is a financial concept covered in this article. A Bank's Core Profit from Lending and Borrowing

In investing, you get what you don't pay for. Costs matter enormously.

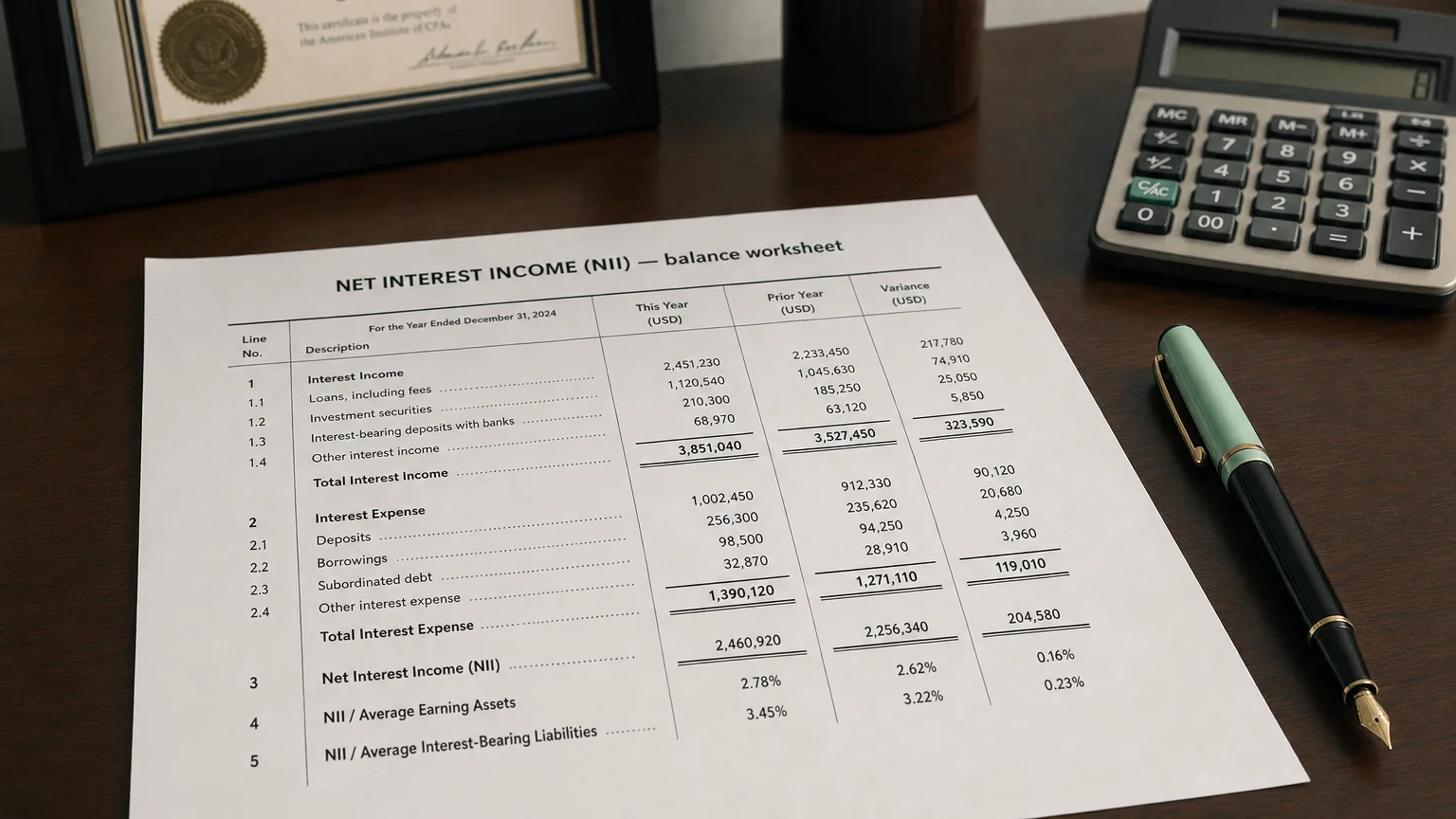

Net Interest Income (NII) is the difference between the interest a company (typically a bank) earns on its interest-bearing assets and the interest it pays on its liabilities. In simple terms, it’s the net profit from interest: the bank’s interest revenue minus its interest expense. For a bank, NII represents the profit from its core activity of taking in money (deposits) and lending it out. This spread between loan interest and deposit interest is essentially the bank’s income from its lending operations. NII is often viewed as the banking equivalent of gross profit in other industries.

How Net Interest Income is Calculated

The calculation for NII involves two main components:

- Interest Income (Revenue): This is the total interest earned on a bank’s assets, including interest received from loans, mortgages, bonds, and other interest-yielding investments.

- Interest Expense: This is the total interest paid on a bank’s liabilities, including interest paid to depositors on savings accounts and interest on any money the bank has borrowed.

Formula: Net Interest Income = Interest Income - Interest Expense

Calculation Example

Suppose in one year a bank earns 20 million in interest to its depositors (interest expense). The bank’s Net Interest Income for the year would be **50M - $20M).

“In investing, you get what you don’t pay for. Costs matter enormously.”

— John C. Bogle, Founder, The Vanguard Group Common Sense on Mutual Funds (1999)

Why NII is Particularly Important for Banks

NII is a critical indicator of a bank’s financial performance and stability for several key reasons:

- Primary Revenue Source: NII is often the largest source of revenue for traditional banks, as lending and borrowing are their primary activities.

- Key Profitability Metric: It measures how profitable the bank’s core operations are before other income or costs. Analysts and regulators watch NII as a key performance indicator.

- Funds Operations and Growth: A healthy NII provides the cash flow for banks to cover operating expenses (like salaries and branch costs) and to invest in growth.

- Reflects Intermediation Effectiveness: NII reflects how effectively a bank performs its role as a financial intermediary. A higher NII implies the bank is maintaining a good interest spread.

How NII Affects Overall Profitability

Changes in NII flow directly to the bottom line, but it is not the only factor in a bank’s profitability.

- Boosting Earnings: When net interest income increases, it directly boosts the bank’s total revenues and potential profit. For example, during a period of rising interest rates in 2023, Bank of America’s NII rose about 14% to $14.2 billion, which helped drive a 21% jump in its earnings per share.

- Profit Pressure when NII Falls: If NII stagnates or declines, profitability can suffer. This is common in a low interest rate environment, where the spread between loan and deposit rates narrows.

- Not the Whole Story: While NII is a major contributor, it isn’t the sole determinant of profitability. Banks also have non-interest income (like fees) and other expenses (operating costs, loan loss provisions) that affect net profit. A bank with high NII could still have poor overall profits if its other costs are too high.

Q · 01What is Net Interest Income?+