Basic Discontinuous Operations is the component of basic EPS attributable to discontinued operations—businesses divested or held for sale. It equals after-tax income or loss from those operations divided by basic weighted average shares, reported separately from continuing EPS.

Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

Basic Discontinuous Operations (commonly labeled as Basic Discontinued Operations in financial reports) represents the component of basic earnings per share (EPS) attributable to the results of discontinued operations. These are business segments, subsidiaries, or major lines of business that a company has divested or classified as held-for-sale. This metric isolates the after-tax, per-share earnings or loss from those discontinued activities using only the basic weighted average shares outstanding, enabling investors to clearly distinguish ongoing core performance from the effects of exiting non-core or underperforming operations.

What are Discontinued Operations?

Discontinued operations encompass components of an entity (such as a subsidiary, division, or major product line) that have been disposed of or are classified as held-for-sale under US GAAP (ASC 205-20) or IFRS (IFRS 5).

Qualification requires the disposal to represent a strategic shift with a significant impact on operations and financial results. Results—including ongoing operations while held, impairments, and final gain/loss on disposal—are reported net of tax, separately from continuing operations.

This separation ensures that basic EPS from continuing operations reflects only the performance of the remaining ongoing business.

How Basic Discontinuous Operations is Calculated

The calculation is consistent with other EPS components:

Formula: Basic Discontinuous Operations = (After-tax Income/Loss from Discontinued Operations) ÷ Basic Weighted Average Shares Outstanding

It incorporates:

- Operating results of the component during the holding period

- Impairment charges upon held-for-sale classification

- Gain or loss on disposal All adjusted for taxes and minority interests.

Tip: Basic shares exclude potential dilution, providing a direct impact on existing shareholders.

“Only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.”

— Howard Marks, Co-Chairman, Oaktree Capital Management Oaktree Memo: ‘The Most Important Thing’ (2003)

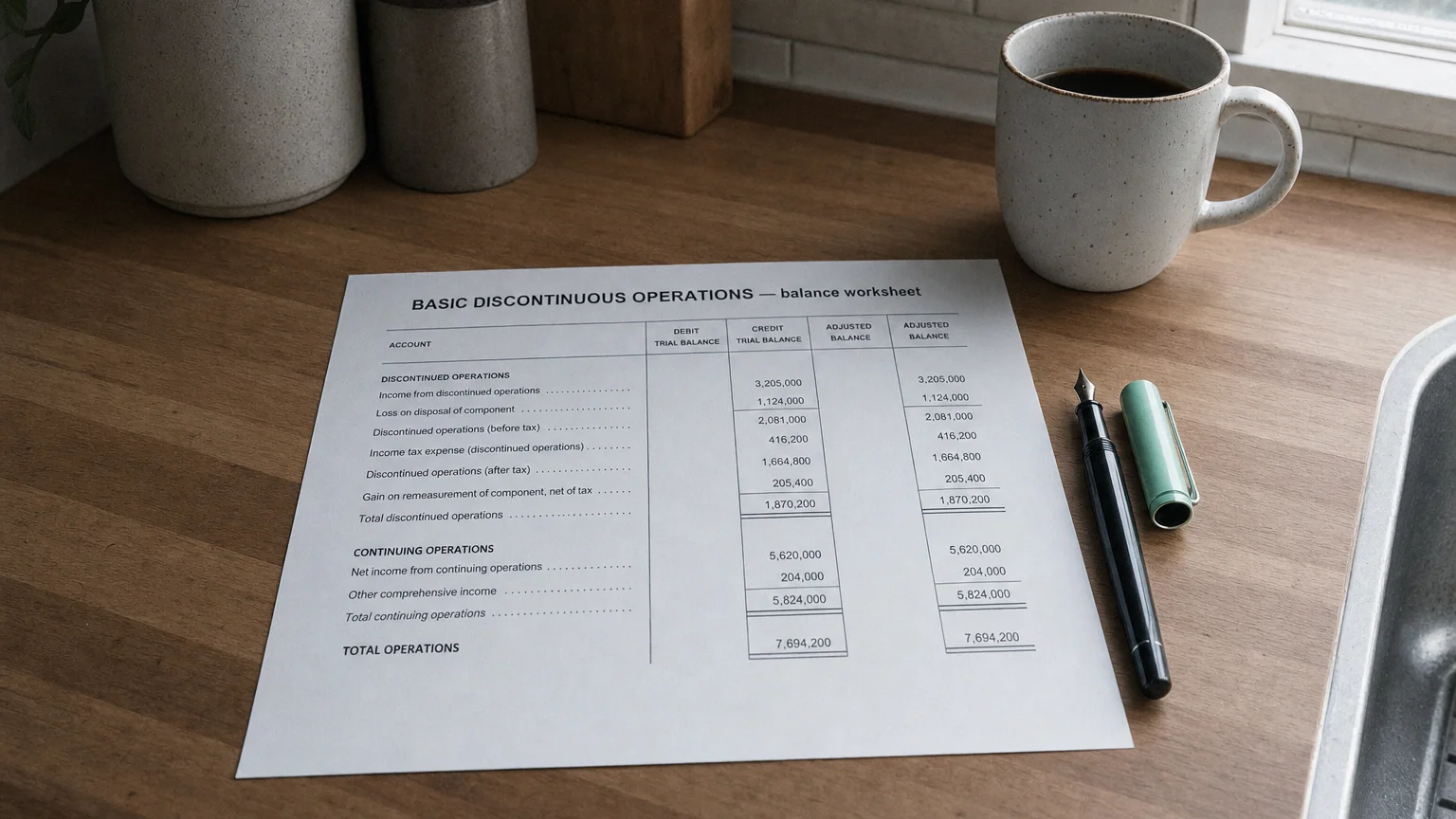

Examples

Example 1: Gain on Divestiture

Company sells a subsidiary for 250M). Pre-tax gain: 37.5M.

After-tax gain: 30M after-tax. Total discontinued: +0.7125 per share.

Example 2: Loss on Shutdown

Company closes a factory. Operating loss while held: −$20M after-tax.

Shutdown and impairment costs: −80M. Basic shares: 160M. Basic Discontinuous Operations = −$0.50 per share.

Positive values often signal successful portfolio pruning; negative values reflect costs of exiting troubled units.

Importance in Financial Analysis

This metric is vital because:

- Total basic EPS = Basic Continuous Operations + Basic Discontinuous Operations + Other Special Items

- Analysts prioritize continuing basic EPS for valuation and forecasting

- Large values indicate active portfolio restructuring

It is typically non-recurring and excluded when computing normalized basic EPS or forward estimates.

Warning: Repeated discontinued operations may suggest chronic strategic missteps or ongoing cleanup—examine management’s commentary.

Financial platforms provide this breakdown to reconcile headline basic EPS with core ongoing performance.

Q · 01What does Basic Discontinuous Operations represent?+

Q · 02How is Basic Discontinuous Operations calculated?+

Q · 03When is Basic Discontinuous Operations positive versus negative?+

Q · 04Why do analysts exclude Basic Discontinuous Operations from valuations?+

Q · 05What accounting standards govern discontinued operations reporting?+