is a financial concept covered in this article. Non-Income Taxes Expensed in Operations

If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes.

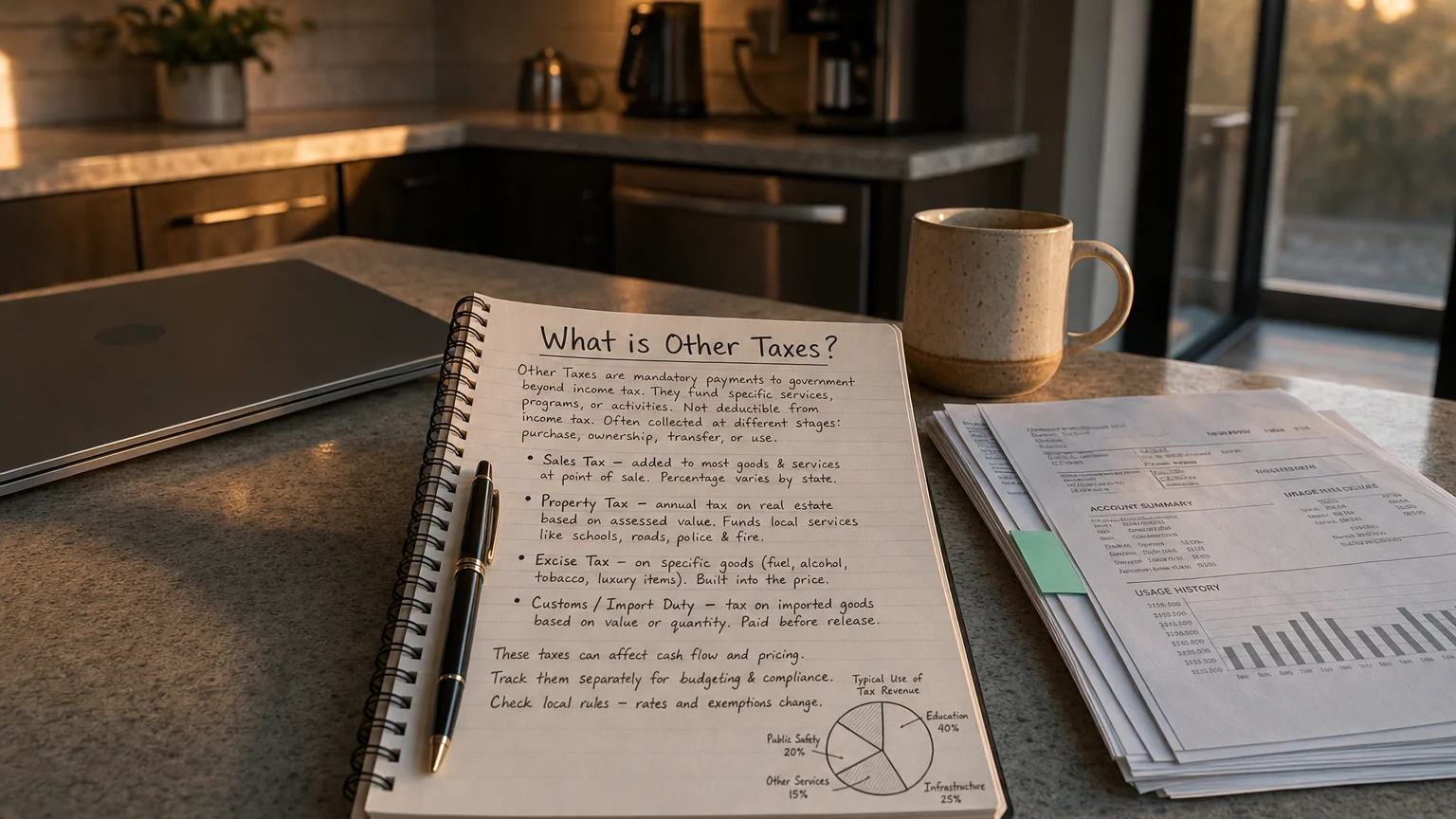

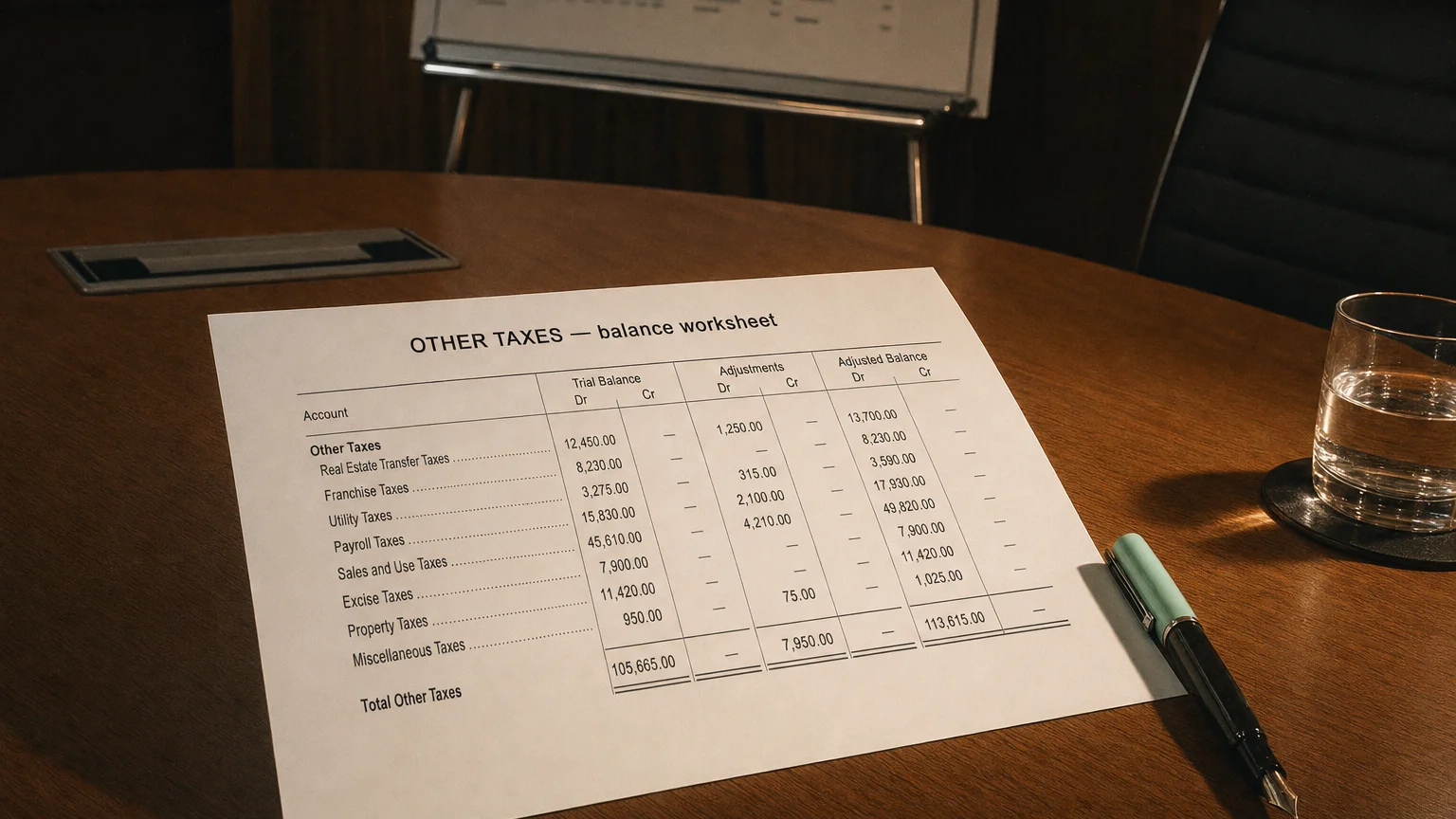

Other Taxes refers to the various tax expenses a company incurs that are not related to income taxes (which are reported separately in the tax provision). These include property taxes, sales and use taxes, payroll taxes (employer portion), excise taxes, value-added taxes (VAT) not recoverable, franchise taxes, and other governmental levies tied to operations. Classified as operating expenses, they are recurring costs of doing business and directly reduce operating income. Understanding this line item is essential for assessing total tax burden, cost structure, and operating margins beyond just the effective income tax rate.

What are Other Taxes?

Other Taxes encompass all tax obligations excluding corporate income taxes. These are primarily transaction-based, asset-based, or employment-based levies imposed by federal, state, local, or foreign governments.

Unlike the tax provision (which is based on pre-tax income), other taxes are generally fixed or volume-driven and treated as operating costs. They are expensed as incurred and included in operating expenses, typically within cost of revenue or SG&A.

These taxes represent the ‘hidden’ tax burden—often overlooked compared to headline income tax rates but material for total cost analysis.

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

— Warren Buffett, Chairman & CEO, Berkshire Hathaway Berkshire Hathaway Chairman’s Letter 1996 (1996)

Common Types of Other Taxes

Major categories include:

Typical Other Taxes

- Property taxes: On real estate, equipment, and sometimes inventory

- Payroll taxes: Employer share of Social Security, Medicare, unemployment (employee portion withheld)

