current period’s timing differences. In other words, deferred taxes ensure that the total tax provision matches the accounting income of the period, even if some income/expenses will be taxed in a different year. On the income statement, the deferred tax expense is reported alongside the current tax expense, and together they sum to the total provision for income taxes. Importantly, while the deferred tax expense affects current financial results, it does not require a cash payment in the current period – it is a non-cash accounting adjustment that foreshadows future tax payments or savings. (Deferred tax liabilities and assets will crystallize into actual taxes payable or recoverable in future years when the timing differences reverse.)

In practice, analysts and financial statement users look at both components. The current tax tells how much tax is actually being incurred based on this year’s taxable income, whereas the deferred tax tells how much of the accounting tax expense is due to timing and will hit cash taxes in the future. Both current and deferred portions must be calculated for all relevant jurisdictions (federal, state, and international) and summed to the consolidated total tax provision. The breakdown of current vs. deferred tax expense is typically disclosed in the footnotes to the financial statements, providing transparency into how much of the provision is current vs. an accrual for future taxes.

Relationship with Taxable Income and Effective Tax Rate

The tax provision is closely related to taxable income, which is the base on which current taxes are computed. Starting from pretax financial income, companies adjust for permanent and temporary differences to arrive at taxable income for the period (as described above). The current tax expense portion of the provision is essentially “taxable income × tax rate” (after credits), reflecting what the company owes on its taxable profits. If financial accounting rules and tax laws were perfectly aligned (no differences), then taxable income would equal book pretax income, and the tax provision would simply equal the statutory tax rate times pretax income. In that ideal scenario, the company’s effective tax rate (ETR) would exactly equal the statutory tax rate.

However, in reality there are often differences and special items that cause the effective tax rate to diverge from the headline statutory rate. The effective tax rate is calculated as the total income tax expense divided by the pretax accounting income in the financial statements. It represents the overall rate of tax the company incurred on its book profits. This metric is important because it shows the impact of all tax planning, credits, and non-standard tax items on the company’s tax burden. An effective tax rate higher than the statutory rate means the company’s tax expense was increased by items that are not tax-deductible or by losses in certain jurisdictions, etc., whereas an ETR lower than the statutory rate indicates the presence of tax benefits like credits or tax-exempt income.

Several factors explain why the tax provision (and thus the effective tax rate) might differ from the simple statutory rate times pretax income:

-

Permanent differences: These directly affect the tax provision without any future reversal. For example, non-deductible expenses (such as certain fines, penalties, or half of meals & entertainment in the U.S.) increase the current tax due without increasing book pretax income, causing the effective tax rate to rise. Conversely, income that is exempt from tax (for instance, interest on municipal bonds) will reduce the tax provision relative to book income, lowering the effective tax rate. These items are called permanent differences because their impact on tax expense is permanent – they will never be recognized in a later period.

-

Tax credits: Credits (like R&D credits, foreign tax credits, etc.) directly reduce the tax owed dollar-for-dollar. They don’t affect pretax book income, but they reduce the tax provision, leading to an effective tax rate lower than the statutory rate. For instance, a company with large tax credits might pay far less than the standard rate on its income.

-

Different tax jurisdictions and rates: If a company earns income in jurisdictions with tax rates different from the home country rate, the overall tax provision will reflect that mix. For example, foreign subsidiaries’ earnings might be taxed at higher or lower rates than the domestic rate, or some states have additional taxes. This causes the consolidated effective tax rate to be a weighted average of various rates. Often, companies provide an effective tax rate reconciliation in their financial statement footnotes, explaining the numerical differences between the statutory U.S. federal rate and the company’s effective tax rate – typical reconciling items include tax-exempt income, nondeductible expenses, tax credits, effects of foreign tax rate differences, state taxes, and other special items.

In formula form, Effective Tax Rate (ETR) = Total Income Tax Provision / Pretax Income. For example, if a company reports $100 million in pretax income and a $20 million tax provision, its ETR is 20%. This rate can then be compared to the statutory corporate tax rate to judge whether the company’s tax strategies or income mix caused it to pay more or less than the baseline expectation. According to one explanation, a company’s effective tax rate “is the income tax expense recorded on its books, divided by pretax income,” and it shows whether the company is paying more or less than the expected statutory rate. Items such as tax credits and tax-exempt income reduce the effective tax rate, while non-deductible expenses and certain prior-period adjustments increase the effective tax rate. Management will often analyze and discuss the effective tax rate, since significant deviations from the statutory rate can be due to important factors (for instance, a one-time deduction, an audit settlement, or changes in valuation allowances), and investors want to understand those drivers.

