A financing cash flow metric showing the net cash effect of a company issuing and repaying short-term debt, which are obligations due within one year.

Pennies don't fall from heaven, they have to be earned here on earth.

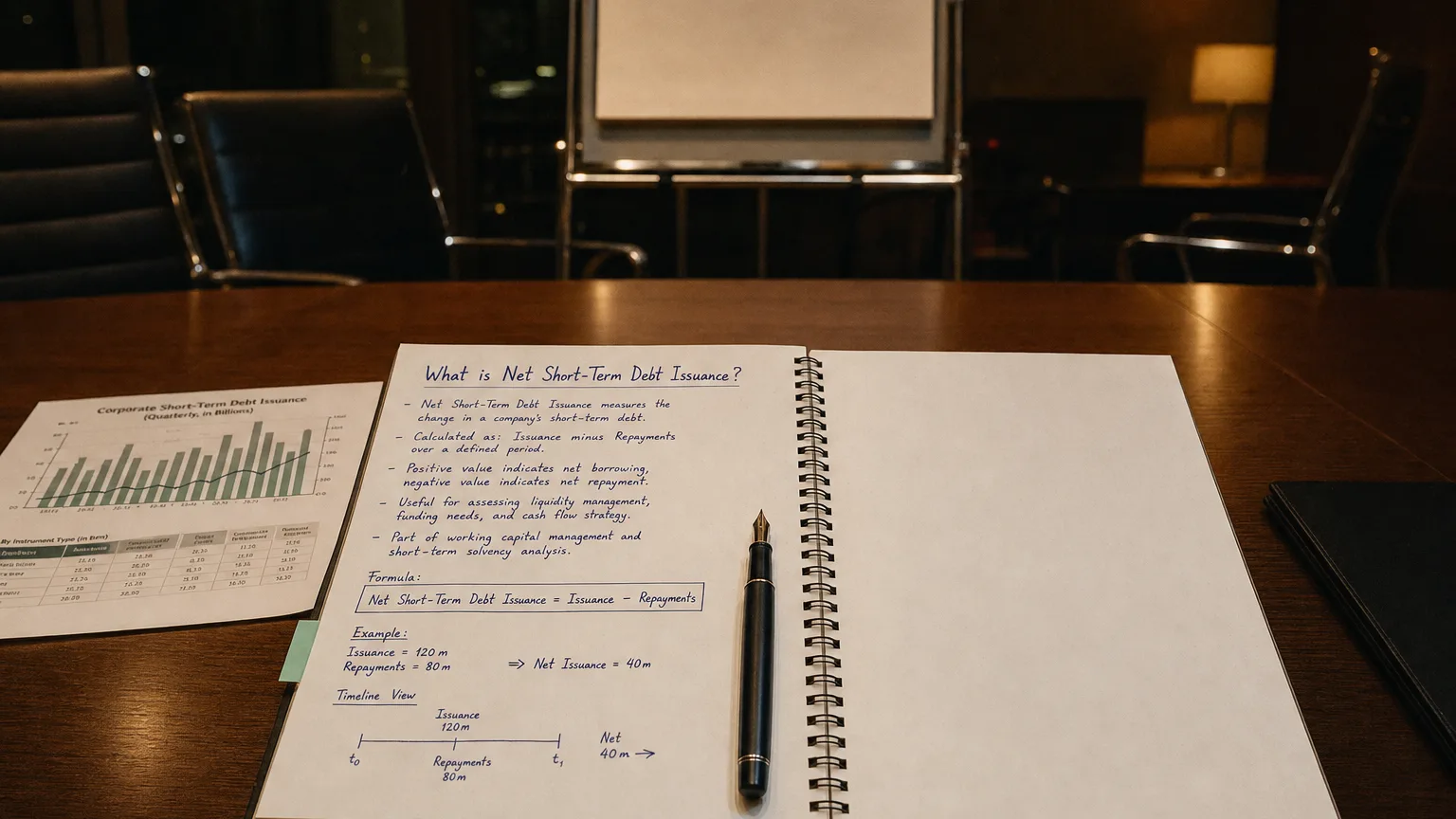

Net short-term debt issuance measures a company’s net borrowing via short-term debt over a period. In other words, it is the total cash from short‐term debt issued minus the short‐term debt repaid during that period. A positive net issuance means the company took on more short-term debt than it repaid (a net cash inflow), while a negative net issuance means it repaid more than it borrowed (a net cash outflow). This figure is always reported in the Financing Activities section of the Statement of Cash Flows.

Calculation and Interpretation

The calculation for net short-term debt issuance is a simple netting of the cash inflows from new short-term borrowings against the cash outflows for repayments of existing short-term debt.

Formula:

Illustrative Calculation

Strategic Use and Analytical Implications

“Pennies don’t fall from heaven, they have to be earned here on earth.”

— Margaret Thatcher, Prime Minister of the United Kingdom (1979-1990) Speech at Lord Mayor’s Banquet, London (1979)

Why Companies Use Short-Term Debt

- Working Capital: To cover immediate expenses like inventory or payroll, acting as a temporary cash bridge.

- Seasonal Needs: To manage cash shortfalls in businesses with seasonal revenue cycles.

- Bridge Financing: To fill a temporary funding gap before long-term financing (like a bond issue) is secured.

- Flexibility: To access funds quickly, as short-term credit lines often have faster approval processes than long-term loans.

A positive net issuance boosts a company’s immediate liquidity but increases its short-term liabilities and future interest costs. A sustained positive trend might indicate a reliance on debt to fund operations. A negative net issuance shows the company is using cash to pay down its short-term obligations, which reduces liabilities and can signal strong internal cash generation. However, neither is inherently good or bad without understanding the company’s specific strategy and financial health.

Real-World Examples

McDonald’s and Apple

Financial statements show this line item clearly. For instance, a McDonald’s cash flow statement reported “Net short-term borrowings” of -1,022K in a prior year, reflecting net borrowing. These examples illustrate how the figure can swing between positive and negative depending on the company’s financing activities in a given year.