A key financing cash flow metric showing the net cash effect of a company issuing and repaying long-term debt, which are obligations due in more than one year.

Know what you own, and know why you own it.

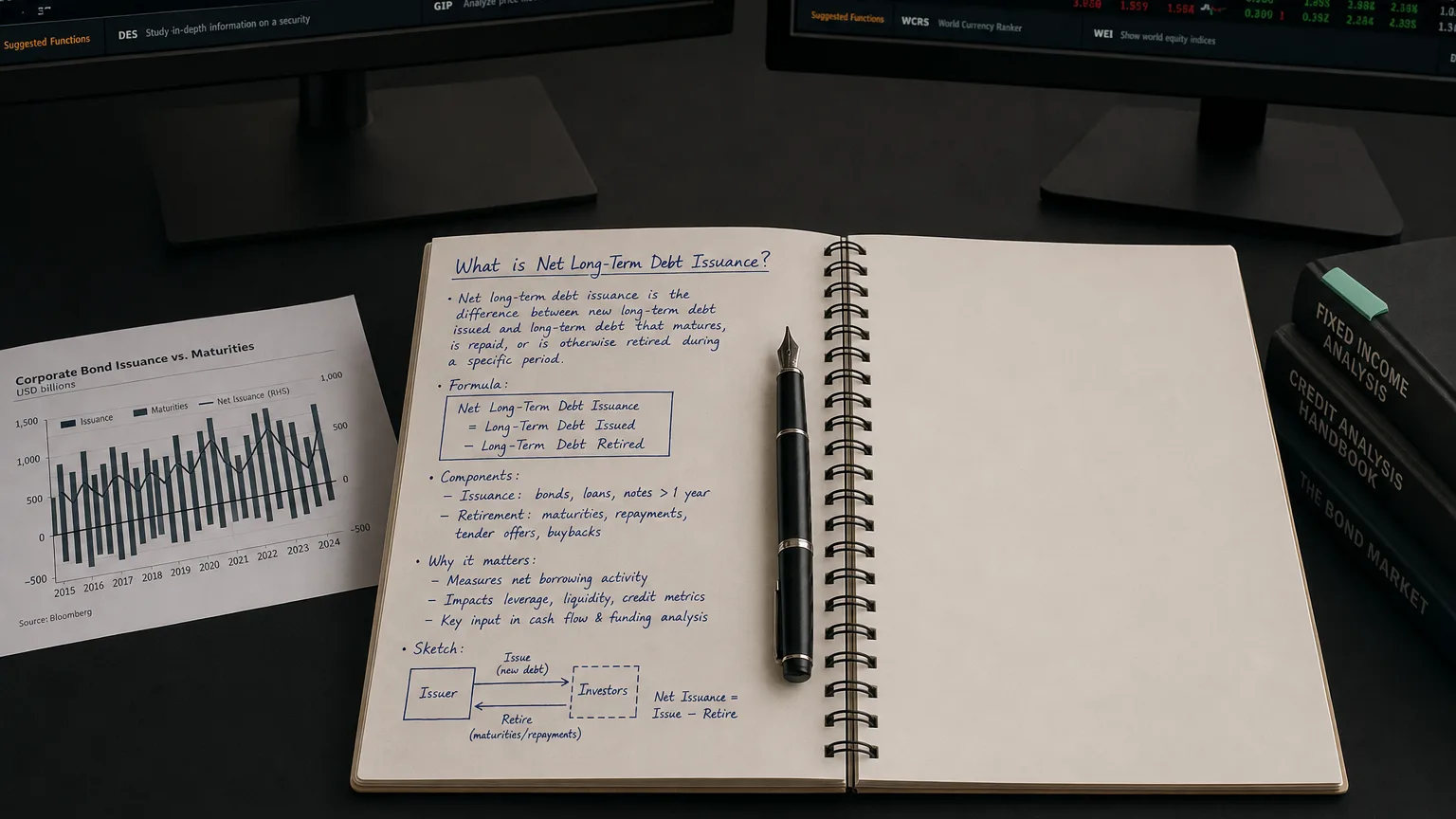

Net Long-Term Debt Issuance refers to the net cash a company raises (or repays) by borrowing. In other words, it is the amount of long-term debt issued minus the amount of long-term debt repaid during the period. “Long-term debt” generally means loans or bonds that mature beyond one year (for example, notes payable, bonds payable, mortgages, etc.). Thus if a company issues new bonds or takes a long-term loan, that is a cash inflow; if it repays principal on existing debt, that is a cash outflow. The net long-term debt issuance line on the cash flow statement simply shows the difference between these inflows and outflows for long-term borrowings. A positive net issuance means more new debt was issued than repaid (net cash raised), while a negative number means the company repaid more than it borrowed (net cash spent on debt).

Classification in the Cash Flow Statement

Issuing or repaying long-term debt is a financing activity, not an operating or investing activity. Accounting rules require these cash flows to be reported in the Financing Activities section of the cash flow statement. As IFRS explains, financing activities include transactions that change a company’s borrowings. In practice, this means any increase or decrease in long-term debt is shown in financing cash flows. For example, a textbook notes: “if there has been a change in a long-term liability… we must account for the item in the Financing section of the statement of cash flows”. (By contrast, operating cash flows come from day-to-day business activities, and investing cash flows come from buying or selling fixed assets or investments.)

Cash Inflow vs. Outflow

The phrase net issuance makes clear this item is the net effect of both inflows and outflows. Specifically:

-

Issuance of long-term debt (e.g. proceeds from new bonds or loans) is a cash inflow in financing.

-

Repayment of long-term debt (principal paid on bonds or loans) is a cash outflow in financing.

-

Net Long-Term Debt Issuance is the difference: (Issuance – Repayments).