- Sales and use taxes: Collected/remitted on sales or paid on purchases

- Excise taxes: On specific goods (fuel, alcohol, tobacco)

- VAT/GST: Non-recoverable portion in some jurisdictions

- Franchise/business license taxes: Based on capital or revenue in certain states

- Customs duties/import tariffs

- Environmental or carbon taxes

Industry-specific taxes (e.g., bank levies, telecom spectrum fees) may also appear here.

How Other Taxes Are Reported

Placement in the income statement:

Common Locations

- Within Cost of Revenue (e.g., excise, production-related)

- Within SG&A (property, payroll, franchise)

- Separate line as Other Operating Expenses or Taxes Other Than Income

They reduce operating income and are included in EBITDA calculations (not added back like depreciation).

Tip: Total tax burden = Income taxes + Other taxes; compare across peers for true cost competitiveness.

Examples

Example 1: Retail Company

Property taxes on stores/warehouses: $80M

Payroll taxes (employer): 15M Franchise taxes: 225M (primarily in SG&A).

Example 2: Manufacturer

Property taxes on plants: $40M

Excise taxes on products: 90M Environmental levies: 202M (split between cost of revenue and operating).

Growth in other taxes can reflect expansion (more property/employees) or rate changes.

Importance in Financial Analysis

Analysts examine other taxes to:

- Calculate total effective tax rate (income + other taxes / pretax income)

- Assess operating margin quality

- Benchmark cost structure vs. peers

- Evaluate geographic exposure (varying state/local rates)

Rising other taxes relative to revenue may signal inefficiencies or unfavorable locations. They are recurring and included in normalized profitability metrics.

Warning: Some companies net recoverable VAT/GST—gross presentation can inflate both revenue and expenses.

Q · 01What is Other Taxes?+