Common Adjustments and Complexities in Tax Provisions

Preparing the tax provision is a complex task because it must reconcile two different rule sets (financial accounting vs. tax law) and incorporate many estimates and adjustments. Some common adjustments and complexities associated with the income tax provision include:

-

Permanent Differences: As noted, permanent book-tax differences (e.g. non-deductible expenses like penalties, certain entertainment or lobbying costs, and income exclusions like municipal bond interest) require adjustments to reconcile book income to taxable income. These do not reverse in future periods, so they directly impact the tax provision and effective tax rate in the period they occur. A company must identify all such items each period to compute the correct current tax and to explain why its tax rate differs from the statutory norm.

-

Temporary Differences and Deferred Taxes: Temporary differences (timing differences) add complexity because the company must track the timing of revenue and expense recognition for tax vs. book purposes across multiple periods. These differences complicate the provision since the accountant must estimate not only the tax for the current year but also set up deferred tax entries for the future impacts. Determining the proper deferred tax for each timing difference involves analyzing the balance sheet (e.g., comparing book vs. tax basis of assets and liabilities) and requires assumptions about when and how those differences will turn around. Changes in future tax laws or rates can further complicate this – if tax rates change, the value of deferred tax assets/liabilities must be revalued, resulting in adjustments to tax expense in the period of the change.

-

Multiple Jurisdictions and Tax Law Changes: Most companies operate in multiple tax jurisdictions (various countries, states, etc.), each with its own tax rates and rules. The tax provision process must incorporate federal, state, and international income taxes, applying the appropriate tax rate to income in each jurisdiction. This requires consolidating the tax calculations across jurisdictions into one total provision. Additionally, changes in tax laws or rates introduce complexity. A new tax law (for example, a rate reduction or an elimination of a deduction) can require re-calculation of the provision. For instance, a cut in corporate tax rate will decrease the value of deferred tax assets/liabilities, causing a one-time hit to the income statement as the deferred balances are adjusted. Tax departments must stay vigilant and up-to-date on law changes, as these can directly affect formulas and assumptions used in the provision. Keeping up with regulatory changes is a continual challenge in tax provisioning, and companies often need to adjust their provision process and computations whenever significant tax legislation is enacted.

-

Uncertain Tax Positions: Tax provisions often involve areas of judgment, especially when the tax treatment of certain items is unclear or subject to IRS (or other tax authority) challenge. Under accounting standards, companies must evaluate their uncertain tax positions – for example, aggressive tax deductions or positions that might be disallowed on audit – and record reserves for positions that are not more-likely-than-not to be sustained. This adds complexity, as it requires estimating the probability of outcomes and potential tax exposures. Many estimates go into the provision, and financial statements must adequately disclose the company’s overall tax position, including any significant uncertain tax positions, to inform readers. Accounting for uncertain positions (per ASC 740-10, formerly FIN 48 in U.S. GAAP) means that the tax provision might include a cushion or adjustment so that the company’s tax expense reflects only the portion of tax benefits that are likely to be realized.

-

Valuation Allowances for Deferred Tax Assets: If a company has deferred tax assets (DTAs) – such as those arising from net operating loss carryforwards or deductible temporary differences – it must assess whether it is likely to earn enough taxable income in the future to utilize those assets. If it is not likely (by the “more likely than not” criterion), the company must record a valuation allowance against the deferred tax asset, which effectively increases the tax provision. In other words, a valuation allowance reduces the carrying value of deferred tax assets to the amount that is expected to be realized in the future. Setting up or increasing a valuation allowance creates additional income tax expense in the current period. This is often a complex area because it requires forecasting future profitability and can have a large impact on earnings. For example, a startup with cumulative losses might not be allowed to recognize a tax benefit for those losses (it would record a full valuation allowance), whereas a turnaround in profitability could later justify releasing the allowance (resulting in a one-time tax benefit). Management and auditors must carefully evaluate evidence (both negative and positive) about future taxable income to decide if a valuation allowance is needed – making it one of the more judgment-heavy aspects of tax provisioning.

These are just a few of the common factors that make income tax provisioning a challenging process. The tax provision is not simply a plug number; it is the result of a detailed reconciliation between financial accounting income and taxable income, consideration of current tax laws, and strategic evaluation of future tax consequences. Because of this complexity, many companies invest in tax accounting expertise and systems to manage the provision process, ensuring that the income statement accurately reflects all relevant tax expenses. An accurate tax provision is critical for compliance (meeting tax reporting obligations) and for painting a truthful economic picture of the company’s after-tax performance to investors. By understanding the components and calculations behind the tax provision, one can better interpret a company’s financial statements and the effects taxes have on its overall financial health.