If more debt is issued than repaid, the net figure is positive (a net inflow). If repayments exceed new borrowing, the net figure is negative (a net outflow). As one source notes, “a positive number indicates that cash has come into the company” (for example from new debt) and a negative number means “the company has paid out capital such as by… paying off long-term debt”.

For illustration, consider a simple example: suppose a company took out a new $30,000 bond (cash in) and paid $25,000 of an existing loan (cash out). The net long-term debt issuance would be $30,000 – $25,000 = $5,000 (net inflow). A KPMG example shows exactly this: “Proceeds from issuance of long-term debt $30,000” and “Principal payments on long-term debt $(25,000)$, yielding “Net cash provided by… financing activities $5,000”.

How Net Issuance is Calculated

Calculating net long-term debt issuance is straightforward:

-

Start with total cash received from issuing long-term debt (bonds, notes, etc.).

-

Subtract total cash paid to repay long-term debt principal.

-

The result is net long-term debt issuance.

In formula form:

Net Long-Term Debt Issuance = Long-Term Debt Issuance – Long-Term Debt Repayments.

If this calculation yields a positive number, it means the company raised cash by issuing more debt than it repaid. If it’s negative, it means the company used cash to repay more debt than it issued (a net debt payment). (Sometimes cash flow statements may list “Proceeds from debt” and “Repayments of debt” separately, and then show the net line.) In many real cash flow statements the net line is clearly labeled “Net Long-Term Debt Issuance (Repayment)” or similar.

Why Companies Issue or Repay Long-Term Debt

Companies manage long-term debt for various strategic reasons:

-

Raise capital for growth or operations: Firms issue bonds or long-term loans when they need cash to fund new projects, capital expenditures, acquisitions, or general expansion. Debt can be faster or cheaper to access than equity, especially if interest rates are low. For example, one analysis notes that large companies often borrow when interest rates are attractive, using debt to fund share buybacks or maintain cash balances. The corporate finance section of Investopedia explains that companies needing additional capital will “raise money by issuing debt or equity,” and these activities are reflected in the cash flow statement.

-

Refinance or restructure existing debt: A company might issue new long-term debt to refinance older debt (perhaps at a lower interest rate) or to change its debt maturity profile. For instance, swapping short-term loans for longer-term bonds can improve liquidity, since long-term debt “gives a company flexibility to pay debt down over a longer period”.

-

Return to shareholders or other uses: If a firm has excess cash, it may choose to repay debt (negative net issuance) rather than hold it. Repaying debt reduces future interest costs and can strengthen the balance sheet. In some cases, companies issue debt to fund dividends or share repurchases, but others reduce debt when they have free cash. For example, a report on Amazon’s finances noted that the company “ceased [issuing] long-term debt” in recent years and began ramping up repayments, signaling a shift to debt reductionstock-analysis-on.net.

In summary, issuing debt provides new cash (an inflow) which can finance growth or shareholder returns, while repaying debt uses cash (an outflow) to reduce leverage and interest expense.

Implications of Positive vs. Negative Net Issuance

The sign of net long-term debt issuance has important financial implications:

-

Positive Net Issuance: A positive net figure means the company raised cash by borrowing (more debt issued than repaid). This boosts liquidity and can fund new investments, but it also increases the company’s leverage. Higher debt means higher future interest payments and potential strain if cash flows drop. Investors might view sustained heavy borrowing as a risk if it seems to fund losses or unsustainable growth. (However, in some cases taking on debt is prudent: for example, businesses often issue long-term bonds during low-rate environments to finance low-cost expansion.)

-

Negative Net Issuance: A negative (or below-zero) net issuance means the company paid down more debt than it borrowed. This reduces debt levels and future interest obligations, which can strengthen the balance sheet. It may be a sign of financial strength (company has enough cash to pay debts) or a conservative strategy to lower risk. For example, one analysis commented that Amazon’s shift to net debt repayment (negative issuance) was consistent with “debt reduction efforts”. On the other hand, very negative numbers could indicate the company is using a lot of cash to pay debt and not investing or returning cash to owners.

In other words, positive net issuance is generally a source of cash (borrowing), while negative net issuance is a use of cash (repaying debt). As noted, one guide says a negative financing cash flow “is not necessarily bad” – it depends on why the company is borrowing or paying down debt and on other cash flows.

Example Entries in Real Cash Flow Statements

In practice, a cash flow statement’s financing section will often list lines like “Proceeds from issuance of long-term debt” and “Repayments of long-term debt”. It might also show a combined line like “Net cash provided by (used in) financing activities” which includes net debt issuance along with other financing items.

For a concrete example, KPMG’s handbook shows this breakdown:

-

Proceeds from issuance of long-term debt: $30,000

-

Principal payments on long-term debt: $(25,000)$

-

Net cash provided by financing activities: $5,000

Here the net long-term debt issuance was +$5,000.

As a real-world case, a financial analysis of Amazon’s 10-K explains how net long-term debt issuance has changed. It notes that after 2022, Amazon “long-term debt issuance ceased… while repayments increased”, indicating that recent net issuance was negative as the company focused on paying down debt. In contrast, you might see a tech firm’s cash flow showing a large positive net issuance number if it borrowed heavily to fund a new factory or acquisition.

Overall, Net Long-Term Debt Issuance is simply the net borrowing (or repayment) cash flow for long-term debt, reported in the financing section. It highlights how much new debt capital a firm raised versus how much it paid back, and helps readers understand one source or use of cash for the business.

Sources: Definitions and concepts of cash flows are drawn from accounting and finance references. Classification guidance comes from accounting standards and textbooks. Specific illustrations and examples are adapted from Investopedia, a corporate finance tutorial, KPMG guidance, and a published analysis of Amazon’s cash flows.