is a financial concept covered in this article. Additional Disclosures and Details on Lease-Related Rent Expenses

In investing, you get what you don't pay for. Costs matter enormously.

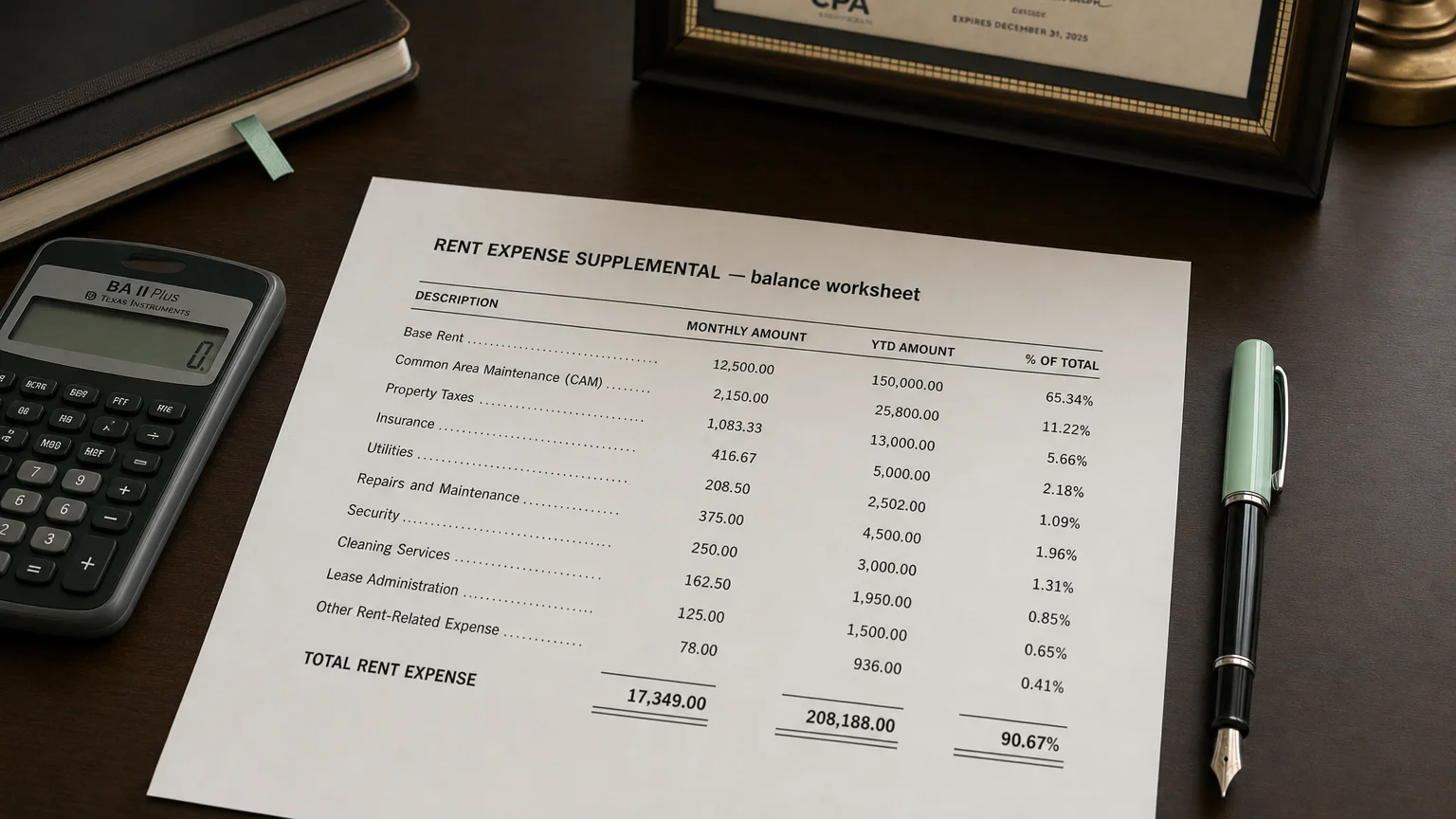

Rent Expense Supplemental refers to the additional information and breakout details provided in the financial statement footnotes or supplemental schedules regarding a company’s rental and lease obligations. This line item typically includes operating lease rent expense, short-term lease costs, variable lease payments, and sublease income that are not capitalized on the balance sheet under operating lease accounting. It offers greater transparency into ongoing rental commitments, especially useful for analyzing cash operating expenses before the full adoption of new lease standards (ASC 842/IFRS 16) that brought most leases onto the balance sheet. Understanding this supplemental disclosure helps assess recurring facility costs and compare pre- and post-lease-standard financials.

What is Rent Expense Supplemental?

Rent Expense Supplemental provides expanded disclosure on rental and lease-related costs that are expensed through the income statement rather than capitalized.

Before major lease accounting changes (ASC 842 in US GAAP, effective 2019 for public companies; IFRS 16 in 2019), most operating leases were off-balance-sheet, and rent expense was simply the periodic cash payment. The supplemental note detailed minimum rentals, contingent rents, and sublease income.

Post-adoption, long-term operating leases are capitalized (right-of-use asset and lease liability), with expense split between depreciation and interest. The supplemental disclosure now focuses on short-term leases, variable payments, and cash flow details.

This disclosure remains valuable for understanding cash rent outflows and comparing companies across lease standard transitions.

Components Typically Included

Common elements in the supplemental note:

Key Disclosures

- Operating lease rent expense (pre-ASC 842: full amount; post: short-term only)

- Short-term lease expense (leases ≤12 months, elected exemption)

- Variable lease payments (e.g., percentage rents, CPI adjustments, utilities)

- Sublease income (offsetting rental revenue)

- Minimum rental commitments (future undiscounted payments schedule)

- Cash paid for operating leases (supplemental cash flow info)

Industry-specific items (e.g., retail percentage rents, airline landing fees) may also appear here.

“In investing, you get what you don’t pay for. Costs matter enormously.”

— John C. Bogle, Founder, The Vanguard Group Common Sense on Mutual Funds (1999)

Pre- vs. Post-Lease Standard Treatment

The evolution impacts analysis:

Key Changes

- Pre-ASC 842/IFRS 16: Straight-line rent expense for operating leases (including escalations)

- Post-adoption: Front-loaded expense (depreciation + interest); supplemental shows cash rent and short-term/variable

- Comparability: Supplemental data helps adjust historical metrics to new standard

Tip: Many analysts add back lease interest and use cash rent from supplemental for consistent EBITDA calculations.

Examples

Example 1: Retail Company (Post-ASC 842)

Total lease cost: $500M

- Operating lease depreciation: $400M

- Operating lease interest: $80M

- Short-term lease expense: $15M

- Variable lease payments: $45M

- Sublease income: (60M cash-like operating rent (short-term + variable).

Example 2: Pre-Standard Disclosure

Minimum rental expense: $300M

Contingent rent (percentage of sales): 20M Net Rent Expense Supplemental: $330M straight-line operating lease cost.

These details enable cash-based rent comparisons across periods and peers.

Importance in Financial Analysis

Analysts use rent expense supplemental to:

- Estimate recurring facility costs

- Adjust EBITDA for consistent lease treatment

- Assess occupancy cost ratios (rent/sales for retailers)

- Model future cash commitments from lease schedules

High variable or short-term rent indicates flexibility; heavy long-term commitments (now on-balance) signal fixed cost burden.

Warning: Post-lease standard, headline rent expense drops dramatically—rely on supplemental cash paid for operating leases to avoid misleading trends.

Q · 01What is Rent Expense Supplemental?+