Provision for Doubtful Accounts is a financial concept covered in this article. The Expense Recognizing Expected Credit Losses on Receivables

In the short run, the market is a voting machine. In the long run, it is a weighing machine.

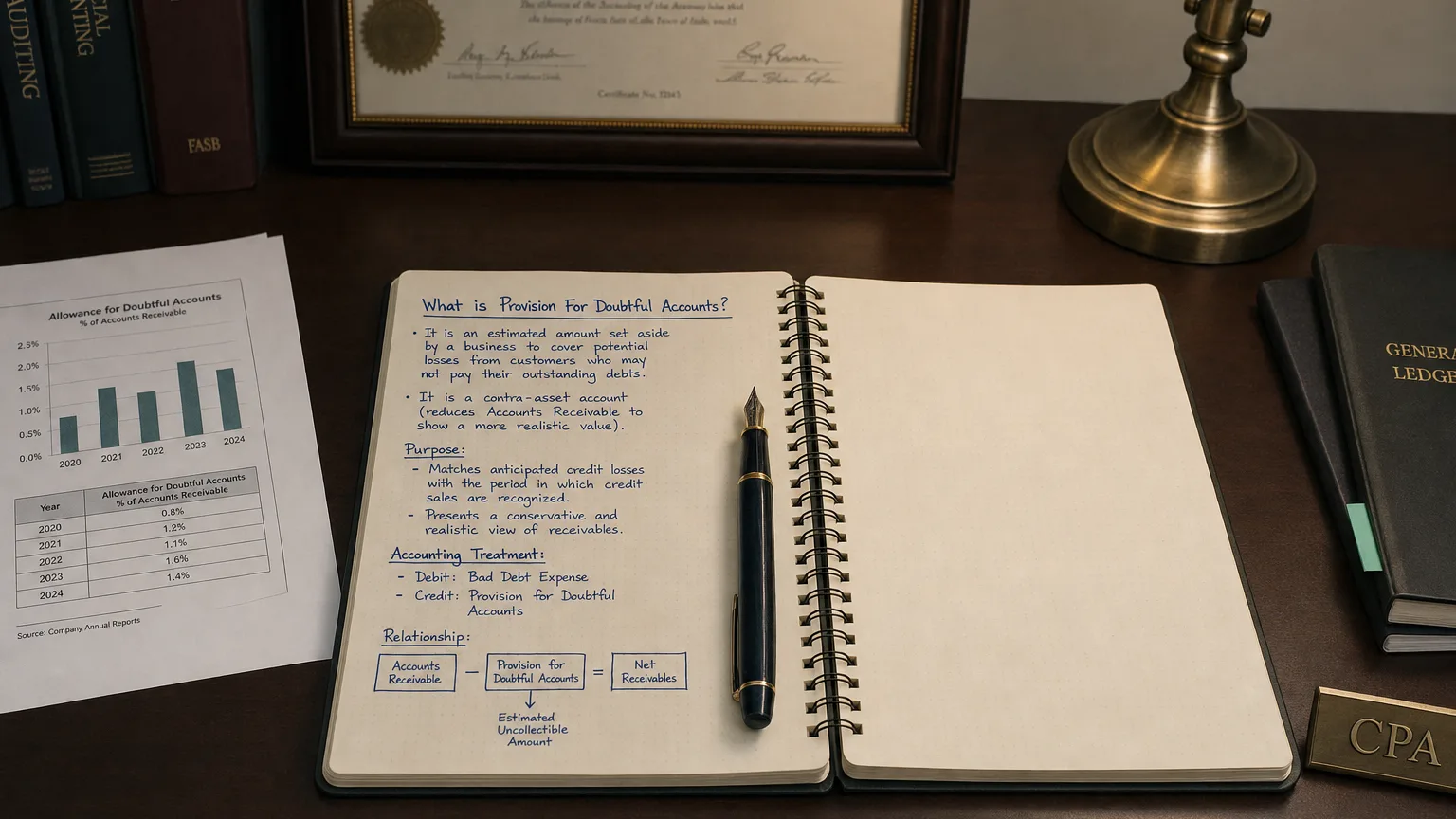

Provision for Doubtful Accounts (also known as Bad Debt Expense or Credit Loss Provision) is the non-cash expense a company records to estimate the portion of accounts receivable that is expected to become uncollectible. It reflects anticipated credit losses from customers who may default or delay payment beyond recovery. This provision increases the allowance for doubtful accounts (a contra-asset on the balance sheet) and is charged against income, reducing reported profitability. Accurate provisioning is crucial for presenting a realistic net receivables value and assessing credit risk management, revenue quality, and earnings sustainability.

What is Provision for Doubtful Accounts?

The provision for doubtful accounts is an estimate of the amount of accounts receivable (AR) that will not be collected. It follows the accrual accounting matching principle by recognizing expected losses in the same period as the related revenue.

Under US GAAP (ASC 326, CECL model since 2019) and IFRS (IFRS 9, expected credit loss model), companies must estimate lifetime expected credit losses rather than waiting for specific delinquencies (incurred loss model pre-2019).

The expense reduces net income while the allowance reduces gross AR to net realizable value on the balance sheet.

Higher provisions signal increased credit risk, economic stress, or aggressive revenue recognition.

“In the short run, the market is a voting machine. In the long run, it is a weighing machine.”

— Benjamin Graham, Author, The Intelligent Investor Security Analysis (1934)

How the Provision is Calculated

Common estimation methods:

Estimation Approaches

- Percentage of Sales (Income Statement Approach): Fixed % of credit sales (e.g., historical bad debt rate)

- Percentage of Receivables (Balance Sheet Approach): % of ending AR, often aging-based

- Aging Schedule: Higher % for older receivables (30-60-90+ days)

- CECL/Expected Loss Model: Forward-looking, incorporating macroeconomic factors

Formula: Dr. Provision for Doubtful Accounts (Expense) XXX Cr. Allowance for Doubtful Accounts XXX

When actual bad debt occurs: Dr. Allowance → Cr. Accounts Receivable (no further expense).

Examples

Example 1: Percentage of Sales

Credit sales: $10M

Historical bad debt rate: 2% Provision = 200K expense Allowance increases by $200K.

Example 2: Aging Method

AR breakdown:

0-30 days: 50K 31-60 days: 100K 61-90 days: 200K

90 days: 250K Total Required Allowance = 400K Provision = $200K additional expense.

Example 3: Economic Downturn

CECL model forecasts higher defaults due to recession.

Expected lifetime losses increase from 800K. Provision = $500K charge (forward-looking impact).

Spikes often coincide with credit policy changes or customer distress.

Presentation in Financial Statements

Typically reported as:

Common Locations

- Within Selling, General & Administrative (SG&A) expenses

- Sometimes in Cost of Revenue (if trade-related)

- Separate line in detailed operating expenses

Reduces operating income; allowance shown as contra-asset under current assets.

Importance in Financial Analysis

Analysts monitor provisions to:

- Evaluate revenue quality (aggressive credit terms inflate sales but raise provisions)

- Assess credit risk management

- Gauge economic sensitivity (higher in downturns)

- Calculate cash conversion (add back non-cash expense)

Days Sales Outstanding (DSO) and bad debt ratio (provision/sales) are key metrics. Persistent high provisions may indicate customer quality issues.

Warning: Low provisions relative to peers or history can signal under-reserving (earnings inflation risk).